- Home

- >

- News

- >

- Transpacific Rates Hold Steady as Tariff Uncertainty Keeps Importers on the Sidelines - TFX Update: wk. August 4, 2025

Transpacific Rates Hold Steady as Tariff Uncertainty Keeps Importers on the Sidelines - TFX Update: wk. August 4, 2025

The Lead:

Reciprocal tariffs are back, rates are back to 2024 levels for now & more.

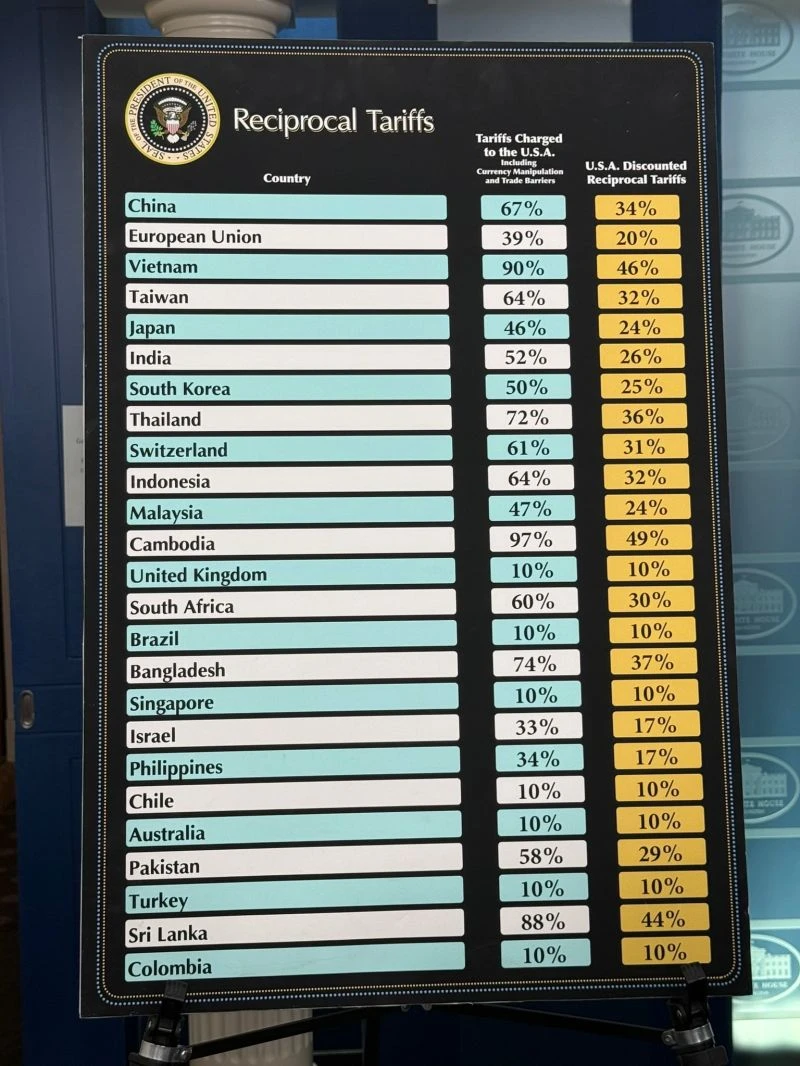

Last week, global trade policy was dominated by sharp escalation in US tariffs under the Trump administration. On July 31st, a sweeping executive order set new reciprocal tariffs, ranging from 15 % baseline to as high as 50% on imports from countries like Canada, Brazil, India, Taiwan, and Switzerland, scheduled to take effect August 7. These measures rattled global markets, with stock indices dropping and investor confidence wavering. India was singled out in U.S. policy rhetoric and tariff enforcement, with no exemptions granted. In response, the EU froze planned retaliatory tariffs for six months, signaling a temporary de-escalation and opening space for fresh negotiations. Amid this turbulence, the IMF reported that although global tariffs eased slightly in June, uncertainty remained elevated and trade policy unpredictability persisted globally.

On Markets & Rates:

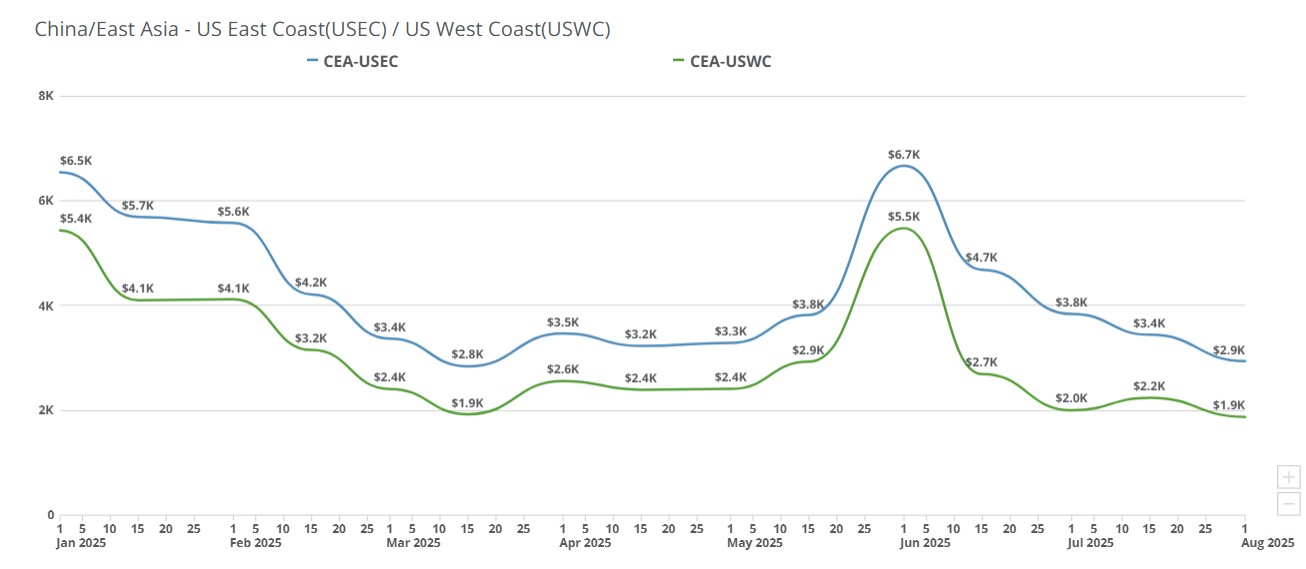

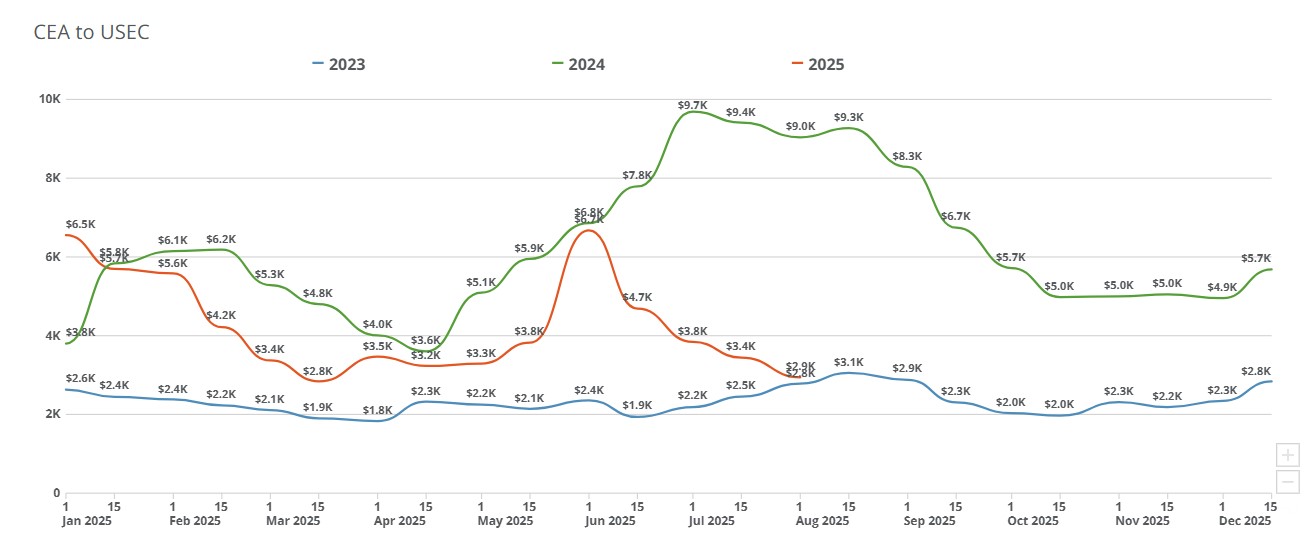

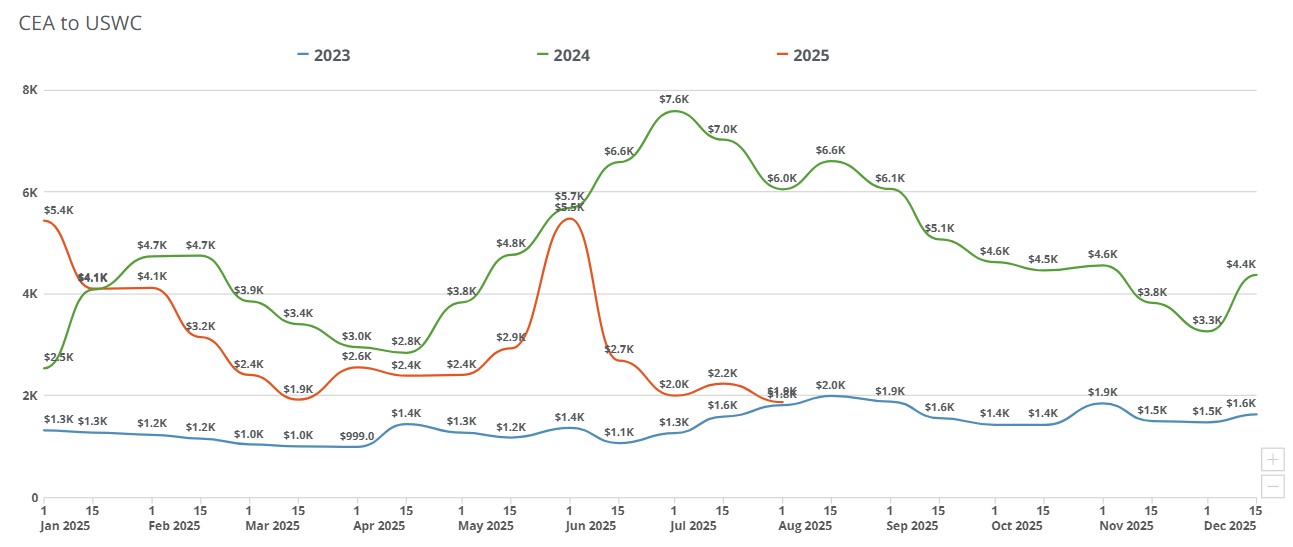

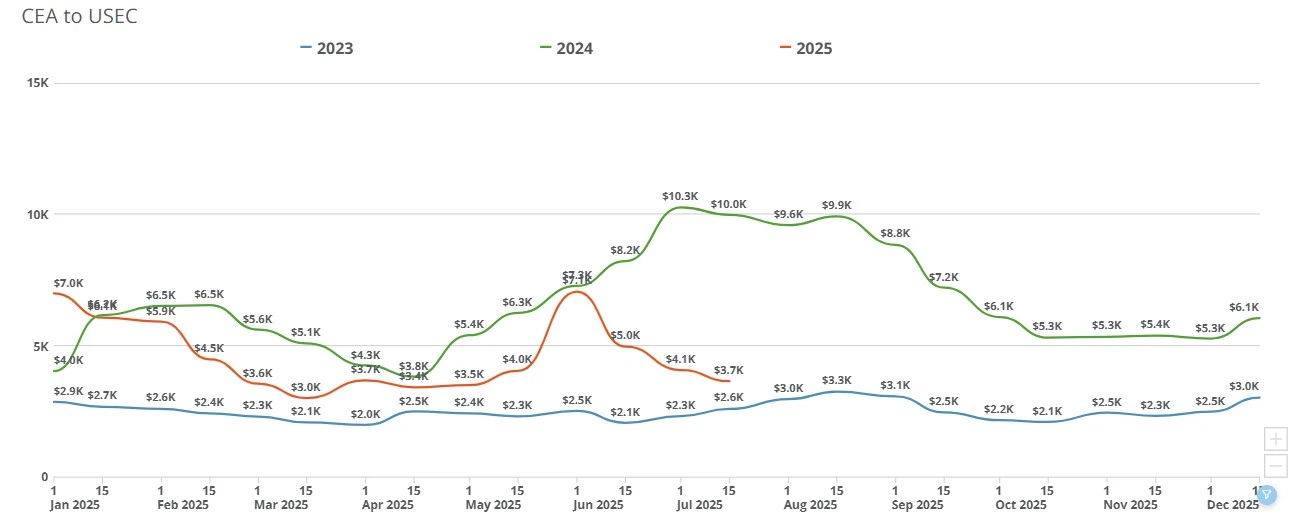

Transpacific ocean rates held largely steady this past week. China-US West Coast (CEA-USWC) rates were unchanged at approximately $1,800-$2,342/FEU, continuing three weeks of stability after the sharp post-June declines. China-US East Coast (CEA-USEC) prices fell 4% to $3,100-$3,950/FEU, marking the sixth straight week of declines. Daily rates have continued easing slightly since the latest tariff-related executive order went into effect on August 1st.

TrueFreight Index (TFX) is tracking the following rates for FEU as of August 1, 2025:

Week of August 4, 2025:

CEA/USEC 20FT $2542.41

CEA/USEC 40FT $3125.14

CEA/USEC 40HC $3125.14

CEA/USWC 20FT $1628.72

CEA/USWC 40FT $1990.42

CEA/USWC 40HC $1990.42

This Week Explained:

Tariff-Driven Uncertainty: The shifting timeline for new US tariffs and the latest August 7th “load-by” deadline has not sparked the same rush seen in April. Months of erratic policy changes and prior frontloading have dampened urgency among importers.

Weak Peak Season Demand: Import volumes surged earlier in the year when tariffs briefly eased in May, but have since fallen back. This year's peak season likely came and went in June, leaving demand at or below current levels.

Carrier Rate Discipline: Carriers have held rates from falling further by pulling capacity, but these measures only keep pricing flat rather than driving increases amid weak overall demand.

Market Fatigue: Importers appear less willing to chase every shifting tariff deadline, choosing to wait out uncertainty instead of committing to high-risk, last-minute moves.

Looking Ahead:

The outlook for August remains bearish. Volumes are expected to stay flat or dip further, while forwarders continue to face compressed margins. A possible 90-day extension of the current 30% tariff rate on Chinese goods could trigger a brief spike in bookings, but any surge would likely be short-lived given earlier frontloading and cautious importer behavior. A possible GRI could take place midway through August to return carriers to around break-even.

If no extension is granted and tariffs rise after August 12th, further disruption and delays in demand recovery are likely. With carriers already operating near break-even levels and importers reluctant to commit, the remainder of peak season appears muted, and rates are expected to hover near current levels unless a major policy shift jolts the market.

In the News:

The White House: Further Modifying the Reciprocal Tariff Rates, Annex 1 and Annex 2:

https://www.whitehouse.gov/wp-content/uploads/2025/07/2025ReciprocalTariffs_7.31.eo_.pdf and

https://www.whitehouse.gov/wp-content/uploads/2025/04/Annex-I.pdf

US Customs & Border Protection: GUIDANCE: Reciprocal Tariff Updates Effective August 7, 2025: https://content.govdelivery.com/bulletins/gd/USDHSCBP-3ec7b5e?wgt_ref=USDHSCBP_WIDGET_2

The Plain Bagel: No Deal for Canada - Now What? https://www.youtube.com/watch?v=dWUUavyfJh4

Subscribe to TFX for weekly updates: https://www.freightright.com/freight-right-rate-index

More News

Breaking Barriers: What the 2025 National Trade Estimate Report Reveals About Global Trade Frictions

Based on the latest insights from the 2025 National Trade Estimate Report, here’s a practical breakdown of the most pressing trade challenges across the United States’ top 10 goods trading partners.

ILA 2024 Strike: What Ports Are Affected & More

The International Longshoremen's Association began their strike October 1, 2024, affecting ports running along the east coast and Gulf regions of the United States. See what ports are affected and what this strike can mean for shippers.

Wait-and-See Grips Importers As Rates Remain Unchanged - TFX Update: wk. July 28st, 2025

As the deadline before reciprocal tariffs take place, the Trump administration continues to make deals with nations around the world. Importers are back to taking a wait-and-see approach while rates USWC and USEC remain unchanged.

International Economic Emergency Powers Act (Reciprocal Tariffs Act): Everything Importers, Exporters & Consumers Need to Know

On April 2nd, the Trump administration announced reciprocal tariffs aimed at 50 countries and a baseline 10% tariff on all imports to the US. Here are the latest tariffs the US plans to levy against other countries.

USWC Up & USEC Down, Supply and Demand Imbalances Persist & More - TFX Update: wk. July 21st, 2025

FEU & TEU rates change slightly week-over-week, importers that can afford to keep importing are continuning to do so while those that are hamstrung by tariffs are sidelined and the August 1st tariff deadline is one week away.

IEEPA Tariffs Update: What Importers Need to Know Now (January 2026)

Each day the Supreme Court moves closer and closer to a ruling for or against the Trump administration's IEEPA tariffs. See what Baker Tilly's Pete Mento advises importers do to get ready for any out come, what the possible outcomes could be and more.

The Future of Freight: The Independent Forwarder's Outlook

Our CEO sat with Freightos last week to discuss the future for independent freight fowarders.

Ocean Freight Rates Retreat as Tariff Uncertainty Freezes Import Demand - TFX Update wk. July 13, 2026

China-to-US ocean freight rates fell by about $1,000 this week as carriers lowered prices to stimulate demand. Read the latest Freight Right market update on CEA to USWC and USEC rates, tariff uncertainty, and the outlook for the remainder of the 2026 pea

Executive Expands Tariff Powers, Streamlines Trade and Security Framework

In a 7–4 ruling on August 29, 2025, the US Court of Appeals found President Trump exceeded his authority under IEEPA by imposing broad reciprocal tariffs. The decision is stayed until Oct 14, giving the administration time to appeal to the Supreme Court.

China-US Ocean Rates Hold Steady at $3K/$4K Baseline Ahead of Threatened June Spikes - TFX Update wk. May 25, 2026

Ocean freight rates hold steady, but massive June GRIs loom. Discover how carrier blank sailings and terminal capacity constraints are driving up transpacific shipping costs.