The Lead:

This week moved the US-China trade fight decisively onto the water. On Oct 14, Washington and Beijing both activated reciprocal port-entry fees that target each other’s shipping ecosystems, adding direct costs for carriers (with detailed carve-outs and five-voyage annual caps) and potential pass-through costs for cargo owners. At the same time, product-specific US tariffs (e.g., wood products and furniture) kicked in, and markets braced for Nov 1 measures, 25% on medium/heavy trucks and an additional 100% tariff on all Chinese imports alongside new export-control moves. Overlapping this, China’s rare-earth export curbs prompted the EU to coordinate with the US/G7 on critical-mineral resilience. Net-net: policy risk rose across ocean shipping, manufacturing inputs and downstream consumer goods, with logistics and sourcing teams facing immediate fee exposure at ports and a near-term step-up in tariff and licensing complexity.

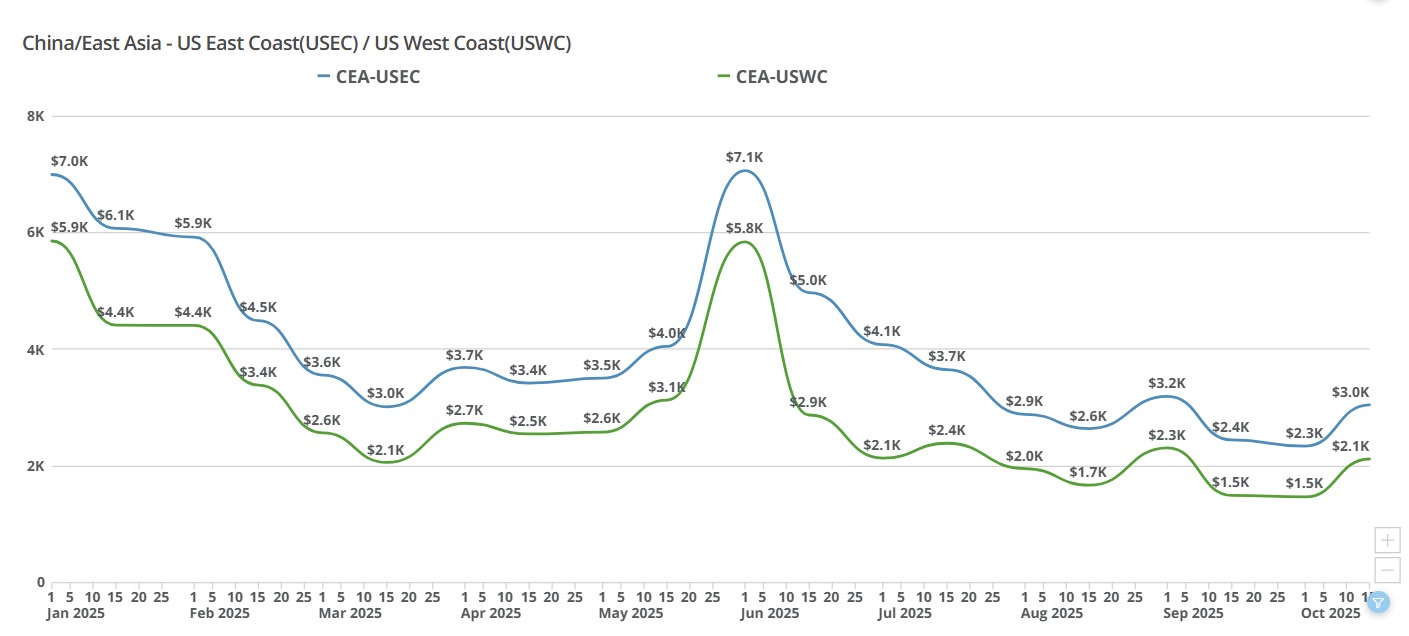

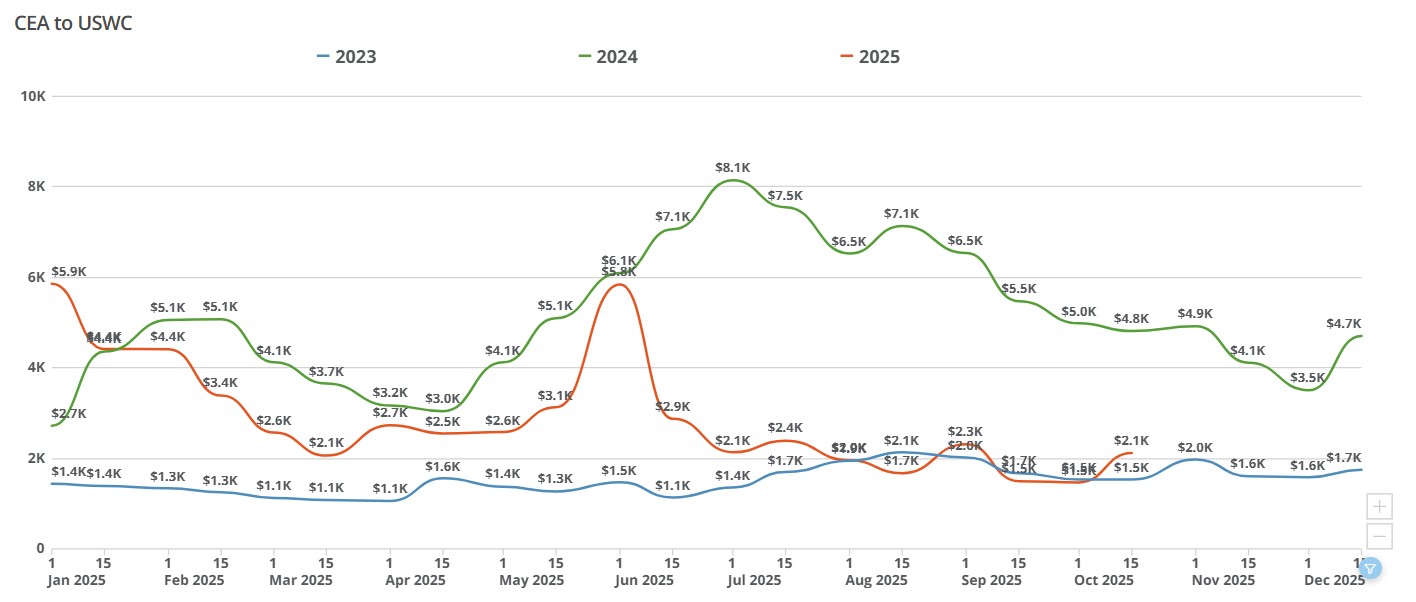

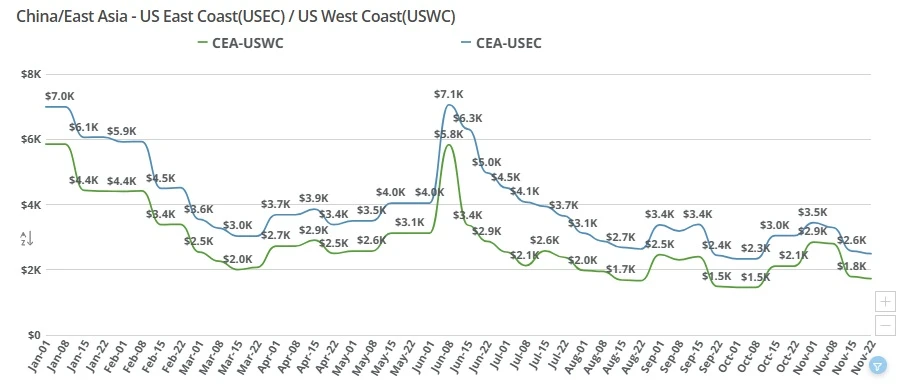

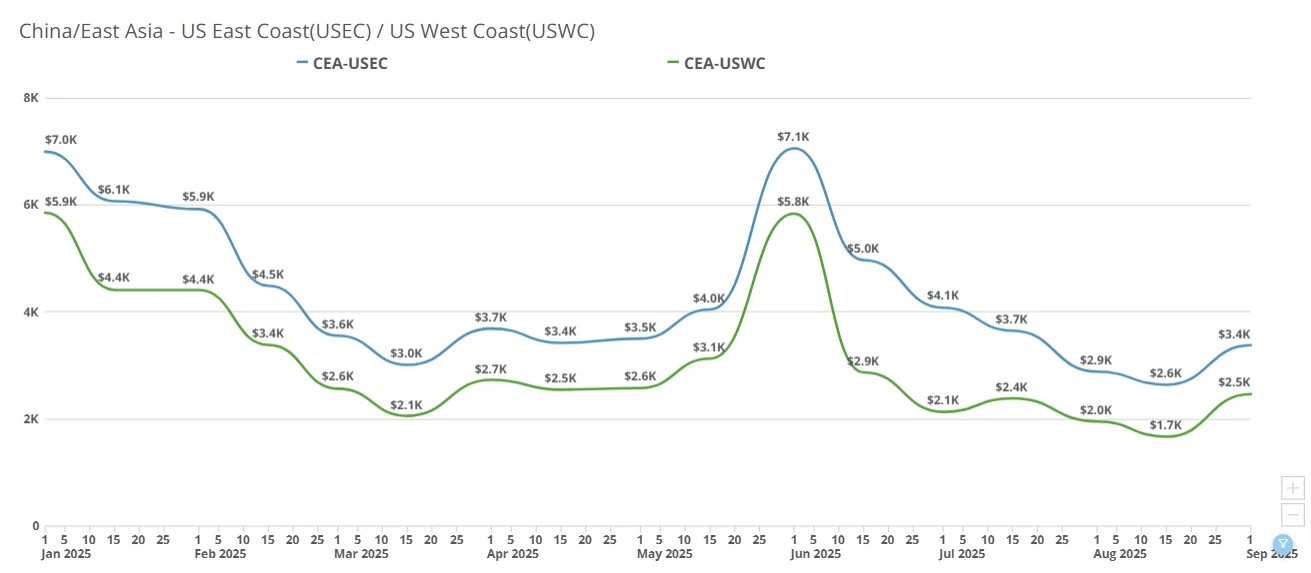

CEA to USWC (China to US West Coast): Spot climbed roughly $700–$900 w/w to about $2,000–$2,100/FEU on mid-month GRIs and acute space tightening.

CEA to USEC (China to US East Coast): Spot rose about $700–$800 w/w to roughly $3,000–$3,100/FEU, but is unlikely to hold given transit times that miss the Nov 1 tariff risk window.

Week of October 13, 2025:

CEA/USEC 20FT $2145.08

CEA/USEC 40FT $2659.38

CEA/USEC 40HC $2659.38

CEA/USWC 20FT $1403.92

CEA/USWC 40HC $1751

CEA/USWC 40FT $1751

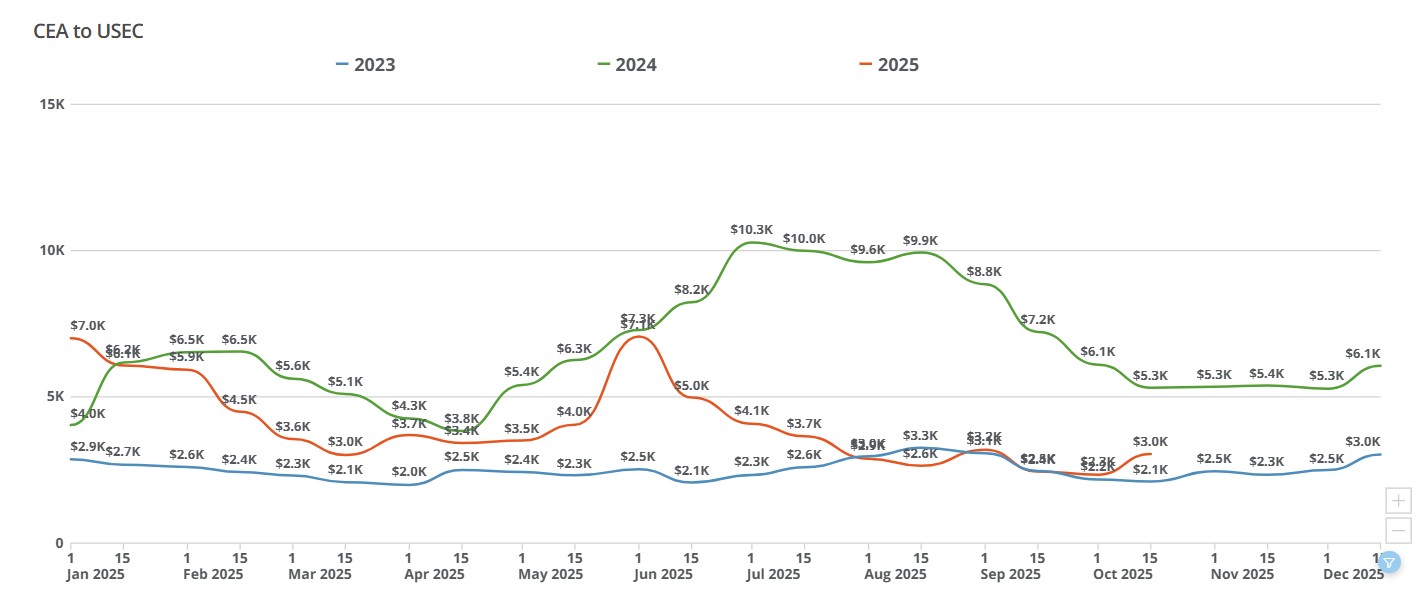

Aggressive capacity pulls/blank sailings: Carriers have removed a large share of vessels from rotations, overbooking the remaining sailings and firming GRIs.

Tariff-driven rush (timing matters): Importers trying to land before a potential 100% China tariff on Nov 1 drove short-haul demand to the West Coast; East/Gulf routes can’t physically arrive in time.

Mid-month rate reset: New half-month carrier rate sheets are kicking in, aligning with the latest GRIs.

Behavioral lag: Many shippers are only now digesting the tariff headlines; the immediate squeeze is concentrated in this few-day window.

The next two weeks are going to be ones to watch. For USWC elevated rates are likely to hold through this week as last-minute cargo chases the only lane that can still arrive in time; modest easing is possible next week if bookings pause post-deadline. For USEC, this week’s bump looks fragile; with arrival deadlines missed, expect faster giveback as shippers step back and carriers reassess GRIs/PSS on softer near-term demand.

With capacity trimmed and policy headlines in flux, expect choppy, headline-sensitive pricing into late October, tight in the near term, then cooling if the tariff rush fades.

The timing of this week’s GRI combined with the sudden announcement of 100% tariffs on Chinese imports on top of existing tariffs placed on China is also something to be mindful of. The observation among those in the industry is the speed of the tariff announcement, specifically, will take many importers by surprise as the announcement was made late last week going into the weekend. Importers will have about 2 weeks to claim carrier space amidst extensive blank sailing and limited space to secure their shipments so that they arrive in the US by November 1st or be faced with the 100% tariff.

Others in the industry, including ourselves, notice that carriers benefit the most from this artificial demand creation and importers are left shouldering higher costs.

Following the end of the de minimis exemption in May, China-US air freight volumes remained soft through late September.

E-commerce slowdown: Major platforms such as Temu and Shein significantly reduced shipment volumes.

Express channel resilience: Other air-express providers held steady or showed modest growth.

Traditional B2B decline: Forwarders and shippers moving standard commercial cargo saw a continued drop in bookings.

Rates and capacity: Overall demand weakness pushed spot rates down to about $3-$4/kg to LAX and ORD, and $4-$5/kg to JFK. Airlines attempted to stabilize yields through select flight cancellations and tighter capacity management.

Air rates rebounded entering this week, driven by pre-holiday shipments and capacity constraints.

Golden Week effect: Demand surged ahead of China’s National Day “Golden Week”, with the 2025 peak season arriving roughly two weeks later than usual. Rates climbed to around $4.5–$5.5/kg to the US

Apple charters tightening space: Apple’s charter operations during Weeks 40–42 further strained available lift. Several dedicated freighter services, such as K4 HFE-JFK, were cancelled, narrowing supply and pushing rates to roughly $5–$6/kg.

With charter flights resuming this week, the market was expected to normalize-until the October 10 announcement of potential 100% US tariffs reignited demand.

We and our partners are expecting immediate increases seen from express channels, traditional B2B exporters, and Apple-related shipments. Current spot levels are averaging $6.0–$6.5/kg and still climbing.

Air freight rates are projected to remain elevated through the end of October, supported by urgent cargo movements ahead of the possible tariff deadline. Market direction for November will hinge on the final tariff decision, with either a brief cooling if rates stabilize or further escalation if new measures take effect.

5

This week’s Big Number is 5, China’s new “special port service fee” on US-linked vessels is capped at five voyages per year per ship.

NBC News: UPS is 'disposing of' US-bound packages over customs paperwork problems: https://www.nbcnews.com/business/business-news/ups-delay-customs-tariffs-packages-destroyed-rcna236607

WSJ: America’s Manufacturing Resurgence Will Be Powered by These Robots: https://logistics.cmail19.com/t/d-l-ggidjy-driitikdhk-yh/

Ars Technica: Not a game: Cards Against Humanity avoids tariffs by ditching rules, explaining jokes: https://arstechnica.com/culture/2025/10/to-avoid-tariffs-cards-against-humanity-becomes-information-material-not-a-game/

WSJ: Sharpie Found a Way to Make Pens More Cheaply - By Manufacturing Them in the US: https://www.wsj.com/business/sharpie-us-production-cost-cutting-d9ba2abd

Ocean freight rates double for USWC and USEC as carrier capacity cuts trigger severe space shortages and rolled cargo. Read the latest weekly freight market update on rising spot rates, premium expedited shipping surges, and the June GRI outlook.

Late-June front-loading has triggered a severe transpacific space crunch. Discover how carrier rate hikes are driving ocean freight costs to new heights as shippers scramble for limited vessel capacity.

China-US air freight rates spike above $7.50/kg amid tariff fears and tight capacity to JFK, ORD, and LAX.

Ocean freight rates skyrocket past $6,000 to USWC and $7,000 to USEC. Discover how carrier blank sailings, space deficits, and tariff front-loading are driving this early peak season crunch.

Transpacific ocean freight rates dropped sharply this week as weak import demand and the Thanksgiving holiday slowdown pushed China–US West and East Coast spot prices to new lows. Get the latest market drivers and outlook.

Outer space is the newest export frontier, where rockets and satellites count as high-tech cargo, triggering a bureaucratic maze of customs, export controls, and duty drawbacks. As the space economy grows, regulators face challenges from orbital warehouse

The Panama canal is experiencing lower water levels as a result of a drought exacerbated by El Nino. The results of this drought have implications for all sizes of shippers around the world but particularly for small to medium sized shippers that are in a

Carriers use aggressive blank sailings to maintain China-US rates at $2,700, while shippers withhold volume in anticipation of a May price drop. Explore the impact of fuel surcharges and booking rolls on your supply chain.

The International Longshoremen's Association began their strike October 1, 2024, affecting ports running along the east coast and Gulf regions of the United States. See what ports are affected and what this strike can mean for shippers.

Ocean freight rates from China to the US spiked this week, with carriers testing higher levels before Golden Week. Importers weigh shipping now or waiting.