- Home

- >

- News

- >

- Tariff Fears Send China-US Air Freight Rates Soaring Past $7.50/kg - TFX Update wk. October 20, 2025

Tariff Fears Send China-US Air Freight Rates Soaring Past $7.50/kg - TFX Update wk. October 20, 2025

The Lead:

Events in global trade fell into 3 buckets this week. The first is best described as escalation. China extended its export-controls on rare earths, technologies and production inputs, signalling a further entrenchment of supply-chain leverage. The US responded by considering export restrictions on software-embedded goods bound for China and by continuing its tariff expansion (e.g., on timber/lumber). These moves reflect a growing shift from tariffs alone to “technology-trade” and export-control levers.

The second major theme was growth and international trade. Institutions such as the WTO and IMF highlighted that while trade volumes were holding up in the near term, growth prospects were softening and the risk of protectionist fragmentation was elevated. The IMF’s advice to Asian economies to strengthen regional trade ties underscores how nations are adjusting to a more volatile trade regime.

The third group of events was around strategic alliances. Evident in Germany’s trade pivot to China, and the breakdown in US-Canada trade talks, the period saw countries responding to US tariff pressure by diversifying away from the US-centric order. For exporters (like you, in big/bulky DTC goods), this signals that sourcing, routing and market selection need to be more dynamic, and that trade-policy risk is not just about tariffs but changing trade-flows and partner dependencies.

This Week’s Ocean, Air & Freight Markets

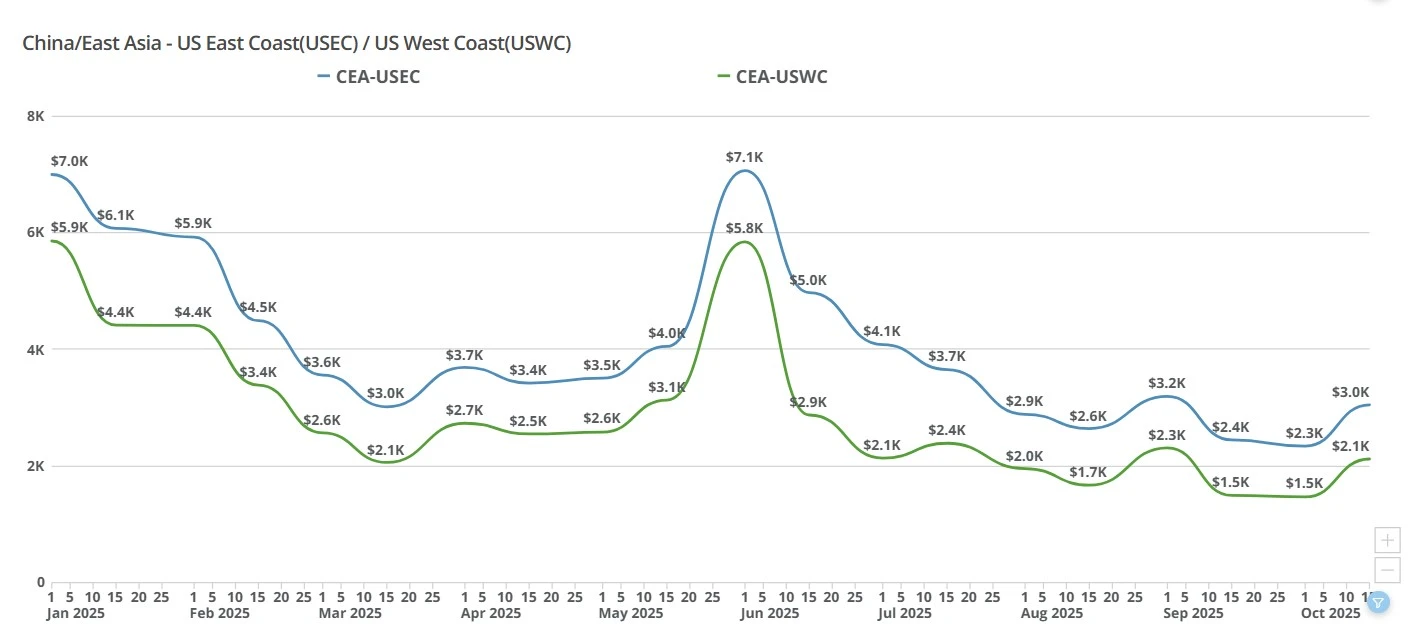

China-US Ocean Freight Market:

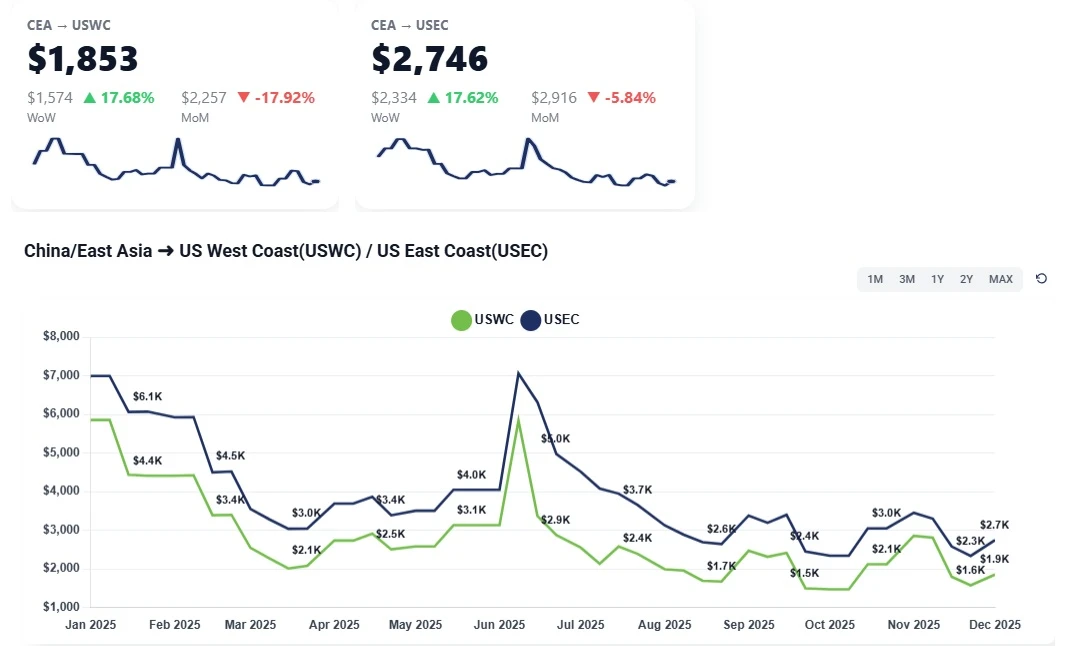

CEA to USWC (China to US West Coast): Spot climbed roughly $700–$900 w/w to about $2,000–$2,100/FEU on mid-month GRIs and acute space tightening.

CEA to USEC (China to US East Coast): Spot rose about $700–$800 w/w to roughly $3,000–$3,100/FEU, but is unlikely to hold given transit times that miss the November 1st tariff risk window.

This Week Explained:

Pre-emptive GRIs and firm carrier posture: Most carriers are "holding the line" on October hikes and floating a fresh November 1st +$800–$900/FEU increase, keeping the spot market tight despite muted booking activity.

Supply cuts via blank sailings: Our partners and team have estimated that carriers have pulled ~40–50% of rotations in some strings, creating rollovers and constraining space. The result is a classic case of artificially restricting supply.

Importer pause ahead of tariff decisions: Many shippers are waiting a week to see outcomes from high-level US–China talks; missing a favorable outcome could mean cargo landing in early November facing significantly higher duties, so some are sidelined despite higher freight costs.

Air cargo spike confirms deadline pressure: With ocean becoming costlier/tighter, CEA to US air has surged from “high-$4s/kg” to roughly $7.30/kg, reflecting a short-term rush to beat end-of-month timing.

From summer troughs to autumn firmness: Compared with late July, when FBX showed USWC ~$2.3k and USEC ~$4.1k, the current step-ups mark a swing back to carrier control, aided by reduced capacity and GRI discipline.

Looking Ahead:

Over the next 2-4 weeks, we’re expecting a stop-go oscillation: carriers press another hike around November 1st, some urgent importers pay up, then bookings dip as others wait, setting up a brief fade in late November if volumes stall.

Carriers appear to be staging multiple smaller hikes (Oct, Nov, then another in January) rather than one big January jump, both to avoid regulatory scrutiny and to capture demand around pre-Lunar New Year pull-forward.

Currently, for USWC, we're seeing $1.9–2.0k now with a risk toward $2.7–3.1k if November 1st tariff sticks. For USEC, we're currently seeing around $2.85–3.0k now with a risk toward $3.8–4.1k with the same risks involved with November 1st tariffs.

Any tariff outcome shift (extension vs. escalation) or capacity add-backs could quickly reroute this path; conversely, continued blank sailings would cement higher floors through year-end.

China-US Air Freight Market:

The China-US air freight market has entered a period of acute volatility. Rates have surged above $7.50/kg, with space nearly full through early next week on most South China-US lanes. This sharp rise is driven by expectations of November tariff hikes, disruptions in ocean freight, and an influx of high-density cargo, particularly to JFK and ORD. Competition for uplift is fierce, and the scramble is expected to peak around October 29 as shippers rush to clear cargo before new duties take effect.

This Week Explained:

Tariff-driven preloading: Anticipation of additional US tariffs in November has triggered a wave of front-loaded exports. Major manufacturers, including Apple and Tesla, are pushing urgent shipments out of China to avoid the next duty cycle, consuming vast amounts of uplift capacity.

Ocean freight disruptions shifting cargo to air: A series of blank sailings in October and new port surcharges on Chinese vessels have worsened sea reliability. With lead times expanding and confidence eroding, some high-density commodities (like aluminum coils and industrial cabinets) are being diverted to air, tightening space and pushing rates higher.

Restocking pressure after the Novelis plant fire: The September 16 fire at Novelis’ New York facility, one of the largest aluminum recyclers in the US, has accelerated replacement imports. These shipments, often heavy and voluminous, are flowing into ORD and JFK, absorbing capacity and further distorting regional rate balances.

Regional capacity disparities:

JFK & ORD: Capacity nearly full through early next week. South China to JFK/ORD: $6.50–$7.50/kg; PVG to JFK/ORD: ~$6.50/kg.

LAX: Some capacity relief due to added flights, yet South China to LAX remains elevated at ~$7.00/kg, while PVG to LAX trails by $0.50–$1.00/kg.

Looking Ahead:

We’re expecting that the current rate of importer activity will likely culminate just before November, as shippers race to finalize movements ahead of potential tariff changes. After that, a brief cooling could occur if tariffs are delayed or softened.

If the full set of November tariffs materializes, expect rates to remain elevated or climb further, with carriers potentially repricing above $8/kg for priority space. A partial or postponed rollout, by contrast, could trigger rate normalization toward mid-$6s/kg by mid-November.

Additionally, even if demand pauses, ocean instability, restocking demand, and pre–Lunar New Year exports suggest a high floor for air freight rates well into December. Capacity relief is unlikely until post Chinese New Year.

This Week’s Big Number

This week’s Big Number is $35 billion, the estimated cost to global companies of US tariffs to date.

In the News:

Sourcing Journal: Red Sea Return Could Flood Europe’s Ports With Cargo: https://sourcingjournal.com/topics/logistics/red-sea-suez-canal-return-europe-port-congestion-sea-intelligence-cargo-ocean-carriers-freight-rates-israel-hamas-1234786278/

Container News: The weaponization of flag-hopping as a new trend in shipping industry: https://container-news.com/the-weaponization-of-flag-hopping-as-a-new-trend-in-shipping-industry/

Container News: Japan bets on shipbuilding revival amid China’s market dominance: https://container-news.com/japan-bets-on-shipbuilding-revival-amid-chinas-market-dominance/

More News

Navigating LAX Air Cargo: Freight Right's Expertise as Customs Broker

Freight Right leads in LAX customs brokerage, managing over 100K tons of air cargo annually. Discover our role in LAX’s cargo efficiency and compliance.

Ocean Spot Rates Rise $700–$900; Air Freight Climbs on Apple Charters and Tariff Rush - TFX Update wk. October 13, 2025

Transpacific ocean and air rates jump as carriers pull capacity, Apple charters tighten space, and shippers rush to beat U.S. tariff deadlines

China–US West and East Coast Rates Hold Flat After Short-Lived December Rate Spike - TFX Update wk. December 1, 2025

Weekly ocean freight update on China–US West and East Coast lanes as an early December GRI fades, leaving spot rates near November levels amid weak demand.

Ocean Freight Rates Double Since March as Carriers Aggressively Squeeze Capacity - TFX Update wk. May 18, 2026

Ocean freight rates double for USWC and USEC as carrier capacity cuts trigger severe space shortages and rolled cargo. Read the latest weekly freight market update on rising spot rates, premium expedited shipping surges, and the June GRI outlook.

China-U.S. Ocean Freight Steadies as Carriers Prepare $1,000 November GRI - TFX Update wk. October 27, 2025

U.S-China trade deal specifics; transpacific freight rates hold steady as carriers plan a $1,000 GRI for Nov. 1, easing fears after tariff threats and muted seasonal demand.

China–US Ocean Freight Market Holds Firm, but Promotional Rates Gain Traction - TFX Update wk. June 22, 2026

China–US ocean freight rates remain elevated, with CEA to USWC pricing above $6,000 while promotional carrier deals help some shipments move lower. Learn what is driving rates and what to expect heading into July.

Importers Race Against July Tariff Deadlines, Throwing Supply Chains Into Chaos - TFX Update wk. June 8, 2026

Ocean freight rates skyrocket past $6,000 to USWC and $7,000 to USEC. Discover how carrier blank sailings, space deficits, and tariff front-loading are driving this early peak season crunch.

Carriers Hold Firm on Fuel Surcharges Despite Emerging US-Iran Peace Plans - TFX Update wk. June 15, 2026

Transpacific ocean freight rates soared past $6,000 to the USWC and hit the mid-$7,000s to the USEC. Discover how front-loading and severe space constraints are driving this week's market update.

US Slaps 10% Lumber and 25% Furniture Tariffs: Impact on Housing, Trade, and Consumers

The U.S. will impose 10% tariffs on lumber and 25% on furniture starting October 14, 2025, a move set to impact housing costs, supply chains, and trade relations.

Digital Air Freight: What You Need to Know about E-bookings

This blog explores digital air freight and how e-bookings provide a more efficient and faster way for logistics professionals to make connections.