- Home

- >

- News

- >

- Shippers Continue to Confront Higher Costs While Freight Forwarders Face Fierce Competition - TFX Update wk. September 8, 2025

Shippers Continue to Confront Higher Costs While Freight Forwarders Face Fierce Competition - TFX Update wk. September 8, 2025

The Lead:

This week was dominated by Washington’s tariff legal saga and a calibrated softening at the margins. The White House moved to fast-track a Supreme Court appeal to keep emergency tariffs in place, even as it carved out zero-duty lanes for “aligned partners” and priority inputs beginning Sept. 8. Abroad, policymakers reacted on two fronts: defensive impact assessments (India’s finance team flagging a 0.5-0.6% GDP hit) and diversification plays (Beijing pushing an upgraded ASEAN pact). Europe’s trade data offered an early read-through of U.S. measures with weaker German exports. Net-net, the global trade stance remains restrictive, but with selective exemptions and regional deals emerging as pressure valves.

On Markets & Rates:

Rates decreased very slightly week-to-week. Last week’s GRI followed through and gave the spot market an expected shock in the form of container prices going up between $800-900 dollars. Rates saw about a 1% decrease. The decrease was expected as are decreases throughout the month of September. The time to look at most closely will be next week as that will help provide insight into the direction of the rest of September before going into Golden Week and the off-season.

Competition is getting increasingly fierce between freight forwarding companies. Forwarders, especially those dealing with SMBs, are fighting for business wherever they can get it as the pool of importers willing to continue to import with spot costs almost $1,000 more expensive than August and tariffs remains small but continues to shrink. Partners are reporting it’s increasingly common to take jobs at-cost or with extremely small margins, often between $25-75. We have not yet reached the point where negative margins are common place but it does not seem far away.

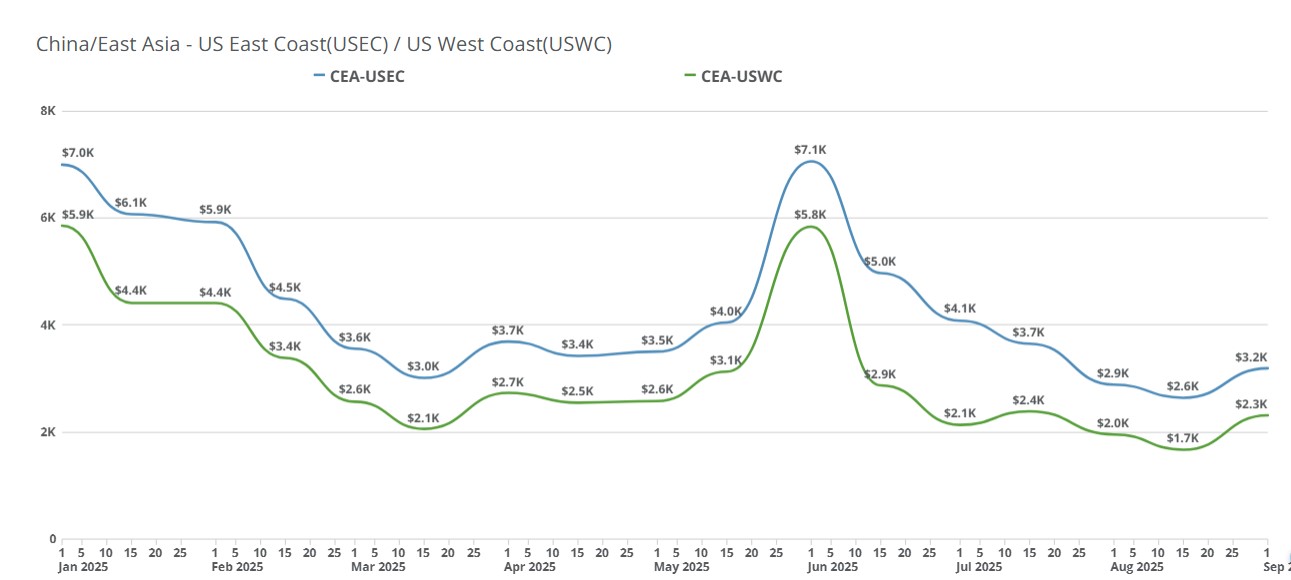

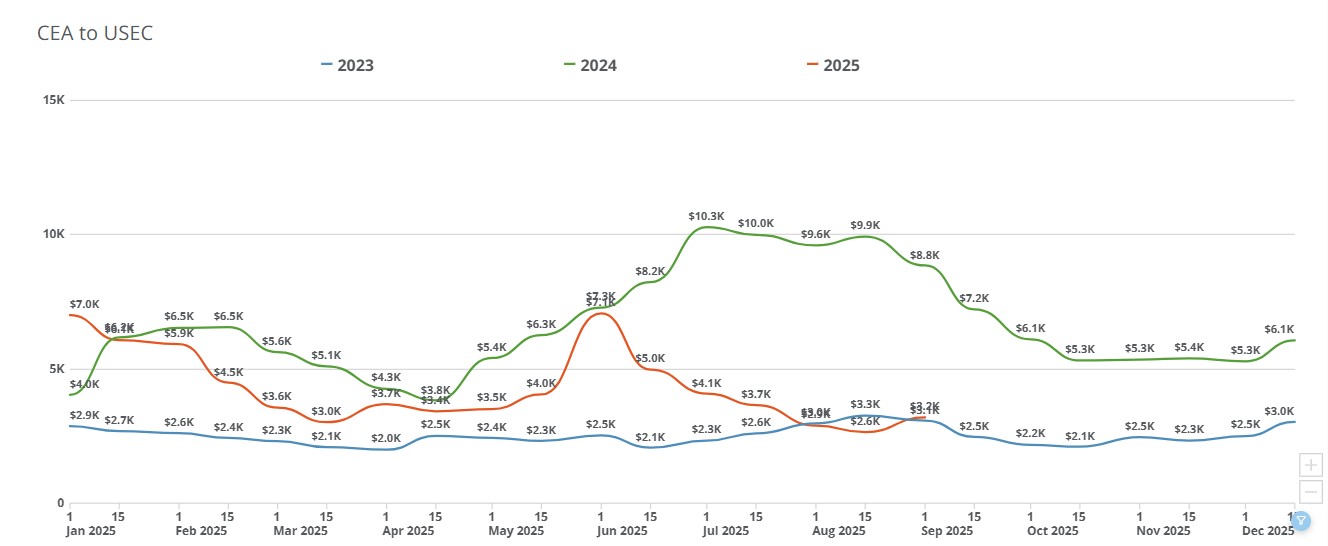

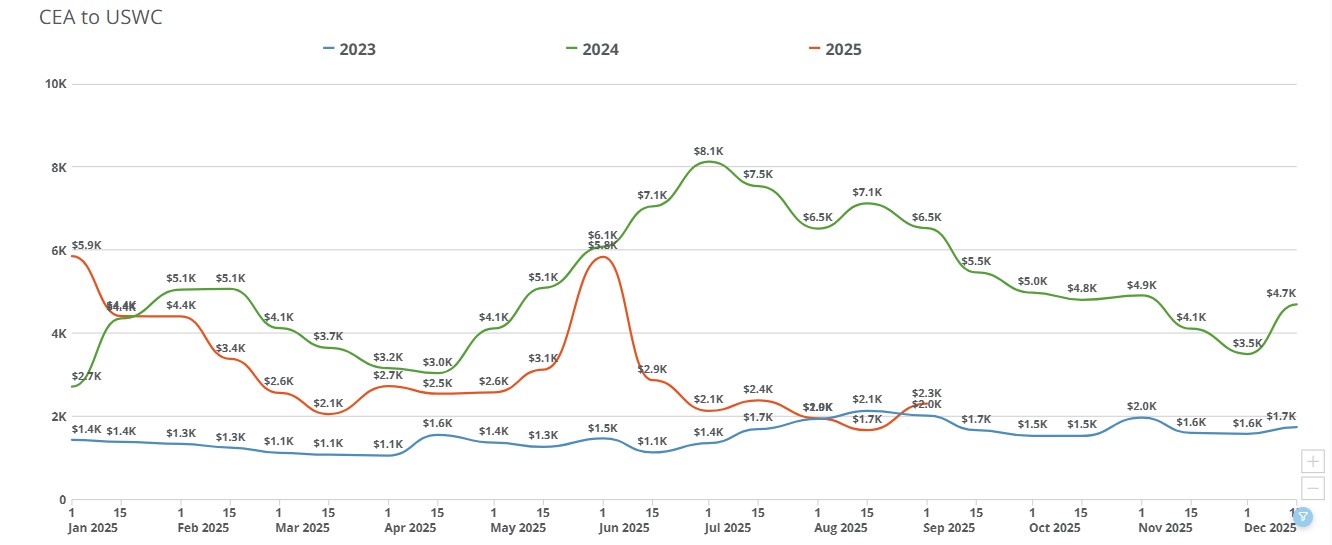

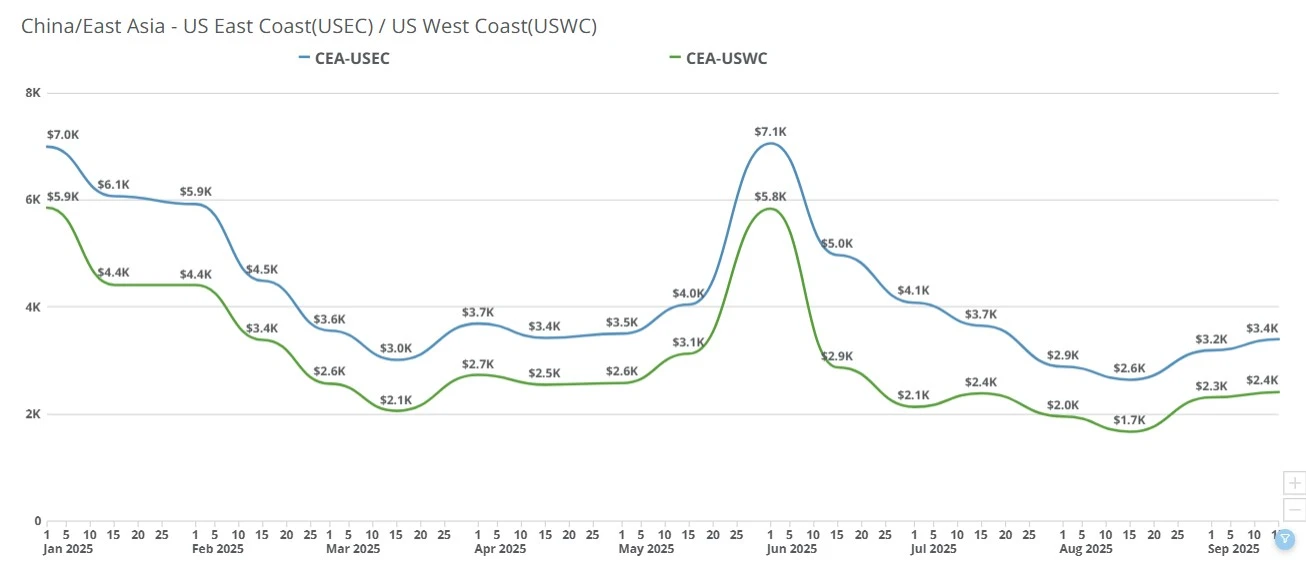

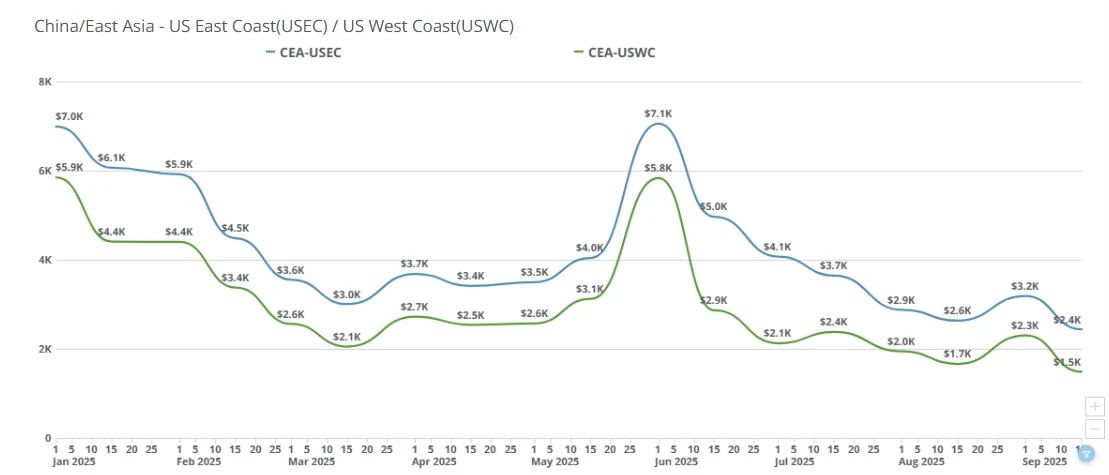

CEA/USEC currently range between $2200-2700. CEA/USWC currently range between $1800-$2400

Week of September 8, 2025:

CEA/USEC 20FT $2633.8

CEA/USEC 40FT $3192.4

CEA/USEC 40HC $3192.4

CEA/USWC 20FT $1859.95

CEA/USWC 40HC $2321.07

CEA/USWC 40FT $2312.23

Week of September 1, 2025:

CEA/USEC 20FT $2787.96

CEA/USEC 40HC $3379.28

CEA/USEC 40FT $3379.28

CEA/USWC 20FT $1983.46

CEA/USWC 40FT $2467.17

CEA/USWC 40HC $2478.19

In the News:

WSJ: Supreme Court Agrees to Fast-Track Trump’s Tariff Appeal: https://www.wsj.com/us-news/law/supreme-court-agrees-to-hear-trumps-tariff-appeal-330b62ca?mod=djemlogistics_h

ShippingWatch: Trump wants 100 percent EU tariffs on China and India to pressure Russia: https://shippingwatch.dk/miljo_og_politik/article18522192.ece

NikkeiAsia: Tariffs to spur US partners to diversify, ex-negotiator says: https://asia.nikkei.com/economy/trade-war/tariffs-to-spur-us-partners-to-diversify-ex-negotiator-says

Marketplace: Quarterly demand for industrial warehouses sees first drop in 15 years: https://www.marketplace.org/story/2025/09/05/why-warehouse-demand-dropped-for-the-first-time-in-15-years?_hsenc=p2ANqtz-90iTOU4ngZHsjz5Jo0fCapYNpFpPM49eOSHb8oZvp7orBibI7vd6LiKkUFKfucgF9MapPiYfeO3Yd5enNal61Fyqg0rQ&_hsmi=379833655

Subscribe to TFX for weekly updates: https://www.freightright.com/freight-right-rate-index

More News

Carriers Rollback September's GRI and Competition Among Forwarders Heats Up - TFX Update wk. September 15, 2025

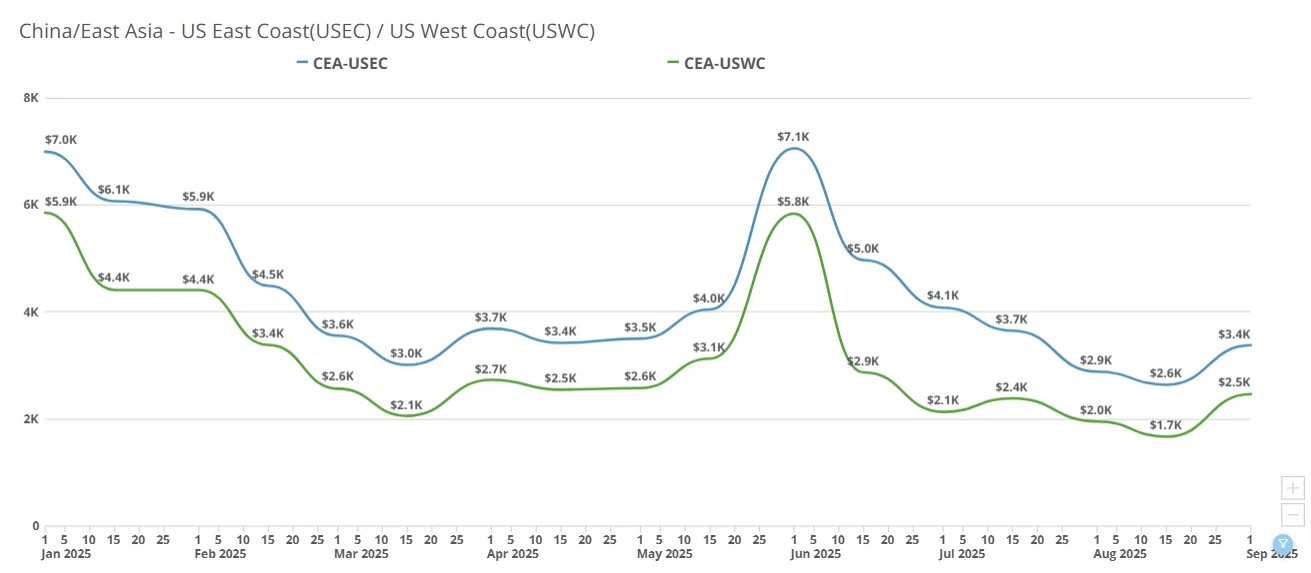

China–US freight rates spiked up to $900 to start September but,in a rare move, promptly rolled back to pre-GRI amounts this week to entice bookings.

Spot Prices Ease on CEA to USWC, CEA to USEC; Forwarders Cut Margins to Win Cargo - TFX Update wk. September 22, 2025

China–US ocean spot rates eased WoW as early-September GRIs faded. USWC nears trough, USEC softens, and fierce forwarder pricing persists ahead of Golden Week.

CEA-USWC and USEC Rates Surge $800-$900 Amid Carrier GRIs - TFX Update wk. September 1, 2025

Ocean freight rates from China to the US spiked this week, with carriers testing higher levels before Golden Week. Importers weigh shipping now or waiting.

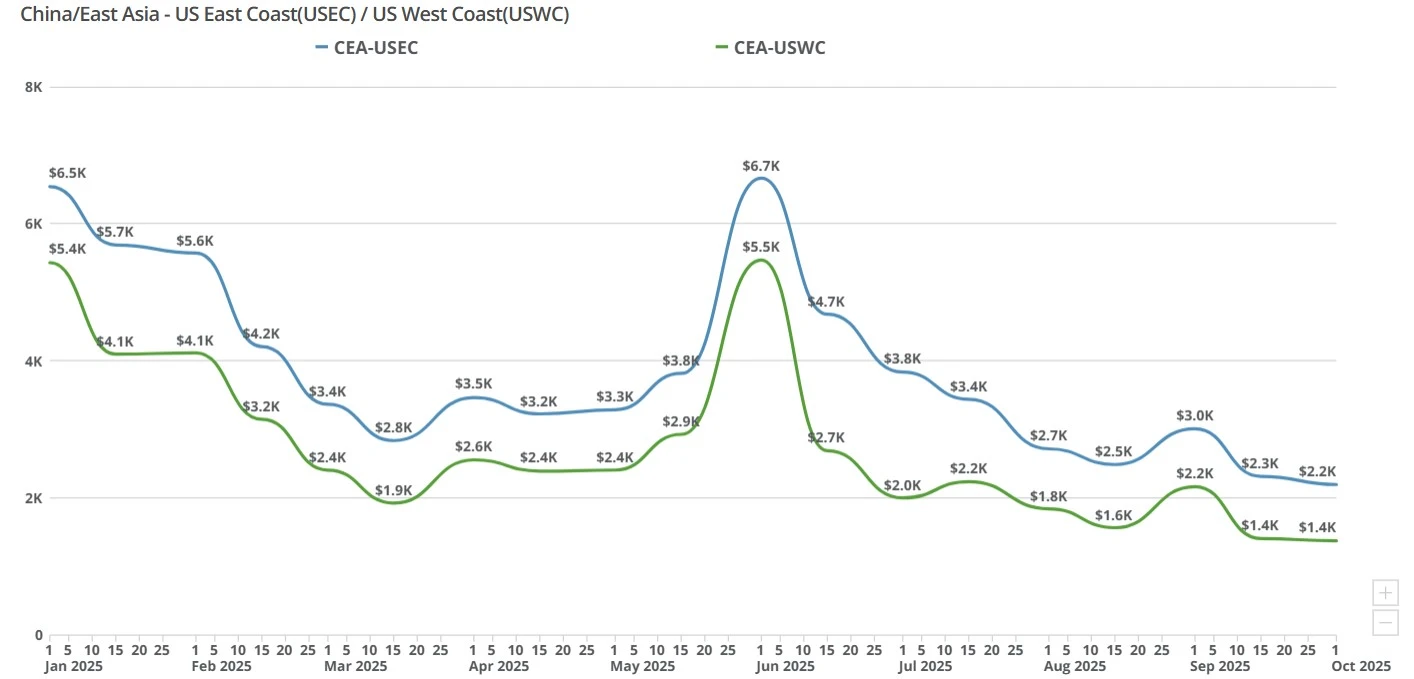

Transpac Spot Rates Slip as Golden Week Quiet Hits; USWC Near $1.3k/FEU - TFX Update wk. September 29, 2025

China-US spot rates dipped again, with USWC near $1,300/FEU. Golden Week slowdowns and tariff drag curb demand as carriers weigh blank sailings.

Last-Minute Sailing Cancellations Push April Cargo into May - TFX Update wk. April 20, 2026

Carriers use aggressive blank sailings to maintain China-US rates at $2,700, while shippers withhold volume in anticipation of a May price drop. Explore the impact of fuel surcharges and booking rolls on your supply chain.

Flat Week for Ocean Freight as China’s Golden Week Pauses Trade Flows - TFX Update wk. October 6, 2025

China-U.S. freight rates stayed flat this week as Golden Week factory closures paused bookings and kept ocean freight markets calm.

Shippers Face a Total Standstill in Transpacific Trade - TFX Update wk. February 23, 2026

Ocean rates remain frozen at $1,400-$1,600 to the USWC as the Lunar New Year shutdown halts all Chinese logistics. Discover why the market is at a standstill and what to watch for in March.

2023 Panama Canal Drought: What Small & Medium-Sized Shippers Need To Know

The Panama canal is experiencing lower water levels as a result of a drought exacerbated by El Nino. The results of this drought have implications for all sizes of shippers around the world but particularly for small to medium sized shippers that are in a

Congestion at Yantian port may mean even higher rates on transpacific

Rising COVID cases partially closes down one of the world's busiest ports, what does that mean for freight?

China-U.S. Ocean Freight Steadies as Carriers Prepare $1,000 November GRI - TFX Update wk. October 27, 2025

U.S-China trade deal specifics; transpacific freight rates hold steady as carriers plan a $1,000 GRI for Nov. 1, easing fears after tariff threats and muted seasonal demand.