Blank Sailings and Rollovers Dominate May Freight Market - TFX Update wk. May 4, 2026

The Lead:

The turn of the month in May 2026 signaled a definitive move toward a centralized trade architecture in the US and a multipolar landscape elsewhere. The provisional launch of the EU-Mercosur agreement represented a major victory for European industrial and agricultural sectors, providing a vital hedge against rising US protectionism. Simultaneously, China’s total elimination of tariffs for 53 African nations solidified a new South-South trade axis designed to secure resources outside of Western influence. While the US formalized its "America First” agenda, using 100% pharma duties and 15% surcharges to force domestic onshoring, the IMF warned that these fragmented trade policies are creating fault lines that threaten to stall global growth for the remainder of the year.

This Week’s Ocean, Air & Freight Markets

China-US Ocean Freight Market:

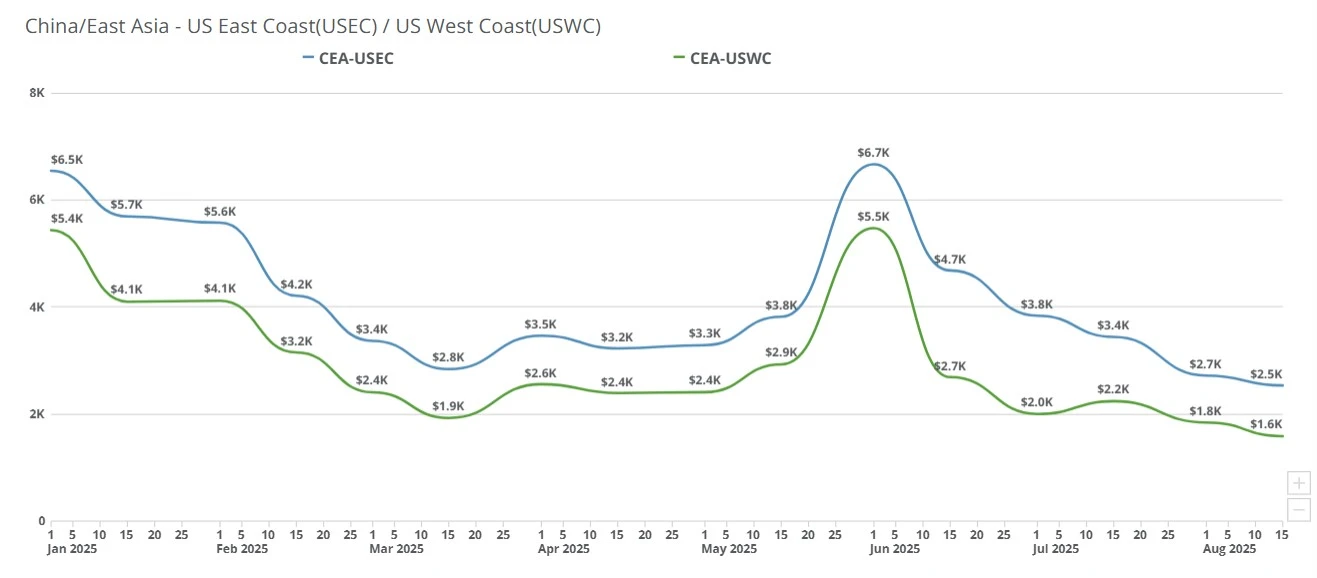

The ocean freight market is currently characterized by relative rate stability compared to the end of April, despite significant operational shifts.

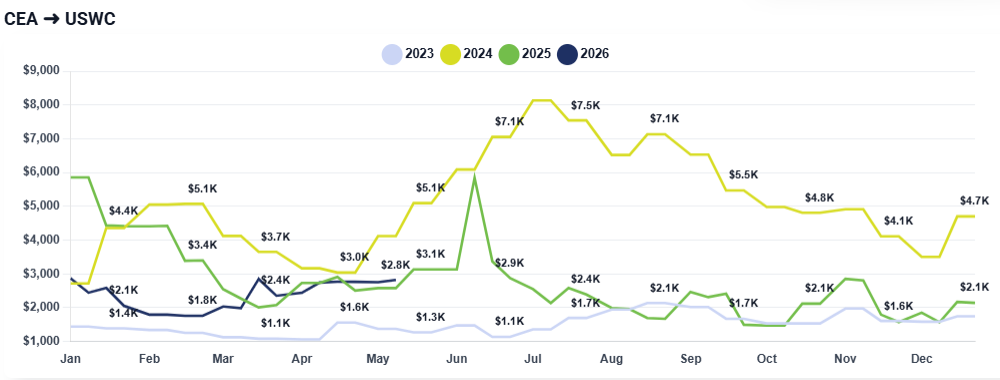

CEA to USWC: rates are still holding at approximately $2,600-$2,800 range per FEU.

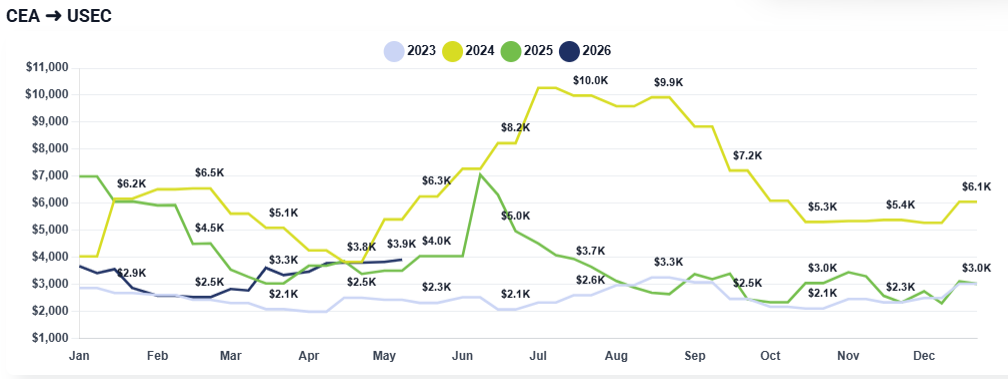

CEA to USEC: Rates to USEC on the other hand, are hovering between $3,700-$3,900.

These figures include the implementation of Emergency Fuel Surcharges that kicked in at the start of the month.

Freight Right’s Lowest Rate indicators are finding that importers can find spot rates as low as $2,500 from China to US West Coast and $3,550 from China to US East Coast. Talk to your freight forwarder about options available to you.

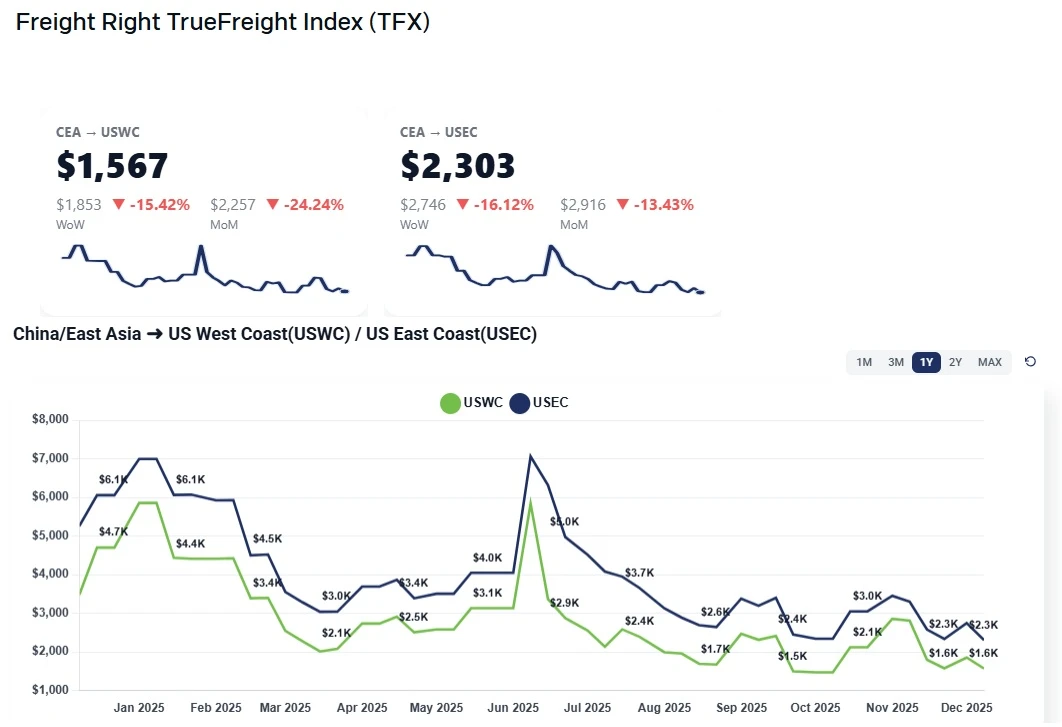

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

What Happened This Past Week

Rollover Risks: While space is technically available to book, the reduction in vessel capacity means a high percentage of shipments are being rolled to subsequent weeks.

Operational Overloading: To compensate for fewer ships, carriers are overloading active vessels, sometimes forcing unplanned discharges at intermediate ports like Busan to lighten the load for the transpacific crossing.

Labor Day Holiday: The market experienced a lull in movement this week due to the Labor Day holiday in China, with many businesses closed until May 6th.

Blank Sailing Surges: Carriers are aggressively pulling vessels out of circulation, with blank sailings occurring at a higher frequency than in April.

Looking Ahead:

The outlook for the remainder of May suggests continued volatility in transit reliability even if rates remain stable. Shippers should expect the overloading trend to persist as carriers manage capacity through tactical blank sailings. This will likely lead to longer lead times and unpredictable routing changes, such as the new trend of transshipment through Busan for traditionally direct China-to-LA routes. Furthermore, if oil prices do not retreat, the market may see another round of rate hikes or increased surcharges across both ocean and air modes before the end of the month.

In the News:

Bloomberg: A New Contest for Global Influence Is Emerging in the Caucasus

https://www.bloomberg.com/news/newsletters/2026-05-04/china-to-russia-us-and-eu-chase-trade-mineral-stakes-in-caucasus

New York Times: President Threatens E.U. With Higher Car Tariffs

https://www.nytimes.com/live/2026/05/01/us/trump-news

Financial Times: How the Trump-Xi threats of trade war softened into a quieter rivalry

https://www.ft.com/content/27bb8e7b-c4f3-4c83-9952-dd140f6ba794?syn-25a6b1a6=1

Reuters: Global trade group SEMI sees robust demand for chips despite geopolitical risks

https://www.reuters.com/world/asia-pacific/southeast-asia-needs-expand-semiconductor-production-global-trade-group-semi-2026-05-05/

CNBC: Trump says he’s raising EU auto tariffs to 25%

https://www.cnbc.com/2026/05/01/trump-eu-auto-tariffs.html

More News

Ocean Freight Contract Season: Winners, Losers, and the Illusion of Stability

A look into the volatile freight contract season, exploring broken promises, rate surges, and solutions for sustainable agreements through strategic contracting and innovative market practices.

China–US Spot Market Stabilizes After November Plunge, But Gains Remain Fragile - TFX Update wk. December 8, 2025

Small December GRIs lift China–USWC and China–USEC rates slightly, but overcapacity, soft demand, and tariff uncertainty continue to cap meaningful recovery. Outlook steady through Chinese New Year with brief January strength.

Ocean Rates Up as Volumes Continue to Sink - TFX Update wk. March 23, 2026

Understand why ocean freight rates are climbing despite record low volumes. Our March 2026 update covers the $600 rate hikes, new emergency fuel surcharges, and how blank sailings are impacting China-to-US shipping costs.

Tariff Fears and Tepid Demand: Why the Transpacific "Mini-Peak" Never Arrived - TFX Update wk. January 19, 2026

Ocean freight rates fall as carriers abandon GRIs due to weak demand and tariff uncertainty. USWC rates hit $1,700–$1,800 as the expected pre-Chinese New Year volume surge fails to arrive.

Last-Minute Sailing Cancellations Push April Cargo into May - TFX Update wk. April 20, 2026

Carriers use aggressive blank sailings to maintain China-US rates at $2,700, while shippers withhold volume in anticipation of a May price drop. Explore the impact of fuel surcharges and booking rolls on your supply chain.

Trump’s Customs Enforcement Order Raises the Bar for Importers - and That May Be a Good Thing

President Trump’s customs enforcement executive order targets foreign importers of record, weak bonding, duty evasion, undervaluation, and supply-chain opacity. Here’s what small and mid-sized importers should know.

Wait-and-See Grips Importers As Rates Remain Unchanged - TFX Update: wk. July 28st, 2025

As the deadline before reciprocal tariffs take place, the Trump administration continues to make deals with nations around the world. Importers are back to taking a wait-and-see approach while rates USWC and USEC remain unchanged.

China–US Ocean Freight Market Holds Firm, but Promotional Rates Gain Traction - TFX Update wk. June 22, 2026

China–US ocean freight rates remain elevated, with CEA to USWC pricing above $6,000 while promotional carrier deals help some shipments move lower. Learn what is driving rates and what to expect heading into July.

Spot Rates Dip Below 2024 Levels as Blank Sailings Ramp Up - TFX Update wk. August 18, 2025

China-US freight rates dip to $1,520/FEU as carriers cut prices and blank sailings set up a $1,000 September GRI amid weak demand and tariff risks.

China-US Ocean Rates Hold Steady at $3K/$4K Baseline Ahead of Threatened June Spikes - TFX Update wk. May 25, 2026

Ocean freight rates hold steady, but massive June GRIs loom. Discover how carrier blank sailings and terminal capacity constraints are driving up transpacific shipping costs.