Global trade policy was dominated by a significant escalation in US tariff actions and ongoing efforts elsewhere to manage trade disputes and expand market access. The most consequential development was the Trump administration’s announcement of a sweeping 25% tariff on any country trading with Iran, immediately raising tensions with major economies and attracting threats of retaliation, especially from China. This marked a continued hardline US approach to trade policy amid geopolitical concerns, and it occurred alongside domestic legal challenges over the authority for past tariff measures.

In parallel, Europe and South America advanced the long-gestating EU-Mercosur free trade agreement, signaling a major tariff-reducing integration after decades of negotiations and reflecting alternative trade cooperation amid rising protectionism. European efforts to strengthen commercial ties with India and resolve Beijing-EU industrial disputes over electric vehicles further underscored a multipolar trade landscape navigating both tariff pressures and strategic partnerships. Overall, the week’s events highlighted the persistence of tariff-driven disruption in global trade alongside efforts to pursue broader trade liberalization and dispute management.

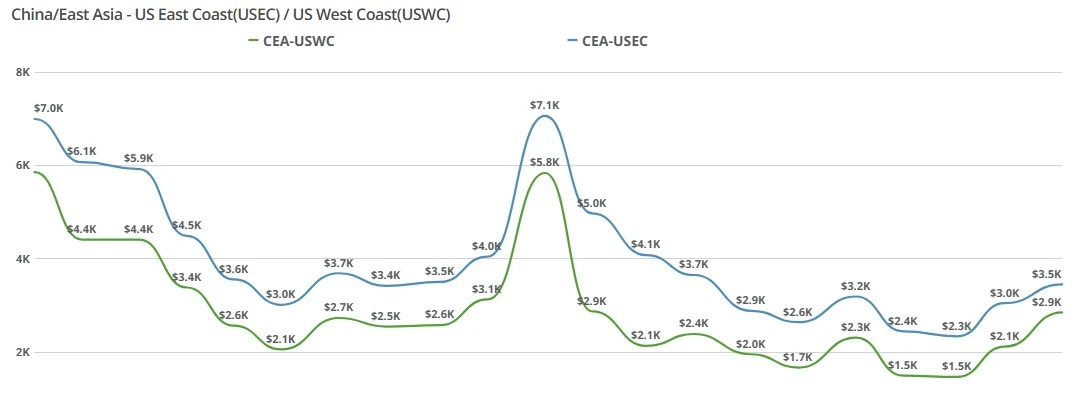

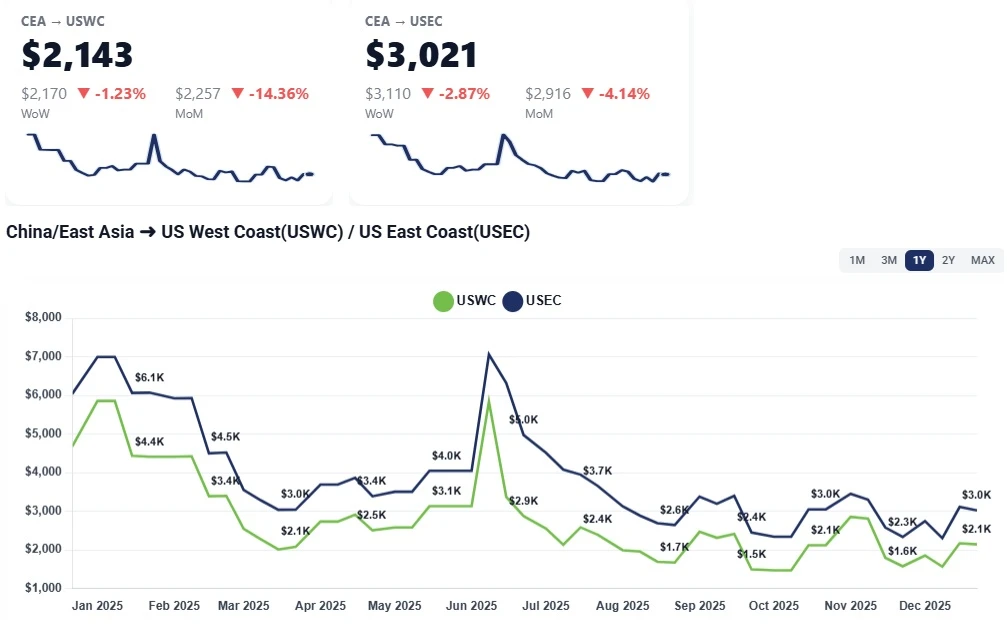

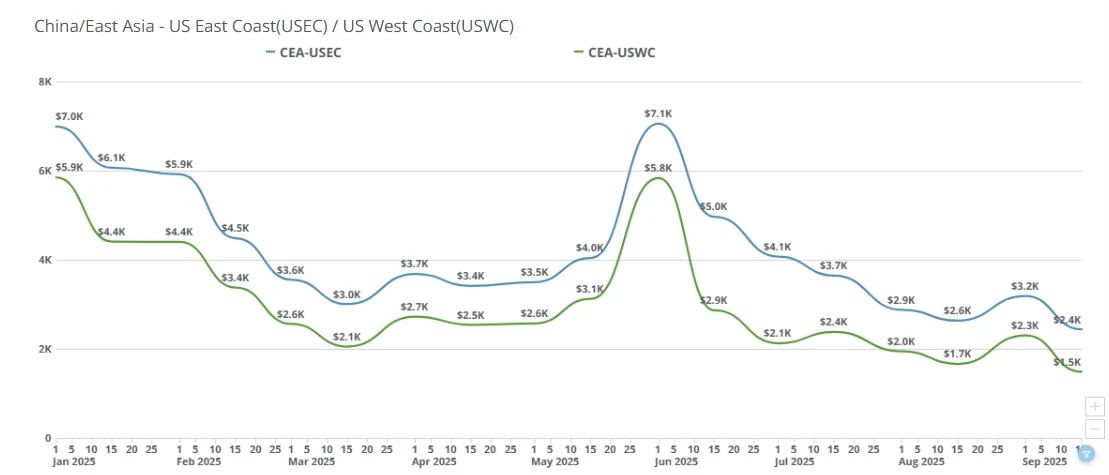

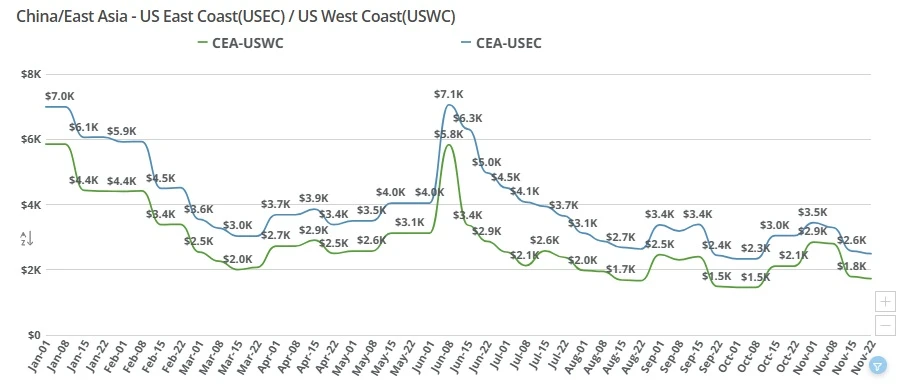

CEA to USWC (China to US West Coast): China–US West Coast spot rates fell sharply week-over-week, sliding back into the $1,850–$1,950 per FEU range. Early-January GRIs have effectively washed out as demand failed to materialize, leaving carriers with little pricing power. While most carriers are signaling another aggressive GRI attempt for the second half of January, targeting rates north of $3,000/FEU, early market behavior suggests limited staying power at those levels.

CEA to USEC (China to US East Coast): Rates to the East Coast followed a similar trajectory, easing week-over-week as volumes remained muted. Although carriers are aiming for $4,000+ per FEU later this month, competitive pressure and weak fundamentals are already undermining these efforts. As with the West Coast, any mid-month increases are expected to face rapid erosion.

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

Lack of volume support: Post-holiday demand has failed to rebound, with January volumes tracking similarly to December lows. As noted in the discussion, “there’s no shipment, there’s no volumes,” making sustained rate increases difficult.

GRIs without fundamentals: Carriers pushed significant GRIs at the start of January, but most of those increases have already disappeared. The market is now seeing a familiar pattern: GRIs announced, partial stickiness, followed by rapid rollback.

Carrier divergence on pricing strategy: While most carriers are holding firm on announced mid-month increases, at least one smaller carrier is offering sub-$2,000 rates deep into the second half of January, signaling low confidence in demand and pressuring the broader market downward.

Artificial capacity management: Blank sailings and vessels taken out of rotation are tightening space temporarily, but this is a supply-side maneuver—not demand-driven congestion. Once capacity normalizes, rates are likely to soften again.

Pre–Chinese New Year timing mismatch: Unlike stronger years, January demand is not strong enough to support elevated pre–Lunar New Year pricing, forcing carriers into repeated GRI attempts rather than a single, sustained increase.

Expect continued volatility through the second half of January. While carriers will attempt to push rates higher ahead of Chinese New Year using GRIs and blank sailings, underlying demand remains too weak to sustain those levels. Market indicators point toward rates drifting back toward the low-$2,000 range by late January, particularly on the West Coast, with East Coast lanes following closely behind. Into February, pricing is likely to stabilize briefly around Lunar New Year before resuming downward pressure as capacity returns and volumes reset.

BBC: How tariff disruption will continue reshaping the global economy in 2026

https://www.bbc.com/news/articles/czejp3gep63o

Bloomberg: China to Cut Export Tax Rebates to Ease Global Trade Tensions

https://www.bloomberg.com/news/articles/2026-01-09/china-to-cut-export-tax-rebates-to-ease-global-trade-tensions

Global Trade Magazine: US Container Imports Expected to Stay Below 2025 Levels Through Spring

https://www.globaltrademag.com/u-s-container-imports-expected-to-stay-below-2025-levels-through-spring/

The Wall Street Journal: TSMC Plans U.S. Expansion in Proposed Taiwan Tariff-Relief Deal

https://www.wsj.com/tech/tsmc-plans-u-s-expansion-in-proposed-taiwan-tariff-relief-deal-280d8a08

Reuters: Trump's Iran tariff threat risks reopening China rift

https://www.reuters.com/world/china/trumps-iran-tariff-threat-risks-reopening-china-rift-2026-01-13/

Transpacific ocean freight rates fell sharply in January after carriers failed to sustain GRIs amid weak China-US shipping demand.

Transpacific ocean freight rates from China to the US West and East Coasts remained elevated week over week as carriers held firm through the holiday slowdown, positioning pricing ahead of Chinese New Year and upcoming contract season negotiations.

China–US ocean freight rates fall as carriers discount to fill space. CEA-USWC down $400-$500; CEA-USEC near $2,800. See what’s driving the drop and what’s next.

China-to-US ocean freight rates fell by about $1,000 this week as carriers lowered prices to stimulate demand. Read the latest Freight Right market update on CEA to USWC and USEC rates, tariff uncertainty, and the outlook for the remainder of the 2026 pea

China–US ocean freight rates remain elevated, with CEA to USWC pricing above $6,000 while promotional carrier deals help some shipments move lower. Learn what is driving rates and what to expect heading into July.

Ocean freight rates hold steady, but massive June GRIs loom. Discover how carrier blank sailings and terminal capacity constraints are driving up transpacific shipping costs.

China–US ocean freight rates from CEA to the US West Coast and East Coast softened slightly week over week as demand remained low, carriers tested modest reductions, and the market appeared to reach a near-term rate ceiling.

China–US ocean freight rates to the West and East Coasts held steady this week amid a holiday slowdown. Learn what’s driving the flat market and why January GRIs could push prices higher.

China–US ocean spot rates eased WoW as early-September GRIs faded. USWC nears trough, USEC softens, and fierce forwarder pricing persists ahead of Golden Week.

Transpacific ocean freight rates dropped sharply this week as weak import demand and the Thanksgiving holiday slowdown pushed China–US West and East Coast spot prices to new lows. Get the latest market drivers and outlook.