The first full week of March 2026 saw the global economy begin to internalize the costs of the new US Section 122 surcharge, sparking a defensive rotation in financial markets as technology and retail giants warned of significant profit losses. While the US judiciary moved efficiently to dismantle the previous IEEPA tariff regime, creating a potential $175 billion windfall for importers, the executive branch simultaneously hardened its stance at the WTO by vetoing major reform plans. In response, the European Union accelerated its transition toward strategic sovereignty with the introduction of the Industrial Accelerator Act, effectively signaling that the era of open markets is being replaced by a system of regional preferences and managed trade.

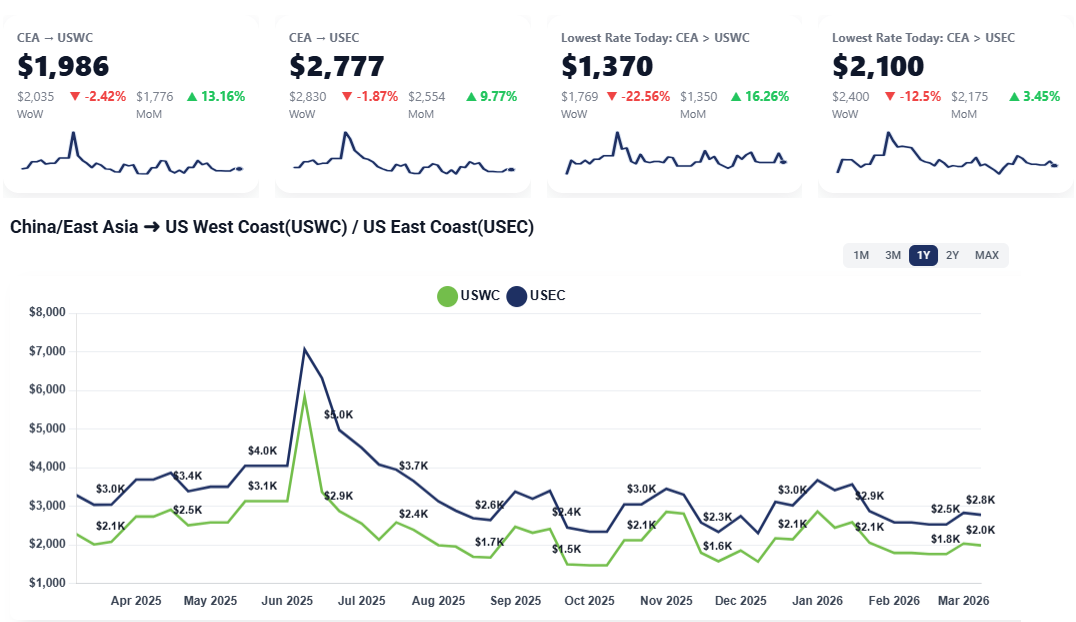

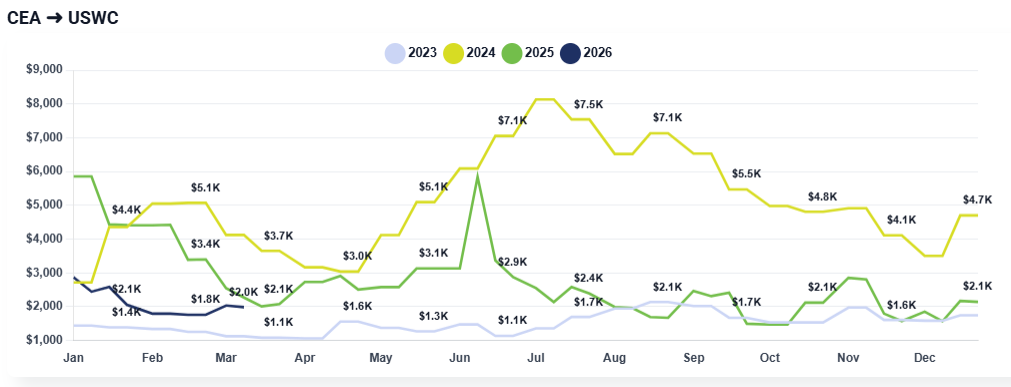

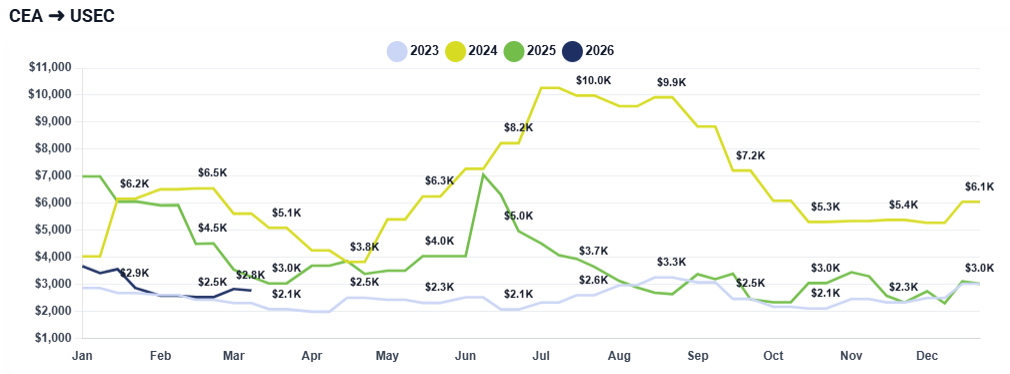

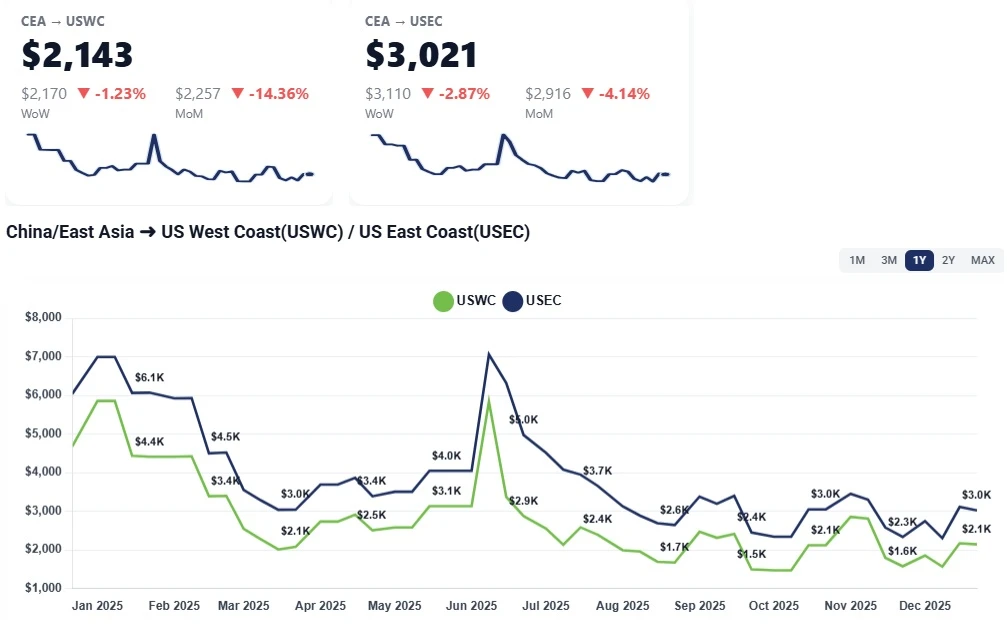

The Transpacific ocean freight market is navigating a period of post-holiday stabilization, while the anticipated free fall in rates following the Lunar New Year has not materialized, pricing remains at or near carrier breakeven levels.

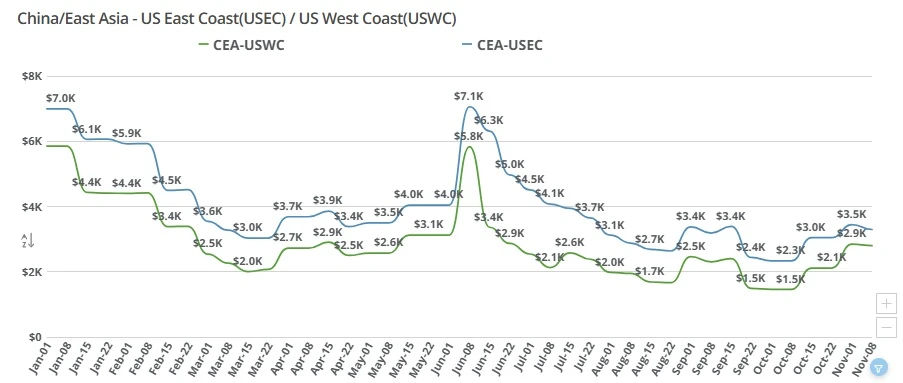

CEA to USWC: Rates have held relatively steady week-over-week, currently sitting at approximately $1,500 per container. Carriers are resisting further drops, as current levels offer little to no profit margin.

CEA to USEC: Rates to the East Coast continue to hover around the $2,400 to $2,500 mark. The spread between West and East Coast pricing remains consistent with the previous two weeks of market activity.

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

Absence of a Rate War: Contrary to historical trends where carriers slash prices post-holiday to capture first volumes, the market has seen a surprising lack of aggressive price-cutting.

Carrier Resistance at Breakeven: Carriers are largely holding the line at $1,500 for the West Coast because dropping further would move operations from "at-cost" into active losses.

Slow Factory Ramp-Up: While factories have reopened, they are not yet producing at full capacity. Most currently moving cargo consists of "breadcrumb" volumes—inventory that was left over from before the holiday shutdown.

Demand Stagnation: The market has yet to see a fresh surge of orders from the U.S. side, keeping the overall supply-demand balance relatively flat despite the resumption of operations.

The industry is currently in a wait and see period that will likely define the upcoming contract season.

The next two to three weeks are critical as the first "true" post-holiday orders begin to hit the water. Current indicators suggest that rates will remain flat through late March. However, carriers are expected to keep a close eye on these volumes to inform their strategy for the April and May contract negotiations. If demand remains tepid, shippers should expect carriers to introduce more aggressive capacity management, such as blank sailings, in an effort to artificially tighten the market and bolster their bargaining power for long-term agreements.

Bloomberg: In Charts: How The Iran Conflict is Disrupting Global Trade

https://www.bloomberg.com/news/articles/2026-03-07/in-charts-how-the-iran-conflict-is-disrupting-global-trade

CNBC: Maersk, a bellwether for global trade, suspends two key shipping services due to Iran war

https://www.cnbc.com/2026/03/06/iran-war-shipping-maersk-middle-east-strait-of-hormuz-gulf.html

Financial Times: Beyond the stricken Gulf, global trade is relatively calm

https://www.ft.com/content/86699441-39fc-44d6-8092-964562ad2c39

Reuters: Tariff ruling will not save tariff evaders

https://www.reuters.com/legal/legalindustry/tariff-ruling-will-not-save-tariff-evaders--pracin-2026-03-09/

The Guardian: US preparing system to process refunds on billions in illegal Trump tariffs https://www.theguardian.com/us-news/2026/mar/06/us-judge-lawyers-175bn-trump-tariffs-refunds

Ocean rates hold at $1,450-$1,500 for USWC as Chinese factories reopen. Explore why the post-holiday rate crash didn't happen and what to expect for the March recovery.

Transpacific ocean freight rates from China to the US West and East Coasts remained elevated week over week as carriers held firm through the holiday slowdown, positioning pricing ahead of Chinese New Year and upcoming contract season negotiations.

Ocean freight rates fall as carriers abandon GRIs due to weak demand and tariff uncertainty. USWC rates hit $1,700–$1,800 as the expected pre-Chinese New Year volume surge fails to arrive.

Ocean freight rates from China to USWC have hit a breakeven low of $1,450 per container. As the Chinese New Year halts Asian manufacturing, explore why rates are falling, the impact of late-week bookings, and the outlook for March contract negotiation.

China to US rates surge toward $4,500 as carriers implement mid-month hikes. Learn how post-holiday demand, IEEPA refunds, and shifting air freight trends are redefining Trans-Pacific logistics strategies.

Ocean rates hold steady at $1,400-$1,600 for USWC as China’s pre-holiday shipping window closes. Explore the impact of high trucking costs and the upcoming total market shutdown.

A look into the volatile freight contract season, exploring broken promises, rate surges, and solutions for sustainable agreements through strategic contracting and innovative market practices.

China–US ocean freight rates to the West and East Coasts held steady this week amid a holiday slowdown. Learn what’s driving the flat market and why January GRIs could push prices higher.

Understand why ocean freight rates are climbing despite record low volumes. Our March 2026 update covers the $600 rate hikes, new emergency fuel surcharges, and how blank sailings are impacting China-to-US shipping costs.

Transpacific ocean freight rates continue to decline as post-peak demand cools. China–US West Coast rates near $1,700, East Coast around $2,600 per FEU.