- Home

- >

- News

- >

- Freight Market Correction Deepens on CEA-US Routes After November GRI - TFX Update wk. November 3, 2025

Freight Market Correction Deepens on CEA-US Routes After November GRI - TFX Update wk. November 3, 2025

The Lead:

Last week, from October 28 to November 3, 2025, global trade policy remained highly dynamic. A major development was the signing of an upgraded free-trade agreement between China and ASEAN, seen as a strategic response to the U.S.’s aggressive tariff posture. At the same time, trade-policy watchers recorded a steady stream of new regulatory and industrial-policy measures across multiple regions, underscoring that tariff pressure is driving realignment in supply-chains and trade flows. Businesses globally are now operating in an environment of heightened uncertainty, adapting to tariff risk and recalibrating sourcing and distribution strategies accordingly.

This Week’s Ocean, Air & Freight Markets

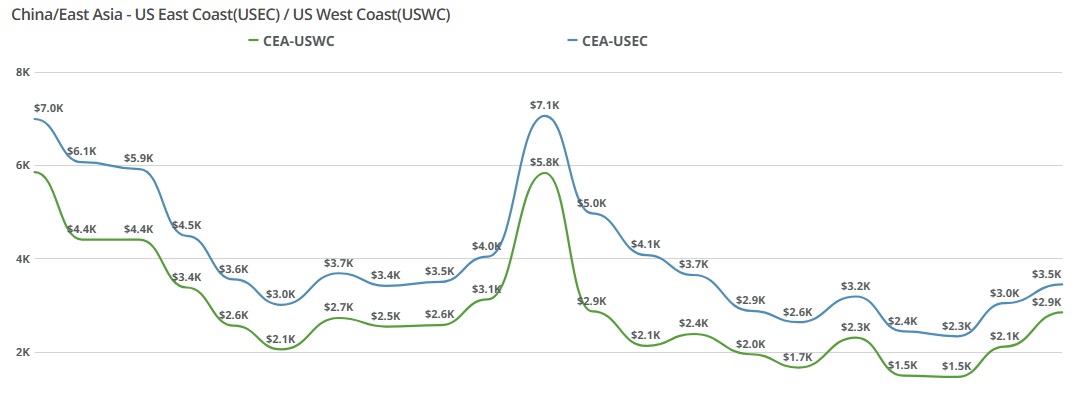

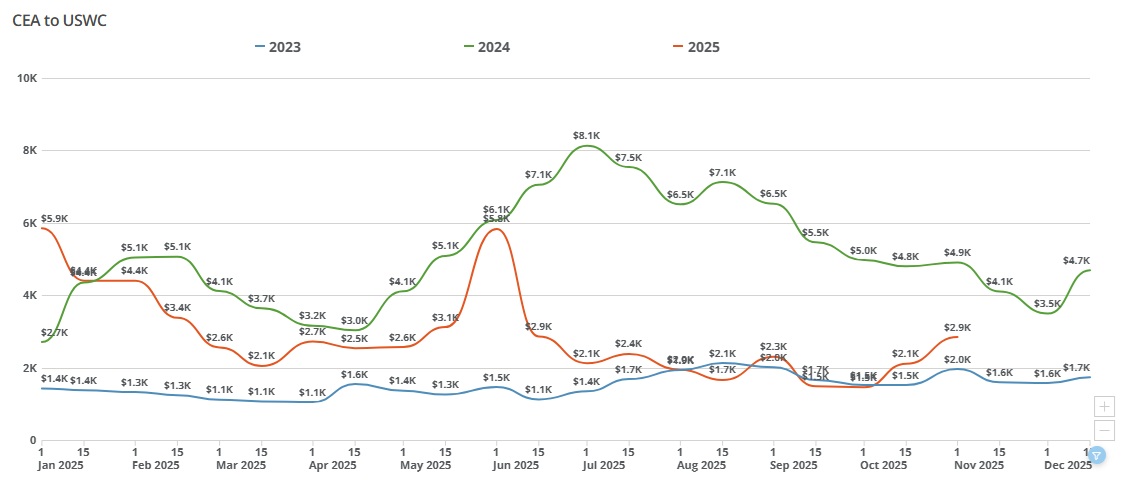

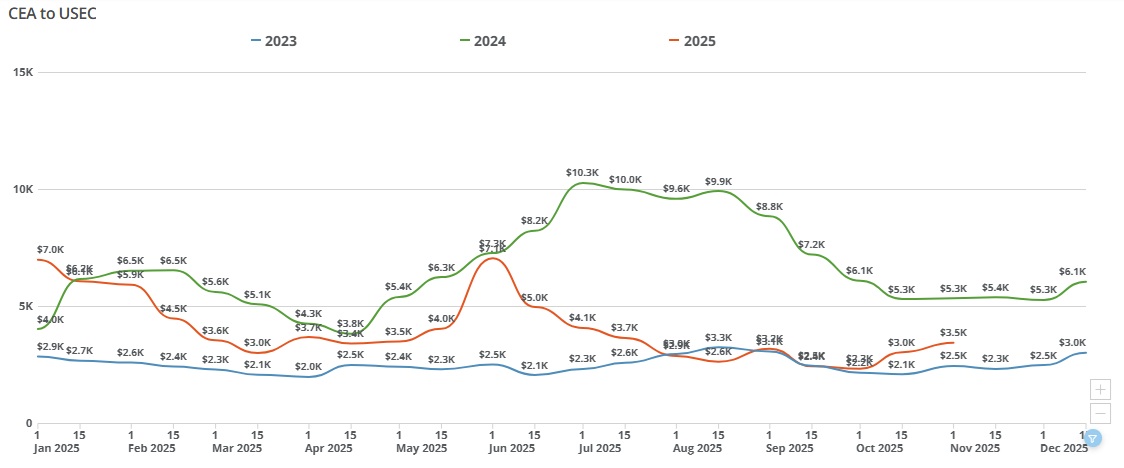

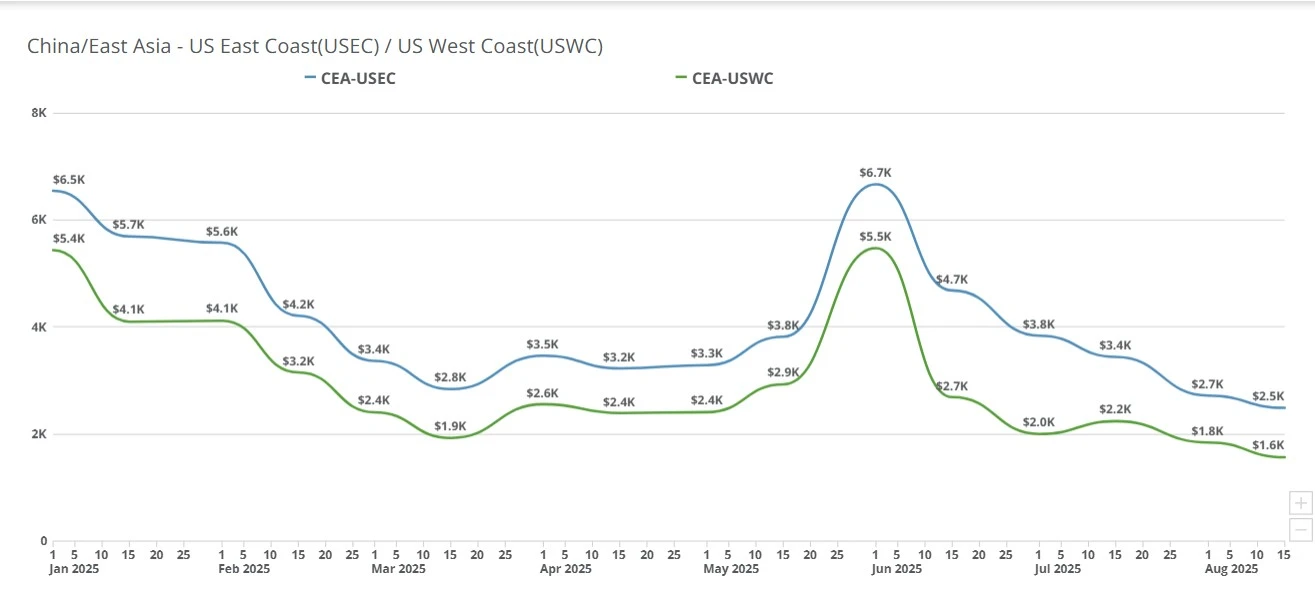

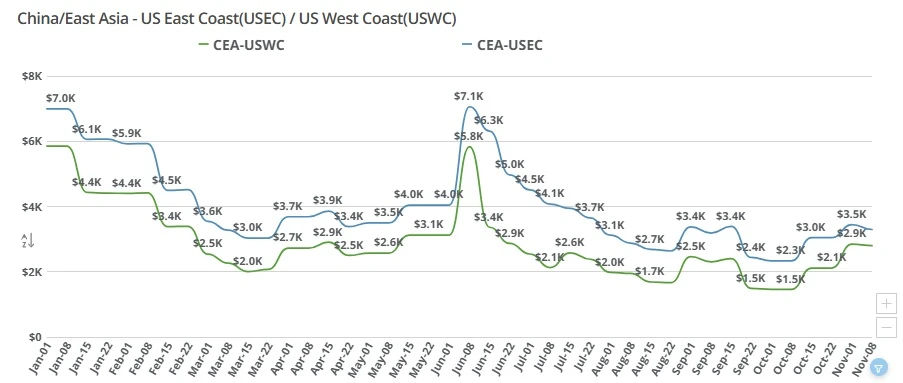

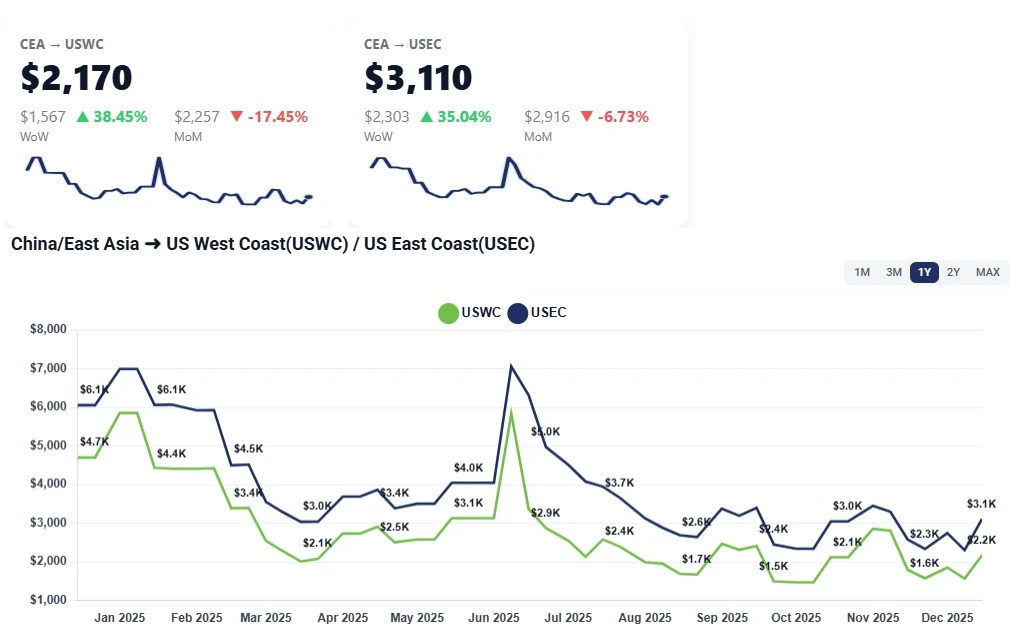

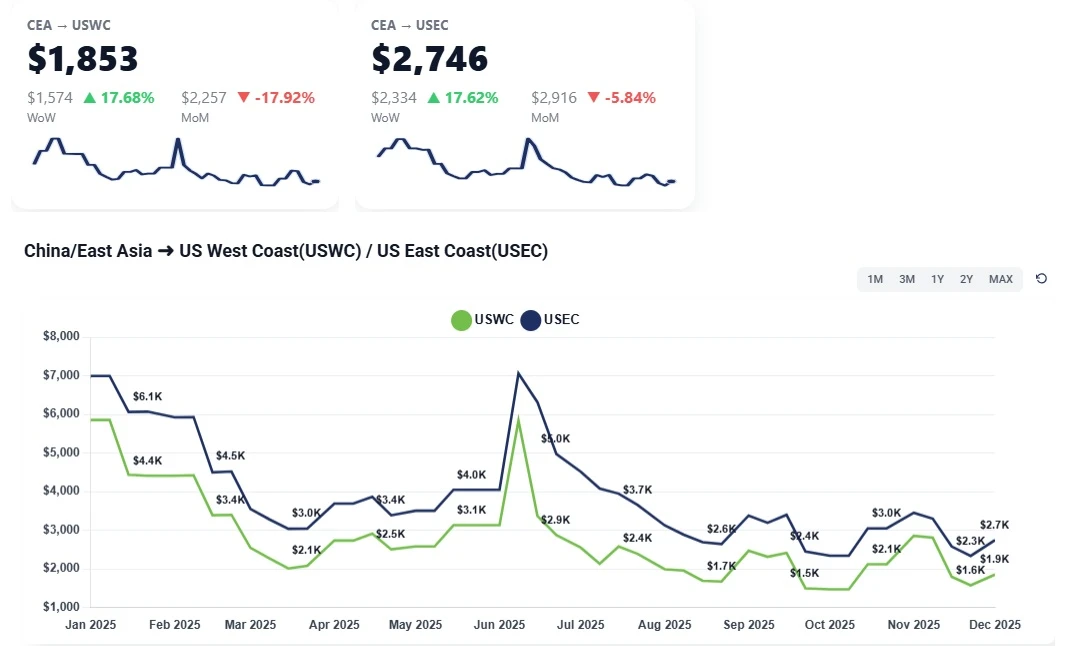

China-US Ocean Freight Market:

CEA → USWC (China → U.S. West Coast): After the Nov 1 GRI lifted posted FAK levels toward the ~$2,900–$3,100/FEU range, actual market-clearing “specials” are widely available around $1,900–$2,100/FEU, with agents indicating a week-over-week slide of roughly $400–$500. These discounts are tied to specific near-term sailings (e.g., vessels around Nov 7 and Nov 12) and reflect carriers’ need to backfill half-empty ships.

CEA → USEC (China → U.S. East Coast): Similar two-tier dynamics. Posted tariffs remain elevated, but “specials” are circulating near ~$2,800/FEU, implying a modest week-over-week softening from early-month peaks. Discounts are again limited to named sailings.

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

This Week Explained:

Demand air pocket post-peak: With peak season done, bookings are thin; carriers are sailing with excess space and need loads now.

Policy uncertainty = importer pause: Headlines about possible tariff changes lack concrete CBP/White House implementation guidance, prompting shippers to wait, further weakening near-term demand.

Two-tier pricing to save face: Carriers keep the higher filed FAKs on paper while quietly pushing broad “specials” to fill a couple of imminent vessels, avoiding the optics of formally rolling back the GRI.

Widespread access to discounts: Forwarders across the market are receiving and selling the discounted rates; this isn’t a niche or restricted offer.

Short booking window: In a two-week pricing cycle, there are effectively only two relevant sailings; carriers concentrate discounts there to quickly firm load factors.

Looking Ahead:

For the next 1–2 weeks, expect USWC to hover $1,800–$2,000/FEU and USEC around $2,700–$2,900/FEU on specials, with posted FAKs remaining higher but not representative of transactable levels.

The current gap between filed and discounted rates is likely to narrow or close, as carriers align headline rates with market reality once immediate sailings are covered. Timing could be late November or the first half of December.

If concrete US–China policy changes materialize or typical pre-CNY pull-forward emerges, carriers may test fresh GRIs; absent that, soft fundamentals should keep rates range-bound near today’s specials. Shippers should target named-sailing space to capture discounts and avoid paying posted FAKs.

In the News:

Reuters: South Korea's Lee says global trade order at critical inflection point: https://www.reuters.com/world/china/south-koreas-lee-says-global-trade-order-critical-inflection-point-2025-10-31/

The Wall Street Journal: Meet Rapidly Evolving Global Trade With Resilience Strategies https://deloitte.wsj.com/riskandcompliance/meet-rapidly-evolving-global-trade-with-resilience-strategies-047bbbee

Global Trade Magazine: President Trump to Skip Supreme Court Tariffs Hearing https://www.globaltrademag.com/president-trump-to-skip-supreme-court-tariffs-hearing/

Global Trade Magazine: US and China Announce Trade Pact Suspending Tariffs and Export Controls https://www.globaltrademag.com/u-s-and-china-announce-trade-pact-suspending-tariffs-and-export-controls/

More News

Carriers Prepare August GRIs Following Sharp West Coast Rate Decline - TFX Update wk. July 27, 2026

China to US ocean freight rates declined again this week, led by sharp drops on West Coast routes while East Coast pricing remained relatively resilient. Learn what's driving the market correction, August rate increases, and what to expect as peak shippin

Carriers Cut Rates at Month-End, Importers Scramble to Book Before GRI - TFX Update: wk. August 25, 2025

China–US freight rates drop again: $1,400 to West Coast, $2,300 to East Coast, as carriers cut prices before September hikes.

Space Tightens on China-US Routes Despite Weak Underlying Volume - TFX Update wk. April 13, 2026

Explore how aggressive blank sailings and new blended rate strategies are stabilizing CEA to USWC/USEC shipping costs despite weak demand. Stay informed on current ocean freight market updates and rate changes.

China-US Ocean Rates Ease Again as Post-Peak Lull Deepens - TFX Update wk. November 10, 2025

Transpacific ocean freight rates continue to decline as post-peak demand cools. China–US West Coast rates near $1,700, East Coast around $2,600 per FEU.

Carriers Push Back with GRIs, but Market Fundamentals Push Harder - TFX Update wk. January 12, 2026

China–US ocean freight rates fell week-over-week as weak January demand erased early GRIs. See what’s driving transpacific pricing and where rates may head next.

Tariff Fears and Tepid Demand: Why the Transpacific "Mini-Peak" Never Arrived - TFX Update wk. January 19, 2026

Ocean freight rates fall as carriers abandon GRIs due to weak demand and tariff uncertainty. USWC rates hit $1,700–$1,800 as the expected pre-Chinese New Year volume surge fails to arrive.

Transpacific Rates Pop Again: Carriers Push Mid-December Increases Into January - TFX Update wk. December 15, 2025

China–US ocean freight rates rose WoW: USWC near $2.1K/FEU and USEC near $2.9–$3.0K as carriers end fixed extensions and hold firm into January.

China-U.S. Ocean Freight Steadies as Carriers Prepare $1,000 November GRI - TFX Update wk. October 27, 2025

U.S-China trade deal specifics; transpacific freight rates hold steady as carriers plan a $1,000 GRI for Nov. 1, easing fears after tariff threats and muted seasonal demand.

China–US West and East Coast Rates Hold Flat After Short-Lived December Rate Spike - TFX Update wk. December 1, 2025

Weekly ocean freight update on China–US West and East Coast lanes as an early December GRI fades, leaving spot rates near November levels amid weak demand.

Carriers Hold the Line at $1,500 Floor - TFX Update wk. March 9, 2026

Ocean rates hold steady at $1,500 for USWC as Chinese factories reopen. Explore why the post-holiday rate war never arrived and what this means for April contract negotiations.