The first week of June 2026 saw a transition from chaotic, emergency trade restrictions to deeply structured, long-term industrial protectionism. By unveiling a two-tiered, 60-nation Section 301 tariff framework based on forced labor criteria, the US successfully engineered a more durable, court-proof legal vehicle to replace its temporary balance-of-payments surcharges before they expire in July. This aggressive US move toward a highly regulated, centralized trade architecture forced major partners into structural pivots: the European Union finalized a critical concession pact with Washington to secure its baseline 10% preference while simultaneously enacting a fierce new domestic steel quota regime to lock out Chinese market dumping. Ultimately, the week proved that while a multipolar landscape continues to operate elsewhere through localized compromises like the new US-China Board of Trade, global supply chains are facing a permanently higher cost baseline dictated by strict national labor, environment, and metal-origin compliance walls.

The container shipping market is experiencing substantial week-over-week rate increases, catching many importers by surprise as prices climb significantly. Current ocean freight rates are rapidly escalating past previous baselines .

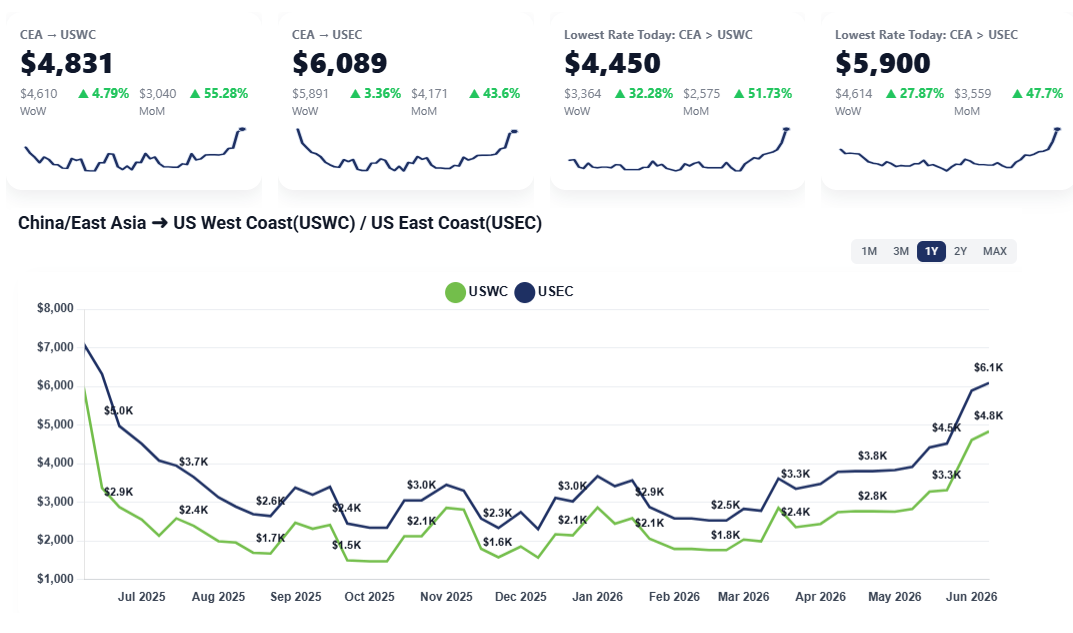

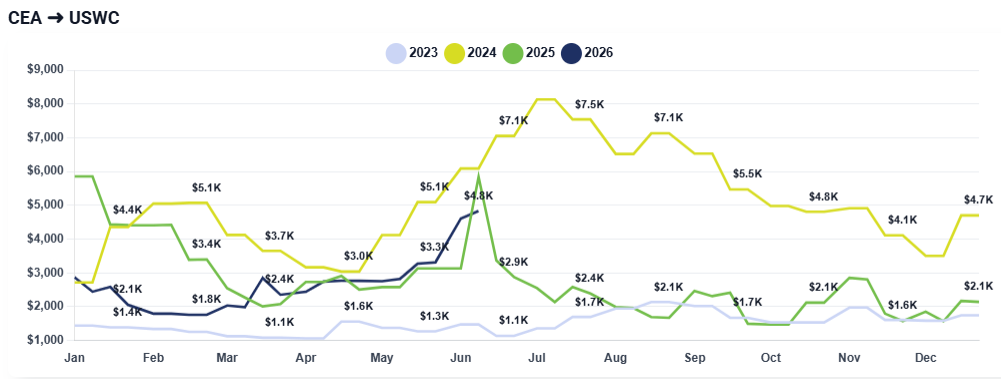

CEA to USWC: Rates have surged from the high $4,000+, nearly $5,000, and are explicitly projected to climb over $6,000+ per container.

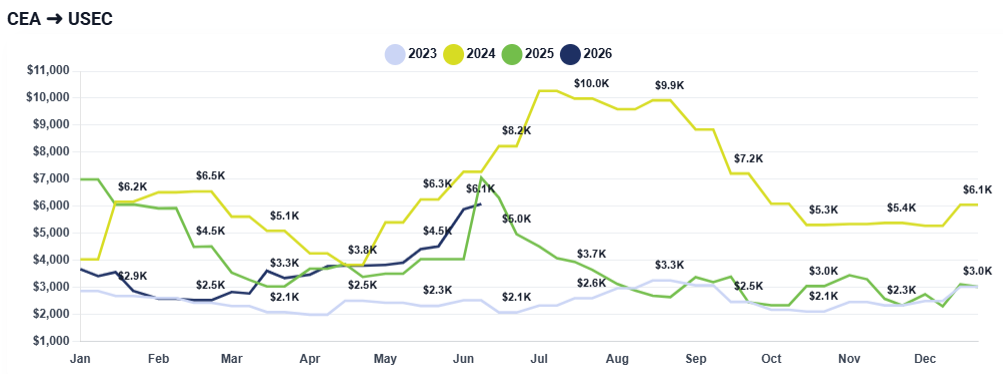

CEA to USEC: Rates are following a similar upward trajectory and are expected to surpass $7,000+ per container.

Freight Right’s Lowest Rate indicators are finding that importers can find spot rates as low as $4,450 from China to US West Coast and $5,900 from China to US East Coast. Talk to your freight forwarder about options available to you.

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

The Traffic Jam Backlog in China: Persistent blank sailings have triggered severe cargo backlogs at Chinese export hubs. When a carrier cancels a voyage, hundreds of containers are rolled to the following week, compounding volumes, generating a traffic jam effect, and triggering multi-day communication delays just to confirm bookings.

Pre-July Tariff Anxiety and Front-Loading: Importers are grappling with immense confusion and marketing anxiety regarding impending July tariff changes. To avoid recalculation headaches and potential margin erosion from unexpected 20% to 30% adjustments, businesses are aggressively front-loading their fall and holiday season inventories ahead of schedule.

Overlapping Demand Cycles: The unseasonal surge of front-loaded holiday goods is directly colliding with the traditional, non-negotiable peak importing window for summer and outdoor seasonal products, overwhelming available vessel space.

The current market strain represents an early, highly compressed peak season rather than the traditional timeline typically seen later in the year. This elevated rate environment is expected to persist through the remainder of June and throughout July, as ocean carriers are highly unlikely to voluntarily relinquish their pricing leverage.

A traditional, prolonged peak season spanning August through October appears unlikely under current macroeconomic conditions. Instead, relief will likely hinge on two primary triggers later this summer: Front-loaders completely depleting their advanced supply chain volumes by late July, causing export demand to drop; and carriers systematically restoring blanked vessels back into active service rotations.

Once vessel space opens up, carriers will be forced to downwardly adjust their pricing levels to attract volume, potentially pointing toward market normalization by August or September.

Bloomberg: Trump’s Tariff Wall Takes a Curious Woke Turn

https://www.bloomberg.com/news/newsletters/2026-06-08/trump-and-tariffs

NYTimes: Trump Administration Turns to a New Rationale to Justify Old Tariffs

https://www.nytimes.com/2026/06/03/business/economy/trump-tariffs-forced-labor.html

CNBC: Trump’s trade war has a new target: forced labor. The case behind it is far from simple

https://www.cnbc.com/2026/06/09/trump-tariffs-trade-china-forced-labor.html

Reuters: Signs global trade in goods is starting to slow, WTO says

https://www.reuters.com/business/signs-global-trade-goods-starting-slow-wto-says-2026-06-05/

Financial Times: Donald Trump’s replacement tariff wall continues to rise

https://www.ft.com/content/ed7c8cb6-821e-47f3-80c0-463f4bca6e3e?syn-25a6b1a6=1

Late-June front-loading has triggered a severe transpacific space crunch. Discover how carrier rate hikes are driving ocean freight costs to new heights as shippers scramble for limited vessel capacity.

Transpacific ocean freight rates soared past $6,000 to the USWC and hit the mid-$7,000s to the USEC. Discover how front-loading and severe space constraints are driving this week's market update.

Ocean freight rates hold steady, but massive June GRIs loom. Discover how carrier blank sailings and terminal capacity constraints are driving up transpacific shipping costs.

China–US ocean freight rates remain elevated, with CEA to USWC pricing above $6,000 while promotional carrier deals help some shipments move lower. Learn what is driving rates and what to expect heading into July.

Transpacific ocean freight rates from China to the US West and East Coasts remained elevated week over week as carriers held firm through the holiday slowdown, positioning pricing ahead of Chinese New Year and upcoming contract season negotiations.

A look into the volatile freight contract season, exploring broken promises, rate surges, and solutions for sustainable agreements through strategic contracting and innovative market practices.

Ocean freight rates double for USWC and USEC as carrier capacity cuts trigger severe space shortages and rolled cargo. Read the latest weekly freight market update on rising spot rates, premium expedited shipping surges, and the June GRI outlook.

China-US freight rates dip to $1,520/FEU as carriers cut prices and blank sailings set up a $1,000 September GRI amid weak demand and tariff risks.

China-US rates remain stable at $2,700-$3,800, but blank sailings and vessel overloading are causing record shipment rollovers and strategic rerouting through Busan.

Carriers use aggressive blank sailings to maintain China-US rates at $2,700, while shippers withhold volume in anticipation of a May price drop. Explore the impact of fuel surcharges and booking rolls on your supply chain.