Last week showed global trade policy moving in two directions at once: governments continued tightening enforcement and tariff tools while also opening new negotiation channels to manage the fallout. In the United States, CBP’s indefinite suspension of the de minimis exemption for low-value imports marked a major enforcement shift, while USTR’s Section 301 investigation into Germany’s pharmaceutical pricing practices signaled that sector-specific tariff pressure remains a live policy tool. In Europe, the UK moved forward with tighter steel safeguards, including lower tariff-free quotas and a higher over-quota duty, while the EU opened a new three-month consultation process with China to address trade imbalances, export controls, market access, and import surges. India’s comments on a potential U.S. trade deal further underscored that tariff positioning remains a core negotiating objective for major manufacturing economies. Overall, the week reflected a global trade environment defined by tariff volatility, industrial protection, supply chain security, and selective bilateral dealmaking rather than broad liberalization.

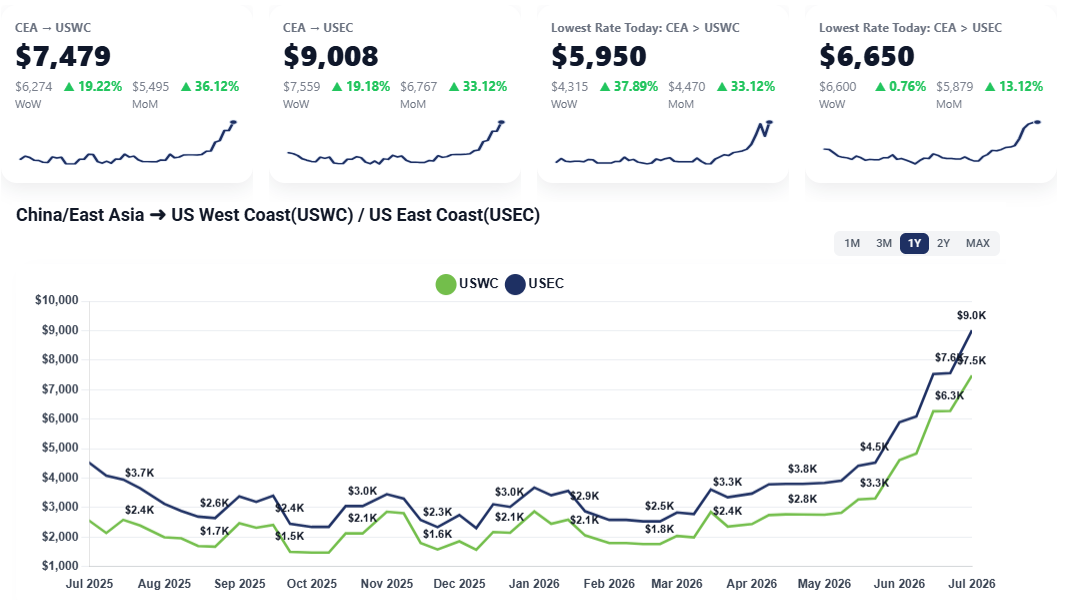

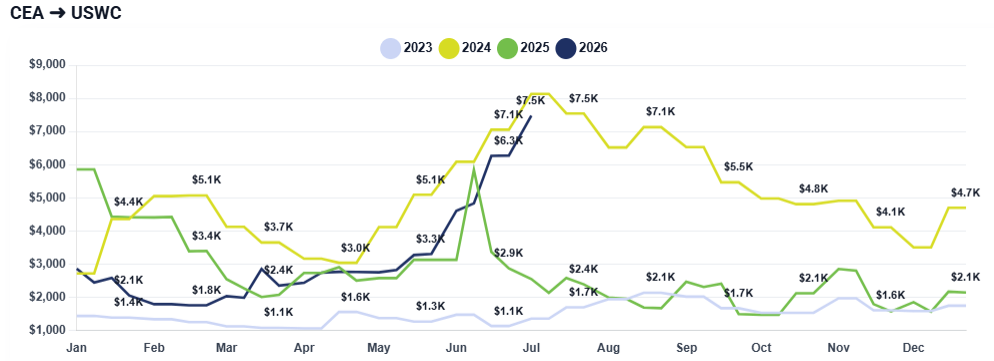

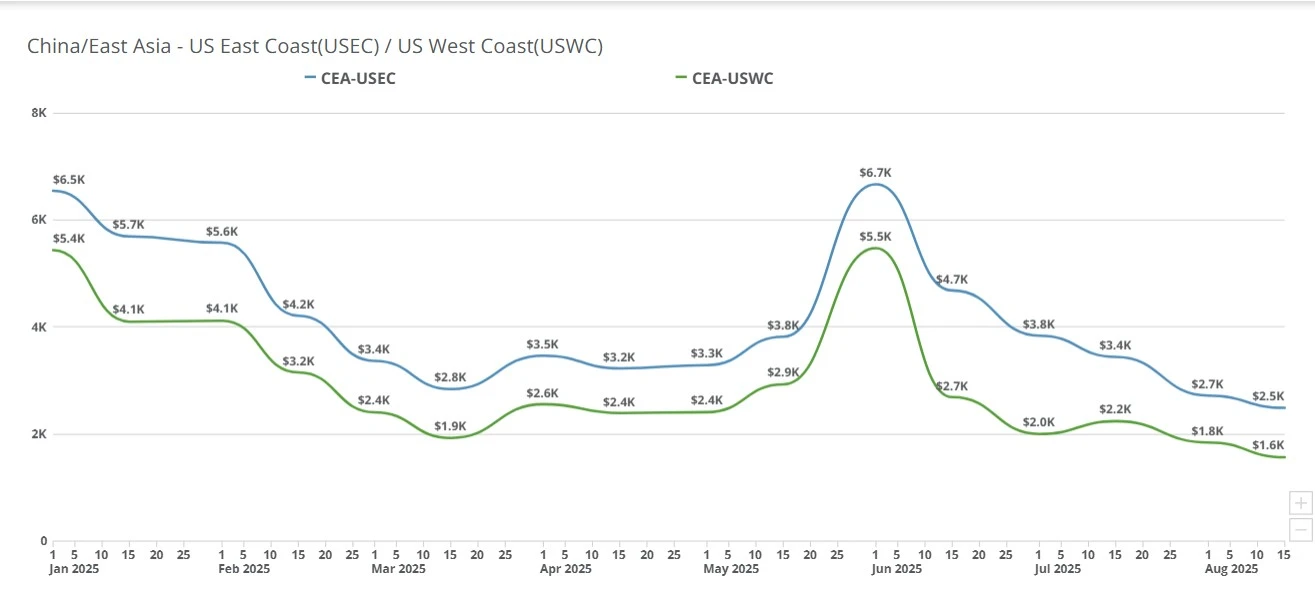

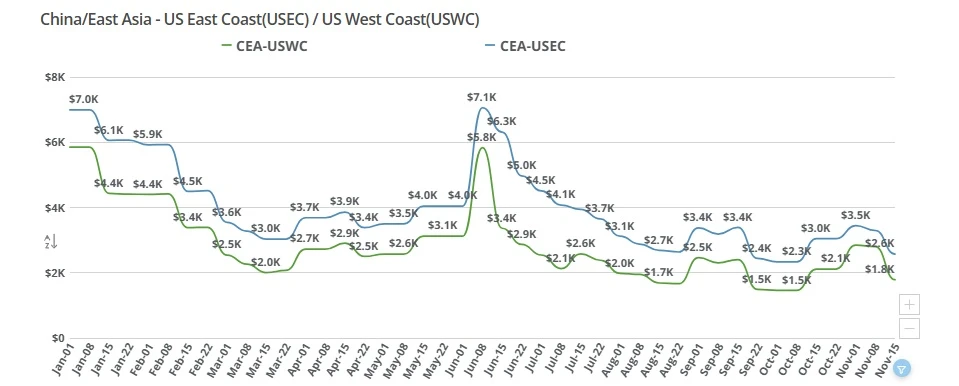

CEA to USWC: spot rates are averaging in the mid-$7,000, with standard standalone containers tracking between $7,500 and $7,900.That represents a dramatic increase from levels seen just a few months ago, when West Coast rates were closer to the $1,600–$1,700 range.

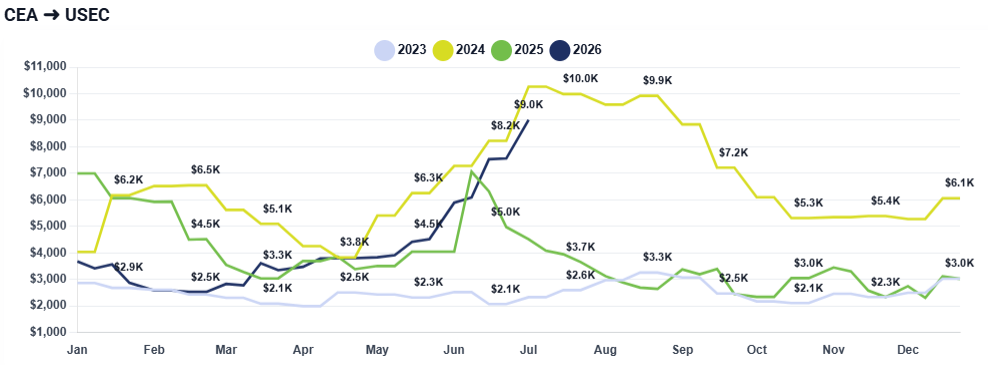

CEA to USEC: rates lane has climbed to nearly $9,000, with inland and Midwest movements pushing past the $10,000 threshold. Space remains tight despite some reported capacity increases of roughly 6%–7%, and those additions do not appear large enough to meaningfully relieve the market.

Freight Right’s Lowest Rate indicators are finding that importers can find spot rates as low as $5,950 from China to US West Coast and $6,650 from China to US East Coast. Talk to your freight forwarder about options available to you.

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

Imminent July General Rate Increases (GRIs): Carriers are testing the market’s upper limits by introducing an additional $1,500 GRI for the first half of July. This triggered a massive, last-minute rush at the end of June as shippers scrambled to push containers out of China to avoid the premium.

Aggressive Inventory Front-Loading: Importers have fundamentally compressed the typical multi-month peak season. Fearing prolonged volatility, businesses pulled forward orders they did not immediately need, clogging current vessel capacity with goods destined for sales cycles months down the line.

The market is rapidly approaching a critical breaking point. Because current rate structures are no longer a true reflection of baseline market conditions, a noticeable drop in volume is projected for July. Many general importers possess roughly three to four weeks of safety stock and are expected to pause bookings for the first half of the month to see if rates soften. The primary exception will be manufacturing supply chains, which are forced to absorb these stiff premiums to avoid halting production lines.

While a two-week shipping strike or buyer strike from importers could force an adjustment , a significant price correction (such as a drop back down to the $5,500 range) is highly unlikely in the near term. Because core geopolitical disruptions remain active and carriers are intent on squeezing every penny out of the current capacity crunch, spot rates are expected to grind out at these elevated levels through the end of July.

NY Post: US tariff refunds rush into company accounts ahead of deadline this week: ‘Never thought this day would come’

https://nypost.com/2026/06/29/business/us-tariff-refunds-rush-into-company-accounts-ahead-of-deadline-this-week-never-thought-this-day-would-come/

The Business Journals: Mitigating disruption: How will evolving global trade dynamics impact my business?

https://www.bizjournals.com/boston/news/2026/06/29/mitigating-disruption-global-trade-impact-business.html

Bloomberg: Global Trade Braces for Another Period of Policy Uncertainty

https://www.bloomberg.com/news/newsletters/2026-06-29/global-trade-uncertainty

Reuters: Why Trump's tariffs had plenty of bark, but limited bite

https://www.reuters.com/commentary/reuters-open-interest/why-trumps-tariffs-had-plenty-bark-limited-bite-2026-06-30/

The Guardian: EU halves duty-free steel quota but UK and other partners given better rate

https://www.theguardian.com/business/2026/jun/30/eu-duty-free-steel-quota-uk-rate-brexit

Ocean freight rates skyrocket past $6,000 to USWC and $7,000 to USEC. Discover how carrier blank sailings, space deficits, and tariff front-loading are driving this early peak season crunch.

Ocean freight rates hold steady, but massive June GRIs loom. Discover how carrier blank sailings and terminal capacity constraints are driving up transpacific shipping costs.

Transpacific ocean freight rates soared past $6,000 to the USWC and hit the mid-$7,000s to the USEC. Discover how front-loading and severe space constraints are driving this week's market update.

Ocean freight rates double for USWC and USEC as carrier capacity cuts trigger severe space shortages and rolled cargo. Read the latest weekly freight market update on rising spot rates, premium expedited shipping surges, and the June GRI outlook.

China–US freight rates drop again: $1,400 to West Coast, $2,300 to East Coast, as carriers cut prices before September hikes.

Understand why ocean freight rates are climbing despite record low volumes. Our March 2026 update covers the $600 rate hikes, new emergency fuel surcharges, and how blank sailings are impacting China-to-US shipping costs.

The Panama canal is experiencing lower water levels as a result of a drought exacerbated by El Nino. The results of this drought have implications for all sizes of shippers around the world but particularly for small to medium sized shippers that are in a

China–US ocean freight rates remain elevated, with CEA to USWC pricing above $6,000 while promotional carrier deals help some shipments move lower. Learn what is driving rates and what to expect heading into July.

China-US ocean freight rates continue to decline, with the East Coast premium narrowing as carriers compete for limited volume. Get the key market drivers and outlook in this week’s update.

Explore how aggressive blank sailings and new blended rate strategies are stabilizing CEA to USWC/USEC shipping costs despite weak demand. Stay informed on current ocean freight market updates and rate changes.