Global economy adjusts to a highly transactional centralized trade architecture dictated by the US, forcing other major powers to solidify a multipolar landscape of alternative alliances. Seeking to shield its automotive and industrial sectors from American pressure, the European Union successfully brokered a major concession pact with Washington to cap general tariffs at 15%, while simultaneously signing a sweeping free-trade expansion with Mexico to open up non-US supply chains. This regional buffering was mirrored in South Africa’s aggressive hike of domestic steel tariffs to maximum WTO levels and China’s expanding zero-tariff framework with Africa. Collectively, the week proved that while the US continues to weaponize its market through strict new full value metal duties and targeted Section 301 labor probes, the rest of the world is adapting through hyper-localized regional pacts designed to bypass Washington entirely.

The transpacific container spot market is holding steady at highly elevated levels as the month of May comes to a close, maintaining the standard baseline established over the last few weeks.

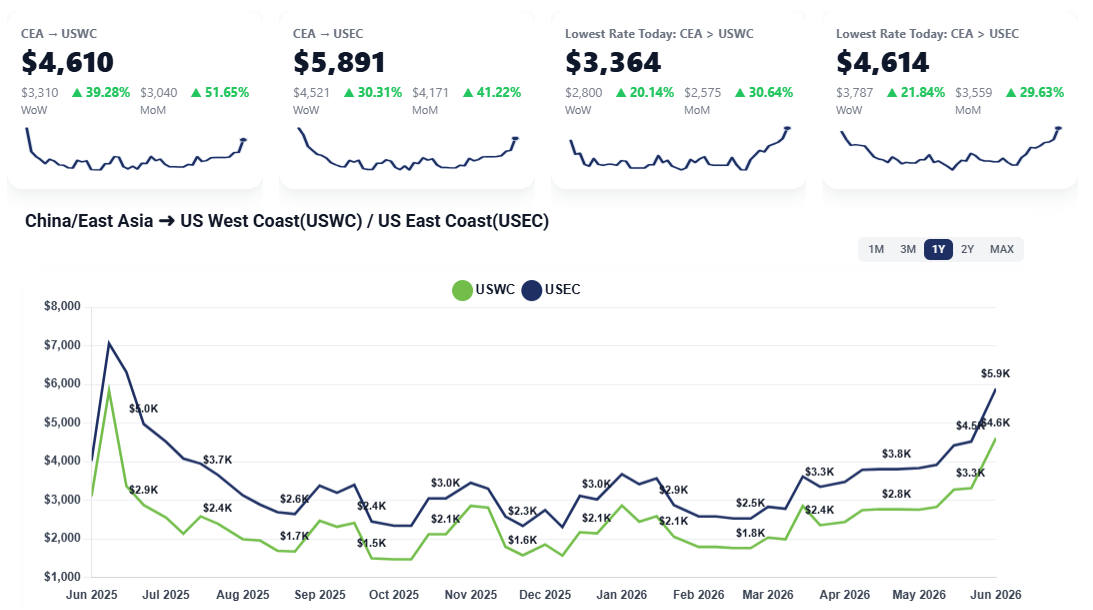

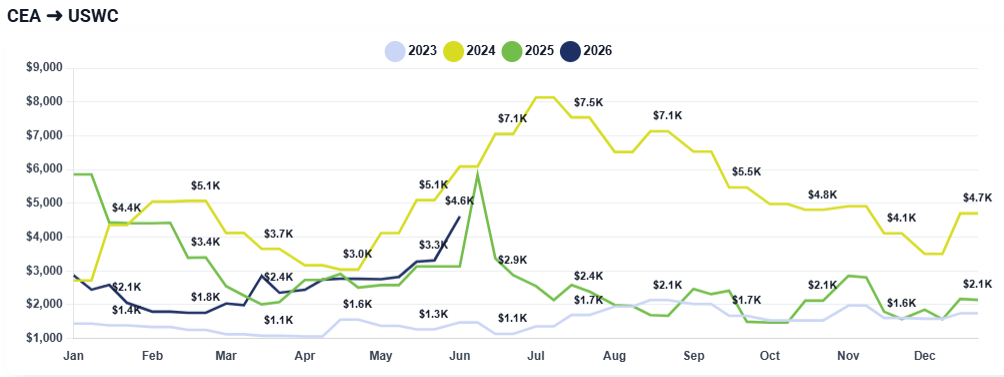

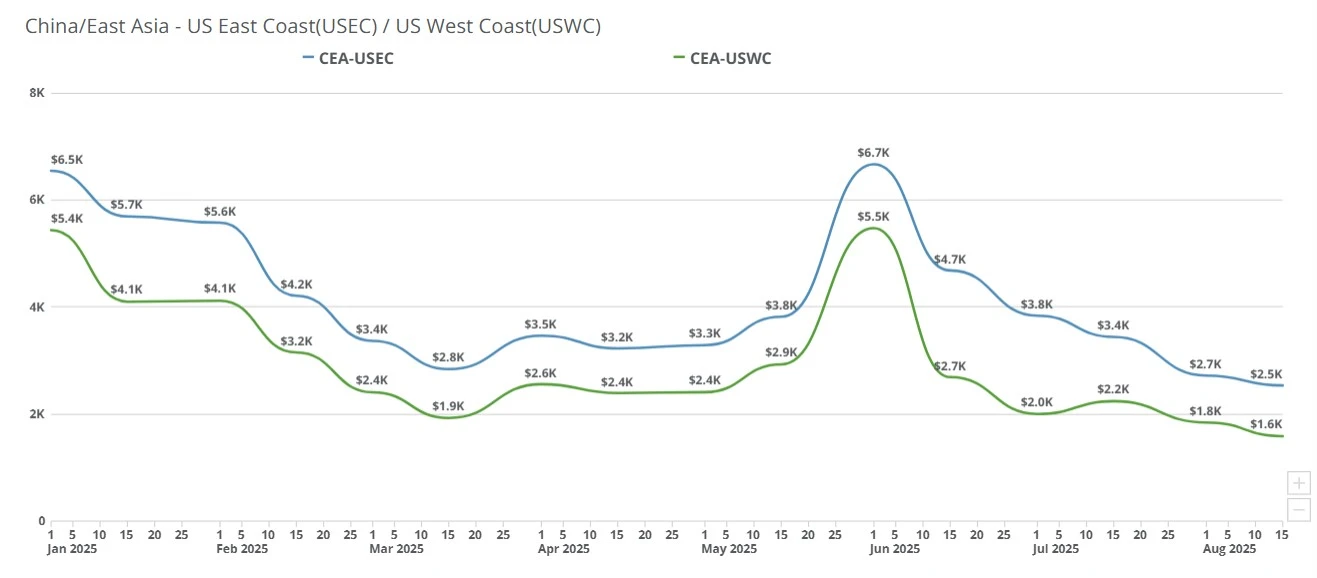

CEA to USWC: Rates are expected to go up to $4,600 per FEU by end of this month to early June.

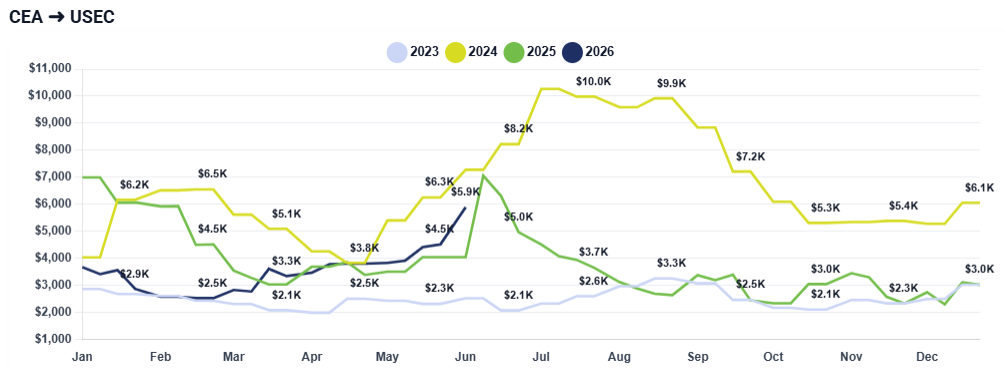

CEA to USEC: Similarly, rates from CEA to USEC is also expected to increase from $4,500 per FEU to around $5,800 by the start of next month.

This current stability this end of May is acting as the calm before an impending storm. Multiple major carriers have issued aggressive General Rate Increase (GRI) indications for June.

Freight Right’s Lowest Rate indicators are finding that importers can find spot rates as low as $3,300 from China to US West Coast and $4,600 from China to US East Coast. Talk to your freight forwarder about options available to you.

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

The "Traffic Jam" Ripple Effect: Ocean carrier loops originate in China before moving down to Southeast Asian hubs like Vietnam and Thailand. Delays and schedule disruptions on the Chinese leg are creating a highway-style traffic jam, triggering rolling delays and congestion throughout secondary Southeast Asian markets.

Widespread Container Rolling: Carriers are systematically booking cargo and implementing "blanked" or changed vessel rotations only after containers are checked into the terminal. Because the equipment is locked behind customs control inside the terminal, shippers are trapped and unable to pull their cargo to switch carriers, forcing them to wait out weekly delays.

Summer Peak and Hospitality Demand: Importers with hard seasonal requirements, specifically those handling summer peak retail products and hospitality supply chains, are aggressively pushing cargo forward regardless of price premiums, inflating short-term demand.

Geopolitical and Fuel Pressures: Rising fuel costs driven by Middle Eastern volatility, alongside complex vessel diversions, continue to establish a high structural floor for operating costs.

The structural setup for June points toward a brutal, highly compressed freight environment. Shippers should expect volume numbers to slide as non-essential importers choose to pause and wait out the market spikes until July or later. However, for freight forwarders, this drop in volume will likely be counterbalanced by expanding cash margins, as generating fixed percentages on a $6,000 rate container yields significantly better dollar returns than on a sub-$2,000 container.

The primary metric to watch over the next two to three weeks will be carrier capacity management. If ocean lines successfully maintain strict blank sailing counts and keep vessel rotations tightly restricted, the $4,800 (USWC) and $6,000 (USEC) thresholds will become reality. If carriers soften their blanking strategy and ease capacity constraints, the rate market is likely to cap out below the terrifying $5,000 mark. Shippers must also keep an eye on upcoming tariff timelines; with key 10% structural tariff exemptions expected to expire around July, any subsequent shifts in trade policy could heavily influence late-summer booking behavior.

Bloomberg: The Race for US Tariff Refunds Gets Off to a Quiet Start

https://www.bloomberg.com/news/newsletters/2026-05-26/trump-tariff-refunds

CNBC: Trump said he'd 'remember' companies that didn't apply for tariff refunds. Many of them are anyway

https://www.cnbc.com/2026/05/22/trump-tariff-refunds-walmart-home-depot-target-apply.html

Financial Times: The power struggle in the world’s narrow seas

https://ig.ft.com/maritime-chokepoints/

Reuters: Mexico, EU sign stalled trade deal as they aim to diversify from US

https://www.reuters.com/world/americas/mexico-eu-sign-stalled-trade-deal-they-aim-diversify-us-2026-05-22/

WSJ: World Trade Grew Strongly at Start of Year on AI Boom

https://www.wsj.com/economy/trade/world-trade-grew-strongly-at-start-of-year-on-ai-boom-c522479c

Late-June front-loading has triggered a severe transpacific space crunch. Discover how carrier rate hikes are driving ocean freight costs to new heights as shippers scramble for limited vessel capacity.

China-US rates remain stable at $2,700-$3,800, but blank sailings and vessel overloading are causing record shipment rollovers and strategic rerouting through Busan.

Ocean freight rates double for USWC and USEC as carrier capacity cuts trigger severe space shortages and rolled cargo. Read the latest weekly freight market update on rising spot rates, premium expedited shipping surges, and the June GRI outlook.

Ocean freight rates skyrocket past $6,000 to USWC and $7,000 to USEC. Discover how carrier blank sailings, space deficits, and tariff front-loading are driving this early peak season crunch.

Transpacific ocean freight rates soared past $6,000 to the USWC and hit the mid-$7,000s to the USEC. Discover how front-loading and severe space constraints are driving this week's market update.

China–US ocean freight rates fell week-over-week as weak January demand erased early GRIs. See what’s driving transpacific pricing and where rates may head next.

China–US ocean freight rates remain elevated, with CEA to USWC pricing above $6,000 while promotional carrier deals help some shipments move lower. Learn what is driving rates and what to expect heading into July.

China-US freight rates dip to $1,520/FEU as carriers cut prices and blank sailings set up a $1,000 September GRI amid weak demand and tariff risks.

Understand why ocean freight rates are climbing despite record low volumes. Our March 2026 update covers the $600 rate hikes, new emergency fuel surcharges, and how blank sailings are impacting China-to-US shipping costs.

Carriers use aggressive blank sailings to maintain China-US rates at $2,700, while shippers withhold volume in anticipation of a May price drop. Explore the impact of fuel surcharges and booking rolls on your supply chain.