- Home

- >

- News

- >

- China–US Ocean Freight Market Holds Firm, but Promotional Rates Gain Traction - TFX Update wk. June 22, 2026

China–US Ocean Freight Market Holds Firm, but Promotional Rates Gain Traction - TFX Update wk. June 22, 2026

The Lead:

Last week, global trade policy activity centered on efforts to stabilize key economic relationships while new tariff and enforcement risks continued to develop. The European Parliament approved the EU-US tariff agreement, helping preserve a 15% tariff framework for most EU exports to the United States while expanding access for U.S. industrial, agricultural, and seafood products. At the same time, the EU and UK prepared for a July summit aimed at easing post-Brexit trade frictions, particularly in food and agricultural goods. In North America, the United States and Mexico advanced USMCA review discussions covering rules of origin, steel, aluminum, autos, agriculture, labor, and economic security. However, tensions also increased as USTR launched a Section 301 investigation into Germany’s pharmaceutical pricing policies, raising the possibility of future trade retaliation. In Asia, the United States and India moved toward further trade negotiations, with India emphasizing the importance of reaching a deal quickly to strengthen its tariff position relative to regional competitors. Overall, the week reflected a mix of negotiated tariff management, regional trade realignment, and targeted enforcement actions shaping global trade policy.

This Week’s Ocean, Air & Freight Markets

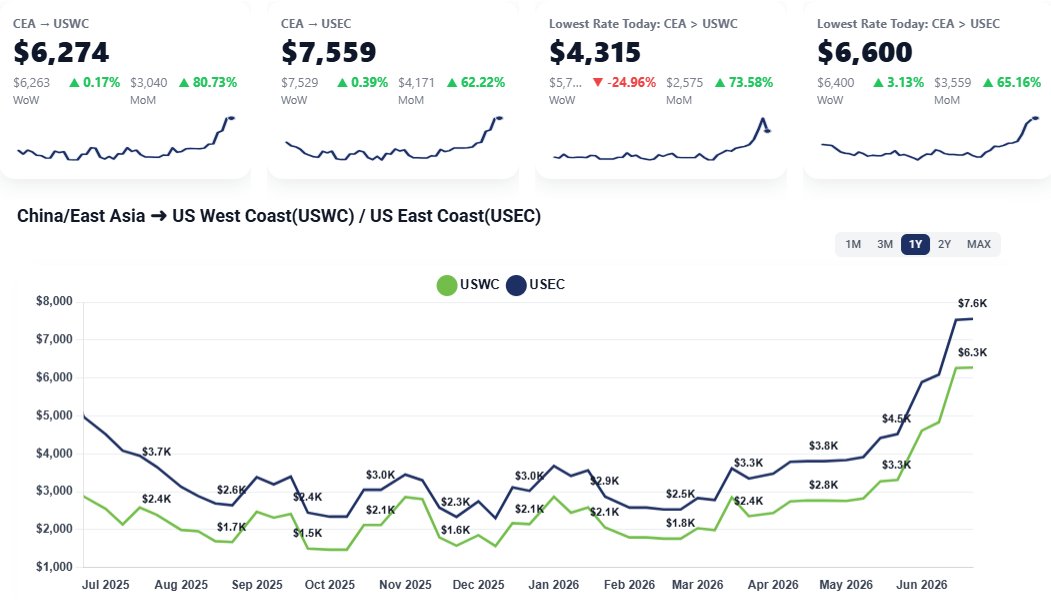

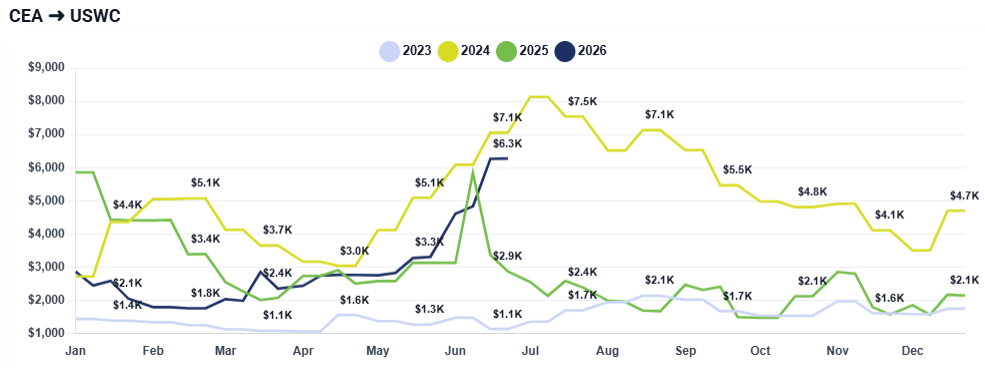

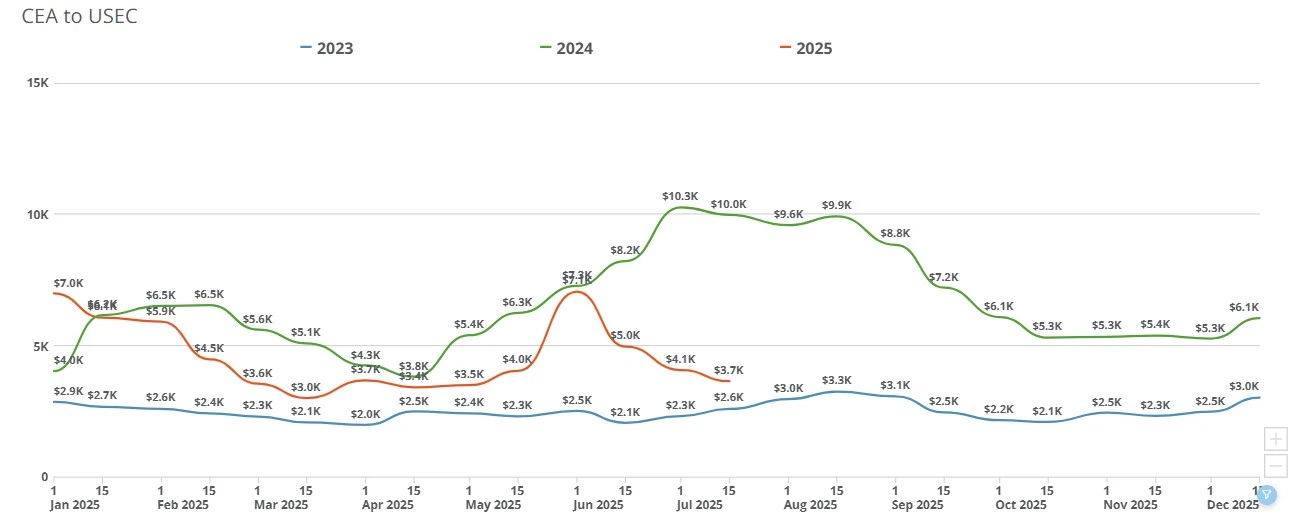

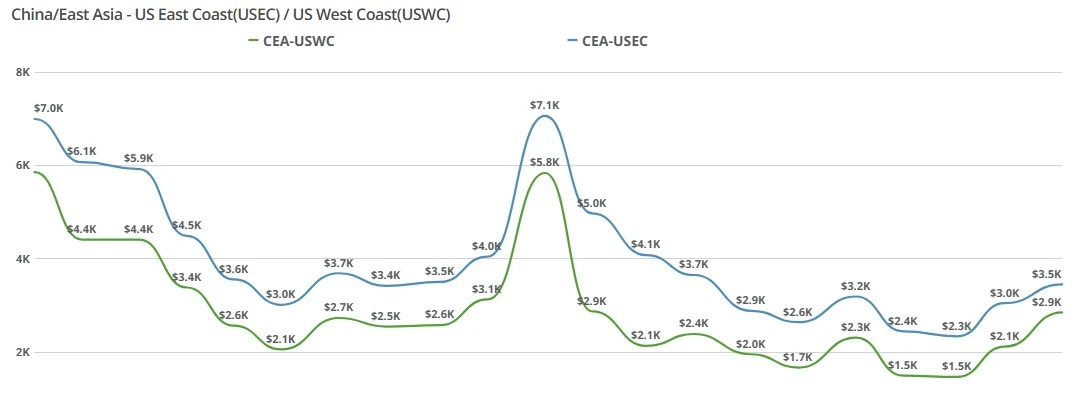

China-US Ocean Freight Market:

CEA to USWC: Rates remained elevated this week, with standard market levels still pushing above $6,000 per container. However, carriers and agents are increasingly making deal or promotional rate structures available, allowing some shipments to move closer to the $5,700–$5,800 range when volume, allocation, or carrier-ratio requirements can be met.

CEA to USEC: market appears broadly unchanged week over week, with no major new rate movement called out this week. The overall pricing environment remains firm, but the most visible competitive pressure is showing up on the West Coast, where high spot levels are beginning to push some importers to pause or delay non-urgent cargo.

Freight Right’s Lowest Rate indicators are finding that importers can find spot rates as low as $4,315 from China to US West Coast and $6,600 from China to US East Coast. Talk to your freight forwarder about options available to you.

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

What Happened This Past Week

End-of-Month Volume Depletion: As June comes to a close, the initial wave of urgent peak-season cargo has already sailed. The remaining leftover volume in the market is less time-sensitive, leaving forwarders fighting harder over a smaller pool of active shippers.

Stricter Carrier Ratio Deals: To guarantee vessel occupancy while capitalizing on high spot rates, carriers are tying low, fixed-contract space (~$3,000) to standard market-rate space. These ratios have become significantly tougher for forwarders, escalating from a 1:1 requirement to 1:3, 1:4, or even 1:5, effectively dragging the blended deal price up closer to the standard spot market.

Aggressive Forwarder Competition: Because space is tight but active customer volume is pausing, freight forwarders are aggressively passing these blended carrier deals directly to shippers. Profit margins are being squeezed as forwarders use these discounts defensively to prevent clients from cross-shopping.

Looking Ahead:

The market is likely to stay firm into July, with continued pressure on space and rates. However, the tone is shifting. Importers are no longer simply accepting higher prices across the board; more are weighing whether to ship now or wait. That customer hesitation is forcing forwarders to be more strategic with deal rates, relationship management, and urgency-based messaging.

If July brings another general rate increase or further tightening, the current “ship now before it gets worse” message may continue to be effective. But if customer pushback grows, we could see more selective discounting or promotional structures used to protect volume, even while headline market rates remain elevated.

In the News:

WSJ: See the Global Chokepoints That Carry Much of the World’s Trade

https://www.wsj.com/world/see-the-global-chokepoints-that-carry-much-of-the-worlds-trade-9683adf2

CNBC: Bruegel’s Wolff says G7 seeks global trade rebalancing

https://www.cnbc.com/video/2026/06/16/g7-leaders-looking-to-achieve-a-global-trade-rebalancing--bruegel.html

Bloomberg: Trump’s New US Tariff Wall Shakes Up Winners, Losers Lineup

https://www.bloomberg.com/news/articles/2026-06-22/trump-builds-a-new-us-tariff-wall-in-shakeup-of-winners-losers

Reuters: India seeks tariff advantage over peers in push to finalise US trade deal

https://www.reuters.com/world/india/india-seeks-tariff-advantage-over-peers-push-finalise-us-trade-deal-2026-06-22/

ABC News: China Shock 2.0: Surging Chinese exports threaten Europe's economy, raising concern

https://abcnews.com/Business/wireStory/china-shock-20-surging-chinese-exports-threaten-europes-133910524

More News

Ocean Freight Rates Hold Firm as Carriers Defend Pricing Into 2026 Contract Season - TFX Update wk. December 29, 2025

Transpacific ocean freight rates from China to the US West and East Coasts remained elevated week over week as carriers held firm through the holiday slowdown, positioning pricing ahead of Chinese New Year and upcoming contract season negotiations.

Importers Race Against July Tariff Deadlines, Throwing Supply Chains Into Chaos - TFX Update wk. June 8, 2026

Ocean freight rates skyrocket past $6,000 to USWC and $7,000 to USEC. Discover how carrier blank sailings, space deficits, and tariff front-loading are driving this early peak season crunch.

Carriers Prepare August GRIs Following Sharp West Coast Rate Decline - TFX Update wk. July 27, 2026

China to US ocean freight rates declined again this week, led by sharp drops on West Coast routes while East Coast pricing remained relatively resilient. Learn what's driving the market correction, August rate increases, and what to expect as peak shippin

Wait-and-See Grips Importers As Rates Remain Unchanged - TFX Update: wk. July 28st, 2025

As the deadline before reciprocal tariffs take place, the Trump administration continues to make deals with nations around the world. Importers are back to taking a wait-and-see approach while rates USWC and USEC remain unchanged.

China-US Ocean Rates Hold Steady at $3K/$4K Baseline Ahead of Threatened June Spikes - TFX Update wk. May 25, 2026

Ocean freight rates hold steady, but massive June GRIs loom. Discover how carrier blank sailings and terminal capacity constraints are driving up transpacific shipping costs.

Carriers Hold Firm on Fuel Surcharges Despite Emerging US-Iran Peace Plans - TFX Update wk. June 15, 2026

Transpacific ocean freight rates soared past $6,000 to the USWC and hit the mid-$7,000s to the USEC. Discover how front-loading and severe space constraints are driving this week's market update.

August Ocean Rate Increase Begins to Unravel as Importers Hold Back - TFX Update wk. August 3, 2026

China to US ocean freight rates rose above $7,000 in early August, but weak demand, excess West Coast capacity, and aggressive discounting are pushing rates back toward the mid-$5,000 range

Freight Market Correction Deepens on CEA-US Routes After November GRI - TFX Update wk. November 3, 2025

China–US ocean freight rates fall as carriers discount to fill space. CEA-USWC down $400-$500; CEA-USEC near $2,800. See what’s driving the drop and what’s next.

Late-June Front-Loading Exacerbates Severe Transpacific Space Crunch

Late-June front-loading has triggered a severe transpacific space crunch. Discover how carrier rate hikes are driving ocean freight costs to new heights as shippers scramble for limited vessel capacity.

Ocean Rates Hold Firm as China Factories Reopen - TFX Update wk. March 2, 2026

Ocean rates hold at $1,450-$1,500 for USWC as Chinese factories reopen. Explore why the post-holiday rate crash didn't happen and what to expect for the March recovery.