Last week reflected a sharper turn toward defensive and enforcement-driven trade policy. In Europe, the EU’s new steel import framework took effect on July 1, setting annual tariff-free quotas at 18.3 million tonnes and applying a 50% duty on out-of-quota imports as part of its response to global steel overcapacity and import pressure.

The UK introduced a similar steel trade measure the same day, reducing tariff-free quota volumes by 51% and applying a 50% tariff on imports above those limits. In North America, the United States declined to renew USMCA in its current form during the agreement’s mandatory joint review, keeping the pact in force while pushing it into a more uncertain annual review process.

At the same time, US Trade Representative (USTR) advanced two major Section 301 tracks: a Brazil-focused action covering practices tied to digital trade, preferential tariffs, intellectual property, ethanol market access and illegal deforestation, and a broader forced-labor-related proceeding covering 60 economies accused of failing to effectively restrict imports made with forced labor.

Taken together, the week showed how tariff policy is increasingly being used not only to protect domestic industries, but also to enforce labor, environmental, industrial and geopolitical priorities across global supply chains.

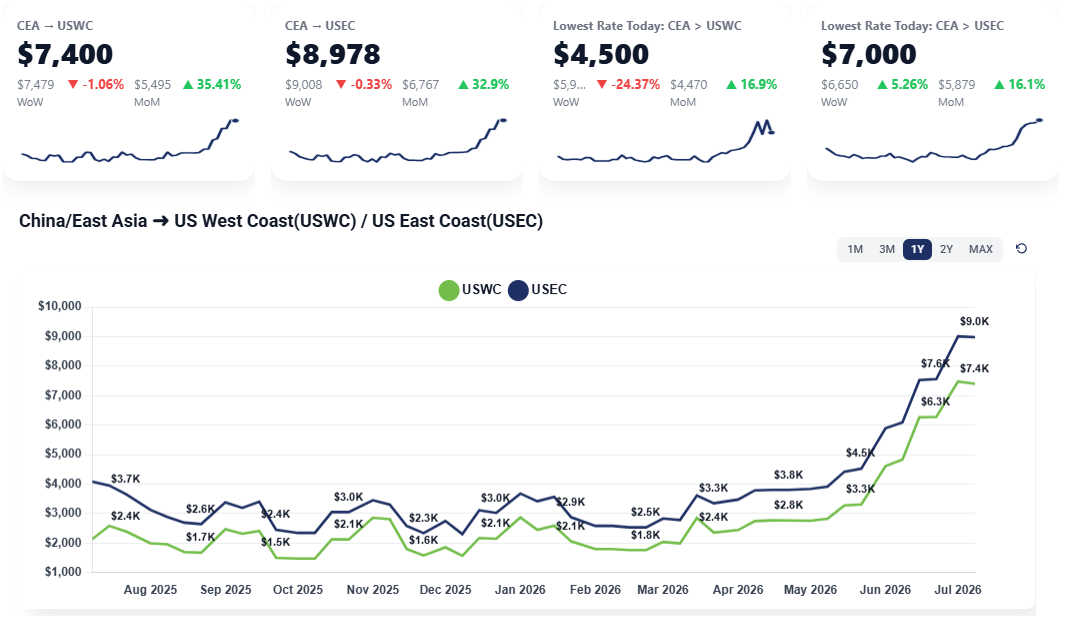

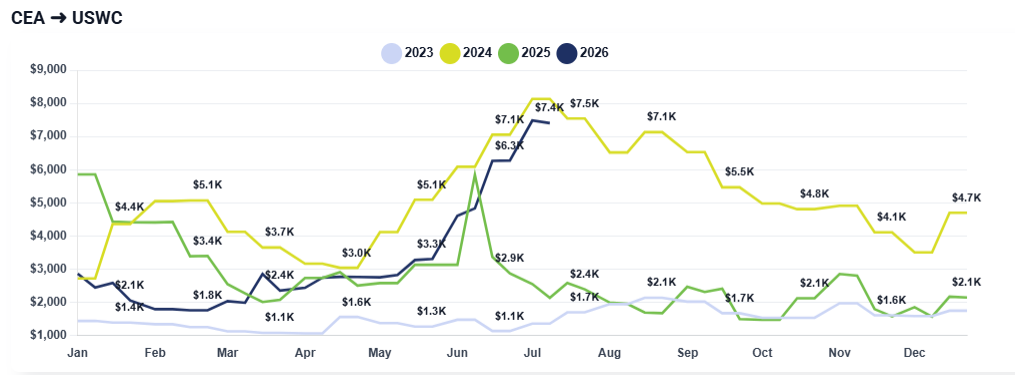

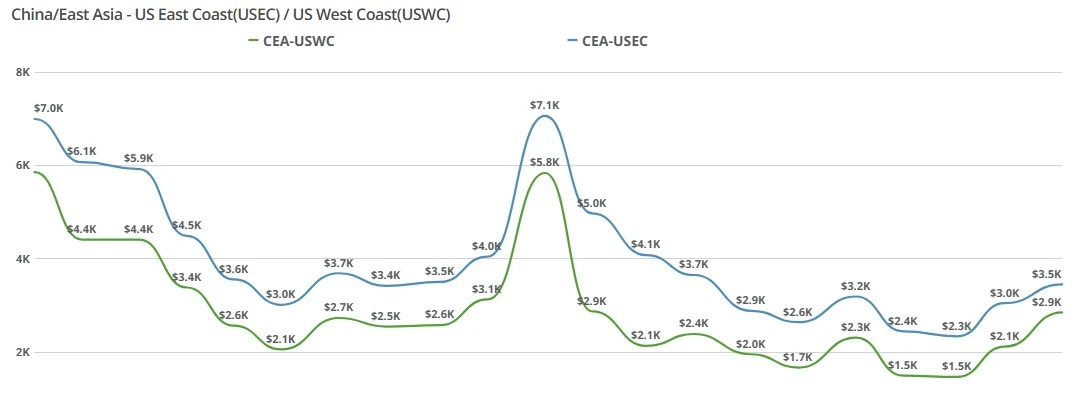

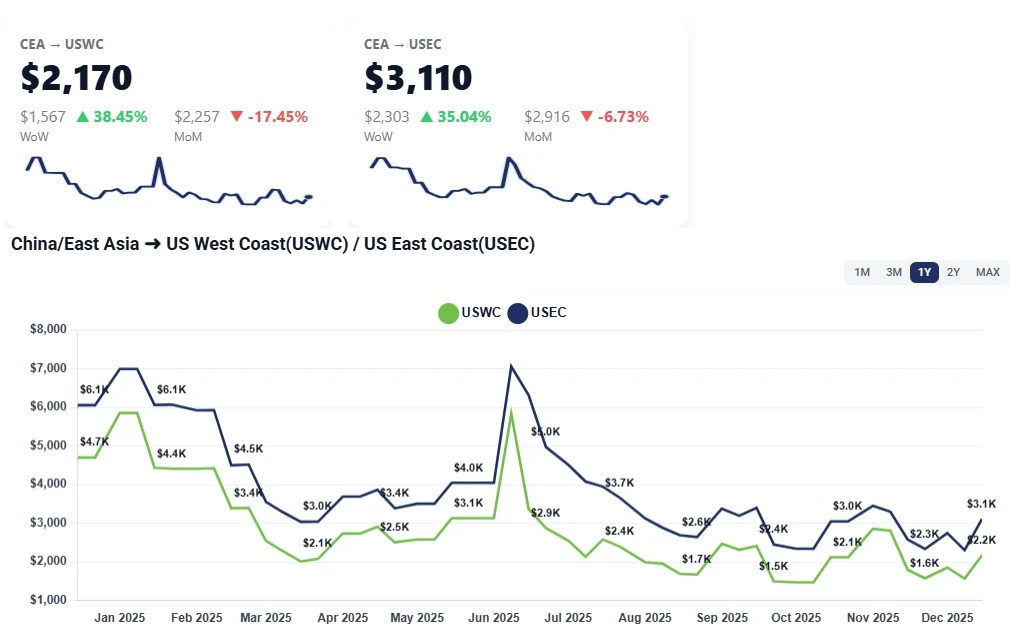

CEA to USWC: Spot rates remain elevated in the mid $7,000 range, though some carriers are beginning to offer small reductions of around $100–$200 week over week. The lane appears to have reached a near-term ceiling after the recent run-up, with demand still soft and no significant rush from shippers to move cargo quickly.

While rates are still among the highest levels seen since the COVID-era freight surge, the market now looks more likely to hold steady or ease slightly than continue climbing.

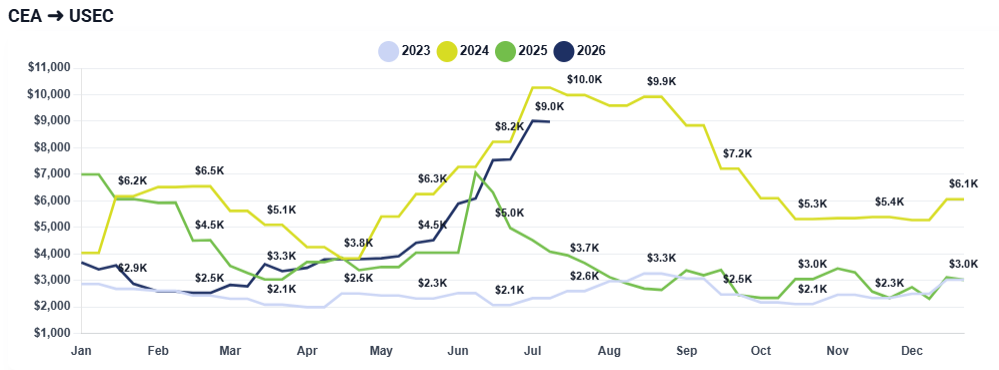

CEA to USEC: East Coast rates are also holding at historically high levels, with pricing at $8,000-plus range and some inland or longer-haul movements likely remaining more expensive. However, like the West Coast lane, the direction is beginning to soften slightly as carriers respond to weaker booking activity.

The market is not seeing enough volume improvement to justify another increase, and any further movement appears more likely to be flat to modestly lower rather than upward.

Freight Right’s Lowest Rate indicators are finding that importers can find spot rates as low as $4,500 from China to US West Coast and $7,000 from China to US East Coast. Talk to your freight forwarder about options available to you.

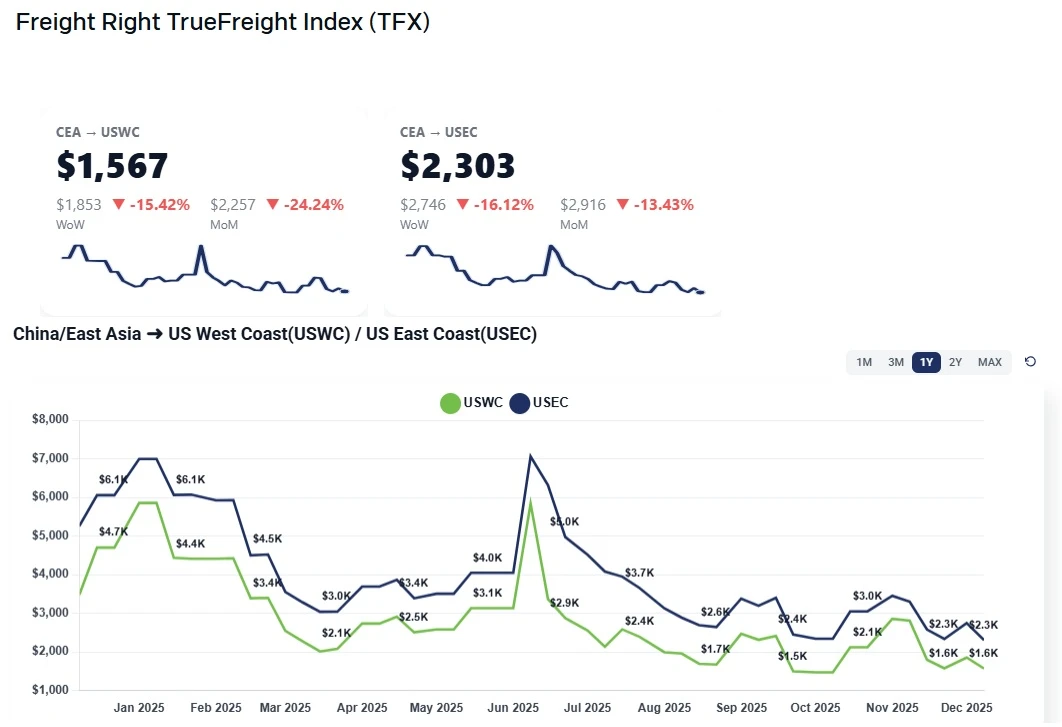

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

Rates may have hit their ceiling. The market has reached a point where further increases could risk stopping demand altogether, pushing carriers to make small adjustments downward.

The US holiday slowed activity. With the first week of July partly affected by the US holiday, carriers had fewer business days to assess real demand, making this week more important for measuring booking momentum.

Carriers are likely seeing softer booking requests. The modest reductions suggest carriers may already be responding to lower demand signals.

Weather may create temporary disruption. Tight air cargo space was attributed more to Typhoon Maysak in China than to strong cargo volume.

The near-term outlook points to a market that is likely to hold steady or gradually decline rather than move higher. The recent peak appears to have been reached, and without a rebound in volume, carriers may have limited room to defend current rate levels for long.

That said, a sharp collapse is not guaranteed. Carriers are expected to manage the decline carefully and may avoid aggressive reductions unless booking activity weakens further. The next one to two weeks will be important for determining whether August brings a meaningful peak season or whether the market settles into a softer summer pattern.

Tariff uncertainty could also influence shipper behavior later in July. If new tariff developments trigger another round of urgency, some short-term demand could return. But based on this week’s market reality, the more likely path is slight downward pressure with rates remaining elevated by historical standards.

NBC News: Trump refuses to renew USMCA trade pact, toppling one of the last pillars of stability in global trade

https://www.nbcnews.com/business/economy/trump-usmca-renewal-tariffs-trade-rcna352594

The Business Times: US forced-labour hearing begins, paving way for more Trump tariffs

https://www.businesstimes.com.sg/international/global/us-forced-labour-hearing-begins-paving-way-more-trump-tariffs

Reuters: EU trade with US hits record high despite tariff tensions, study shows

https://www.reuters.com/business/eu-trade-with-us-hits-record-despite-tariff-tensions-study-shows-2026-07-03/

Reuters: Democratic AGs oppose Trump plan to impose tariffs on forced labor concerns

https://www.reuters.com/world/us/democratic-ags-oppose-trump-plan-impose-tariffs-forced-labor-concerns-2026-07-06/

WSJ: Trump’s Brokerage Accounts Made Big Trades Around ‘Liberation Day’ Tariffs

https://www.wsj.com/finance/stocks/trumps-brokerage-accounts-made-big-trades-around-liberation-day-tariffs-06e92290

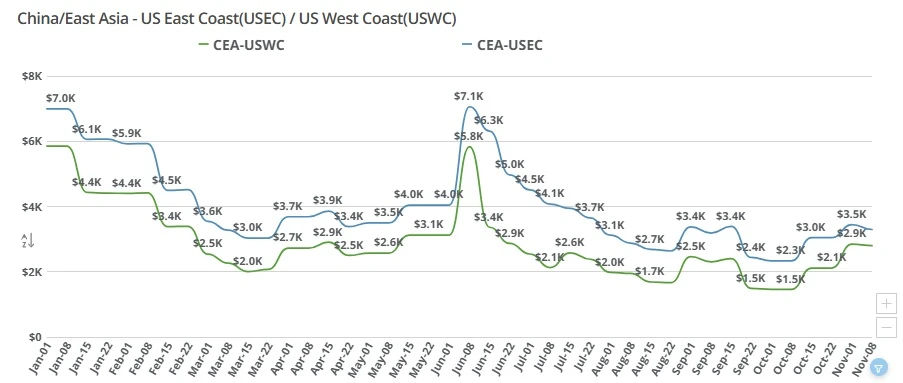

Transpacific ocean freight rates from China to the US West and East Coasts remained elevated week over week as carriers held firm through the holiday slowdown, positioning pricing ahead of Chinese New Year and upcoming contract season negotiations.

Weekly ocean freight update on China–US West and East Coast lanes as an early December GRI fades, leaving spot rates near November levels amid weak demand.

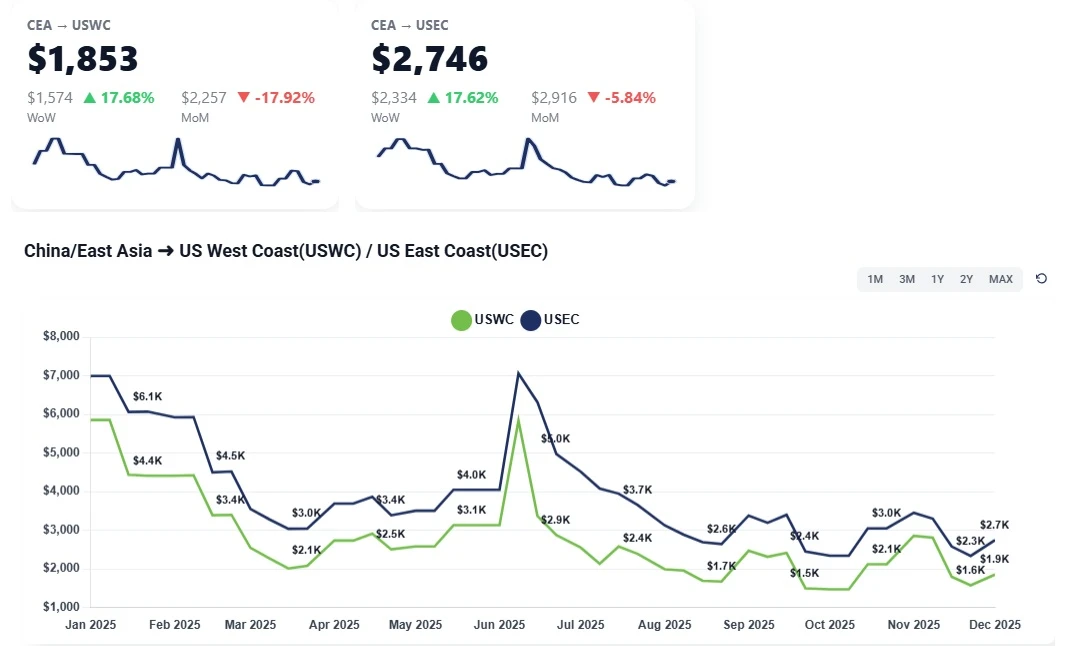

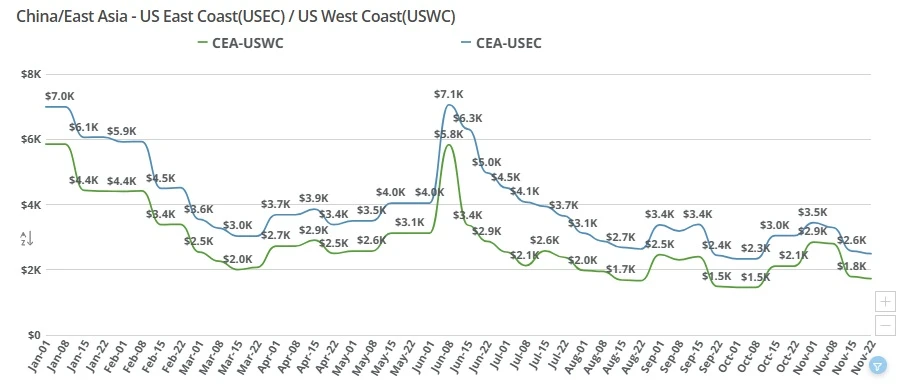

China–US ocean freight rates fall as carriers discount to fill space. CEA-USWC down $400-$500; CEA-USEC near $2,800. See what’s driving the drop and what’s next.

Transpacific ocean freight rates continue to decline as post-peak demand cools. China–US West Coast rates near $1,700, East Coast around $2,600 per FEU.

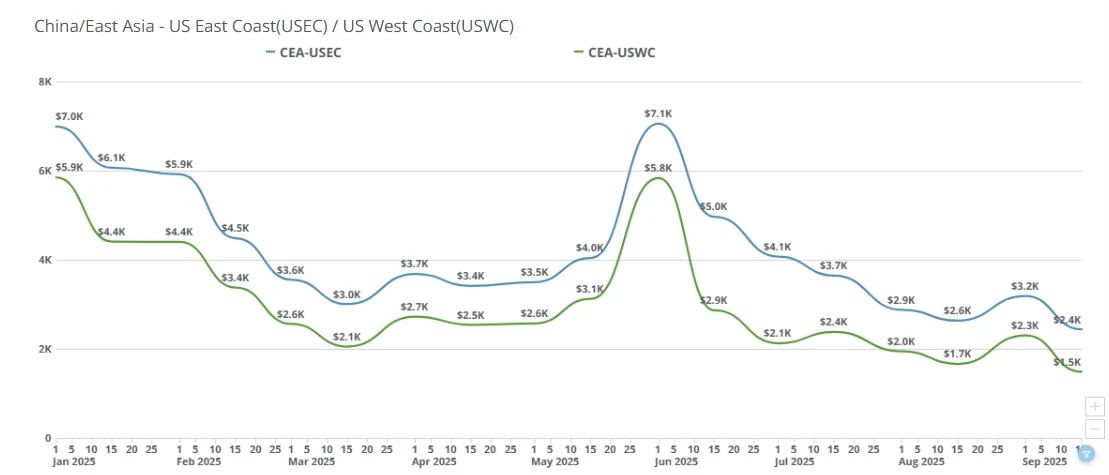

FEU & TEU rates change slightly week-over-week, importers that can afford to keep importing are continuning to do so while those that are hamstrung by tariffs are sidelined and the August 1st tariff deadline is one week away.

Transpacific ocean freight rates dropped sharply this week as weak import demand and the Thanksgiving holiday slowdown pushed China–US West and East Coast spot prices to new lows. Get the latest market drivers and outlook.

China-US spot rates dipped again, with USWC near $1,300/FEU. Golden Week slowdowns and tariff drag curb demand as carriers weigh blank sailings.

China–US ocean freight rates rose WoW: USWC near $2.1K/FEU and USEC near $2.9–$3.0K as carriers end fixed extensions and hold firm into January.

Small December GRIs lift China–USWC and China–USEC rates slightly, but overcapacity, soft demand, and tariff uncertainty continue to cap meaningful recovery. Outlook steady through Chinese New Year with brief January strength.

Understand why ocean freight rates are climbing despite record low volumes. Our March 2026 update covers the $600 rate hikes, new emergency fuel surcharges, and how blank sailings are impacting China-to-US shipping costs.