Last week was defined by the transition from temporary, emergency US surcharges toward a permanent, investigation-justified centralized trade architecture. The USTR’s launch of public hearings for the 60-nation forced labor tariffs signaled that Washington will lock in a new double-digit baseline duty structure before its temporary Section 122 fees expire.

This unyielding protectionist environment, spurred by prior legal constraints like the Court of International Trade's invalidation of universal tariffs, has forced close trading partners like Canada and Cambodia to rapidly rewrite their domestic import laws to claim US compliance exemptions. However, as the joint IMF-WTO summit confirmed that global commerce is becoming deeply uneven under these measures, the week closed with clear signs that the high compliance costs of the US metal multiplier are driving a major manufacturing migration away from secondary regional partners, fundamentally squeezing the North American supply chain.

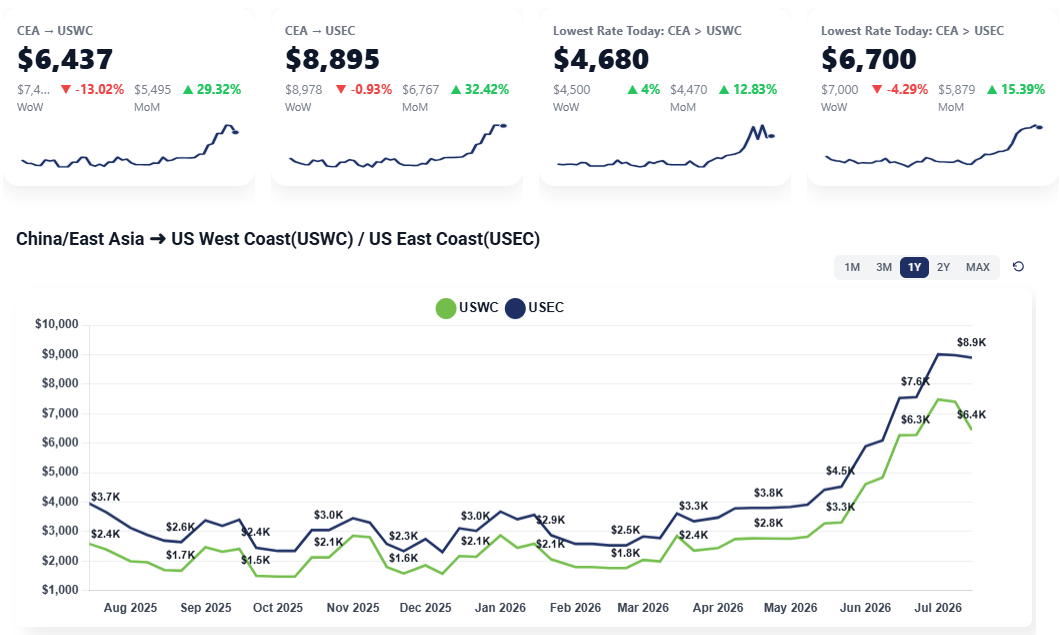

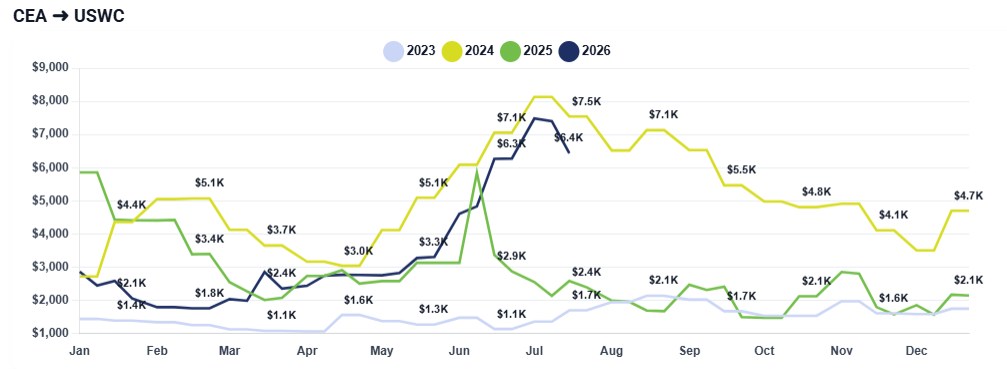

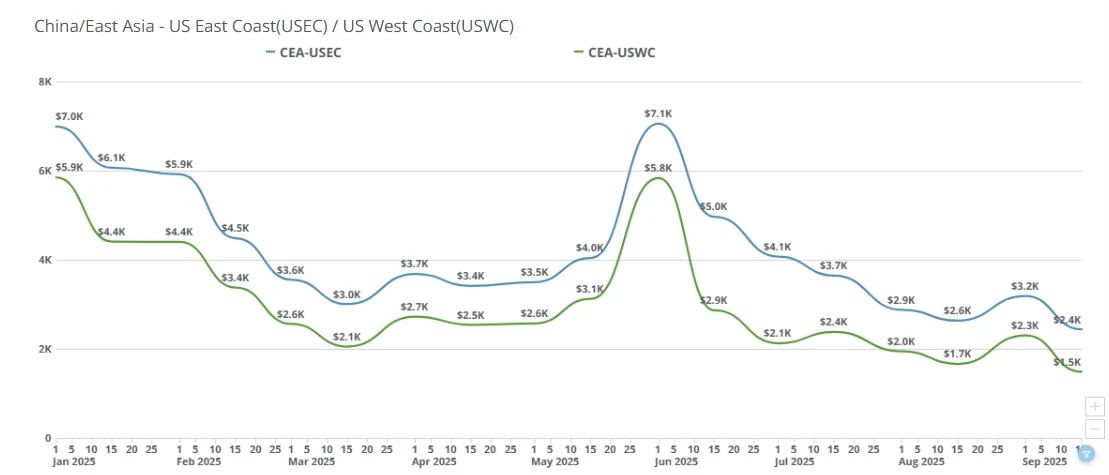

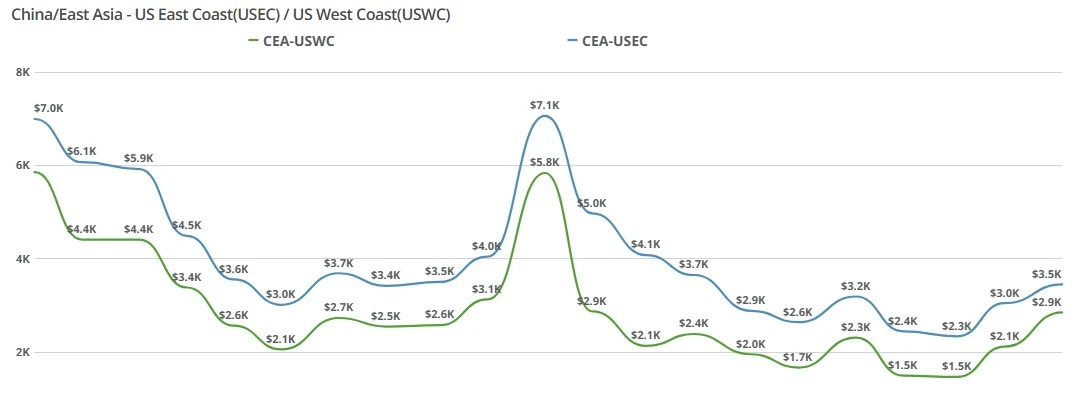

CEA to USWC: Spot rates eased this week, falling from the mid-$7,000 range to the mid-$6,000 range. Carriers have reintroduced fixed-rate space and special-rate allocations, bringing pricing down by approximately $1,000 per container from the early July peak.

Despite the lower pricing, booking volumes remain soft as many importers continue delaying shipments while waiting for greater clarity on US tariff policy.

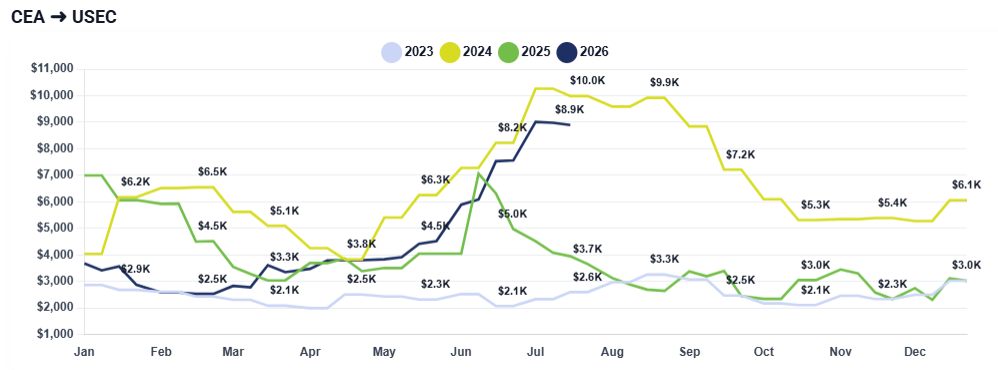

CEA to USEC: Rates to the East Coast, however, declined more moderately, with carriers offering more competitive pricing and improved space availability to stimulate demand. While pricing remains elevated compared to historical norms, the week-over-week decline reflects weakening booking activity rather than increased capacity constraints.

Importers continue adopting a wait-and-see approach, limiting any meaningful rebound in demand despite lower freight costs.

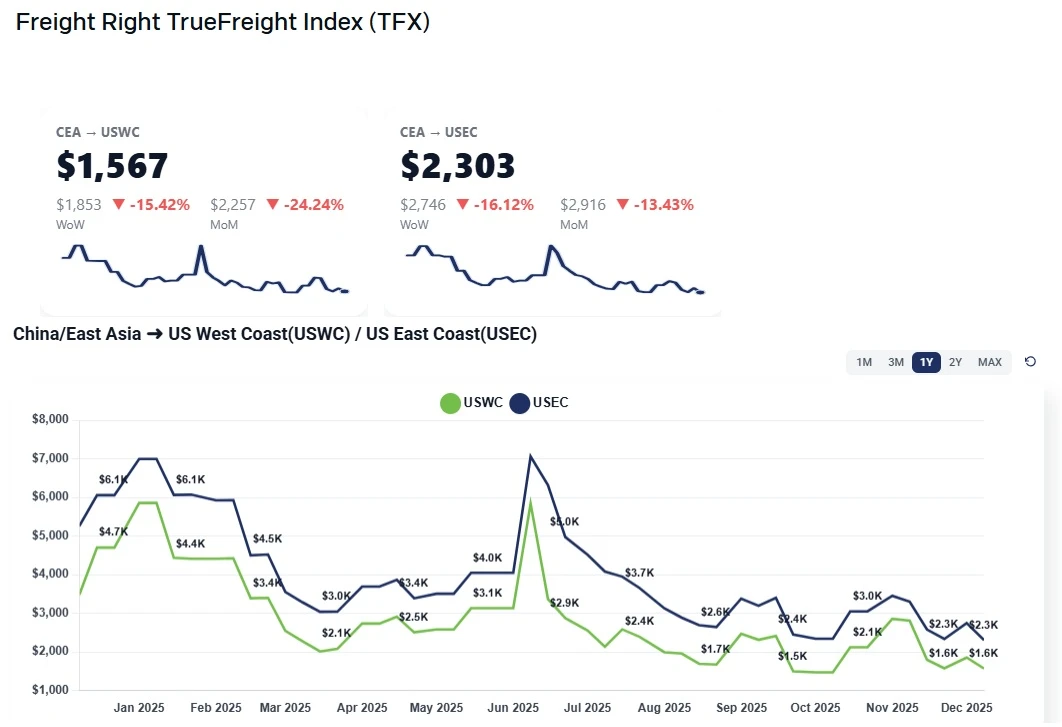

Freight Right’s Lowest Rate indicators are finding that importers can find spot rates as low as $4,680 from China to US West Coast and $6,700 from China to US East Coast. Talk to your freight forwarder about options available to you.

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

Tariff uncertainty is delaying imports. Many importers are postponing customs clearance, or delaying shipments altogether, until there is greater certainty about what happens after the current tariff period expires.

Lower prices are not translating into higher volumes. Despite the rate reductions, freight forwarders are not seeing any meaningful increase in booking activity, suggesting importers remain focused on policy risk rather than transportation costs.

Middle East tensions have not yet impacted rates. Although geopolitical risks remain, market participants believe any effect from oil prices or shipping disruptions would likely take several weeks to filter into ocean freight pricing and may be muted given rates are already at elevated levels.

Peak season may have already occurred. Many importers accelerated shipments during May and June to stay ahead of tariff deadlines, effectively pulling forward the traditional late-summer peak season.

The next two weeks are likely to determine the direction of the trans-Pacific market. If tariff uncertainty is resolved with lower or eliminated duties, import demand could quickly rebound, potentially creating an extended peak season through August and September and pushing ocean rates higher again.

However, if tariffs remain in place, or increase, market participants expect booking volumes to weaken further, putting additional downward pressure on freight rates. With many importers already frontloading inventory earlier this year, the industry may ultimately experience another year without a traditional peak season, instead seeing demand shift around trade policy developments rather than seasonal retail cycles.

The Guardian: US refunds $81bn in Trump tariffs after supreme court ruled them illegal

https://www.theguardian.com/us-news/2026/jul/14/trump-tariffs-us-refunds

Bloomberg: How Trump’s Zest for Tariffs Pits US Industries Against Each Other

https://www.bloomberg.com/news/newsletters/2026-07-14/trump-and-antidumping-tariffs

Reuters: IMF lowers 2026 global growth forecast to 3%, sees rebound in 2027

https://www.reuters.com/world/china/imf-edges-2026-global-growth-forecast-lower-3-sees-rebound-2027-2026-07-08/

CNBC: China exports in June rise at fastest pace since 2021 as AI boom, tariff rush lift trade

https://www.cnbc.com/2026/07/14/china-june-trade-data-exports-imports.html

CNN: After a year of tariffs, automakers are still resistant to moving production to the US

https://edition.cnn.com/2026/07/12/business/tariffs-automakers-new-factories

Ocean freight rates double for USWC and USEC as carrier capacity cuts trigger severe space shortages and rolled cargo. Read the latest weekly freight market update on rising spot rates, premium expedited shipping surges, and the June GRI outlook.

Transpacific ocean freight rates dropped sharply this week as weak import demand and the Thanksgiving holiday slowdown pushed China–US West and East Coast spot prices to new lows. Get the latest market drivers and outlook.

China–US ocean spot rates eased WoW as early-September GRIs faded. USWC nears trough, USEC softens, and fierce forwarder pricing persists ahead of Golden Week.

China–US ocean freight rates fall as carriers discount to fill space. CEA-USWC down $400-$500; CEA-USEC near $2,800. See what’s driving the drop and what’s next.

China–US ocean freight rates from CEA to the US West Coast and East Coast softened slightly week over week as demand remained low, carriers tested modest reductions, and the market appeared to reach a near-term rate ceiling.

Ocean freight rates skyrocket past $6,000 to USWC and $7,000 to USEC. Discover how carrier blank sailings, space deficits, and tariff front-loading are driving this early peak season crunch.

China–US ocean freight rates remain elevated, with CEA to USWC pricing above $6,000 while promotional carrier deals help some shipments move lower. Learn what is driving rates and what to expect heading into July.

China–US ocean freight rates fell week-over-week as weak January demand erased early GRIs. See what’s driving transpacific pricing and where rates may head next.

FEU & TEU rates change slightly week-over-week, importers that can afford to keep importing are continuning to do so while those that are hamstrung by tariffs are sidelined and the August 1st tariff deadline is one week away.

Small December GRIs lift China–USWC and China–USEC rates slightly, but overcapacity, soft demand, and tariff uncertainty continue to cap meaningful recovery. Outlook steady through Chinese New Year with brief January strength.